THE AUTHOR:

To build a fraud detection platform for digital banking, banks need to move fraud checks closer to the moment of action: login, onboarding, beneficiary creation, card payment, account transfer, password reset, or loan application. The pressure is already visible in payment data. The European Banking Authority and the European Central Bank reported that fraud across payment transactions in the European Economic Area reached €4.2 billion in 2024, up from €3.5 billion in 2023. The same report notes that new types of fraud are emerging, especially cases in which legitimate users are manipulated into authorizing fraudulent transactions.

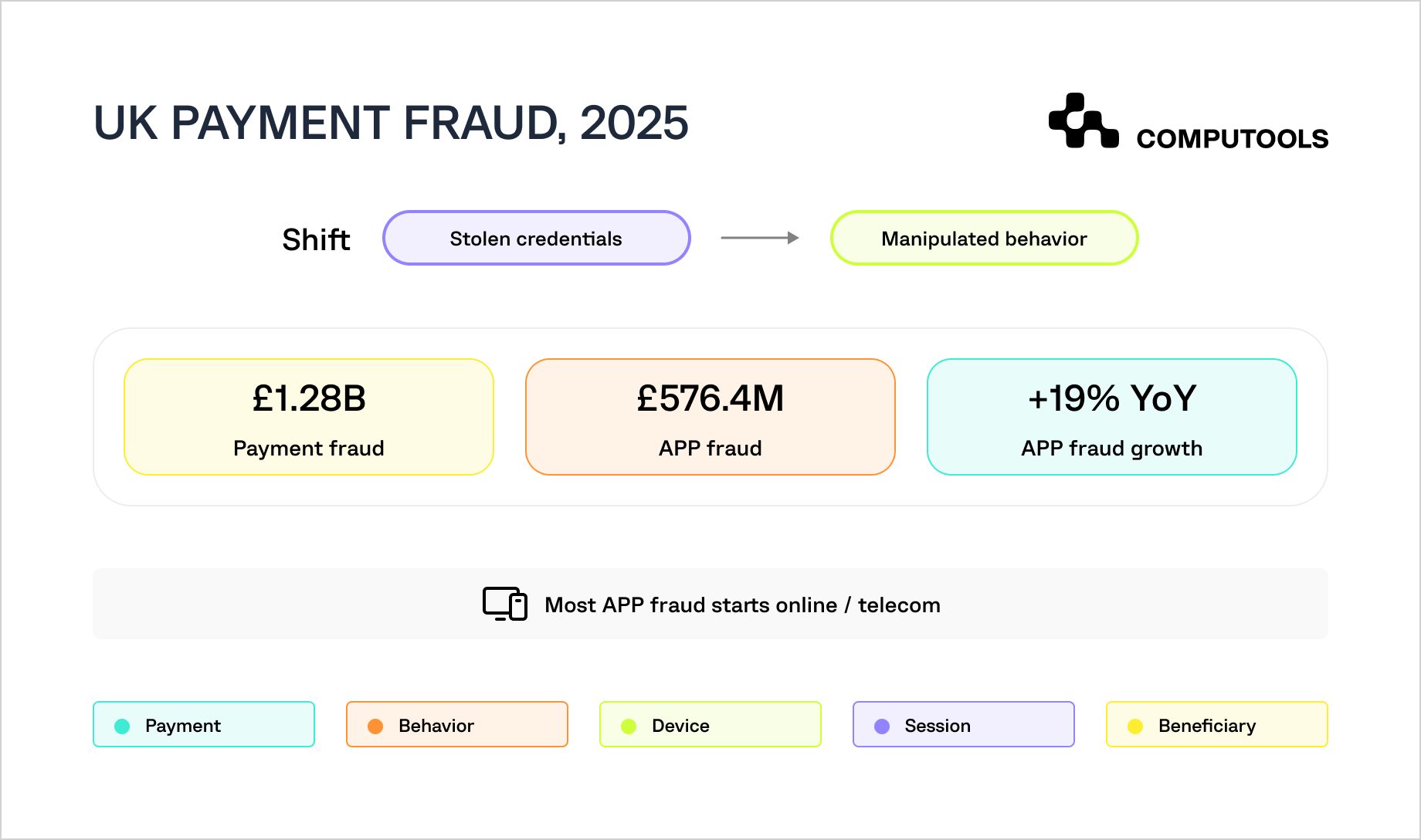

The UK market shows the same shift from stolen credentials to manipulated customer behavior. UK Finance reported that criminals stole £1.28 billion through payment fraud in 2025, while authorized push payment fraud rose to £576.4 million, up 19% year-over-year. Most APP fraud cases start online or via telecommunications, which means banks have to analyze payment data together with behavioral, device, session, and beneficiary signals before money leaves the account.

A real-time fraud detection platform helps financial institutions evaluate these signals while the customer journey is still active. Instead of reviewing suspicious activity after settlement, the system scores risk in milliseconds, applies rules and machine-learning models, flags high-risk actions for step-up verification or manual review, and provides analysts with enough context to make a fast, explainable decision.

How Computools helped a European finance provider build a fraud detection platform

Computools helped a European finance provider strengthen fraud prevention, customer verification, and compliance operations across its digital banking environment. The client needed to reduce manual reviews, improve alert accuracy, accelerate onboarding, and integrate fraud, KYC, AML, and reporting workflows into a single controlled system.

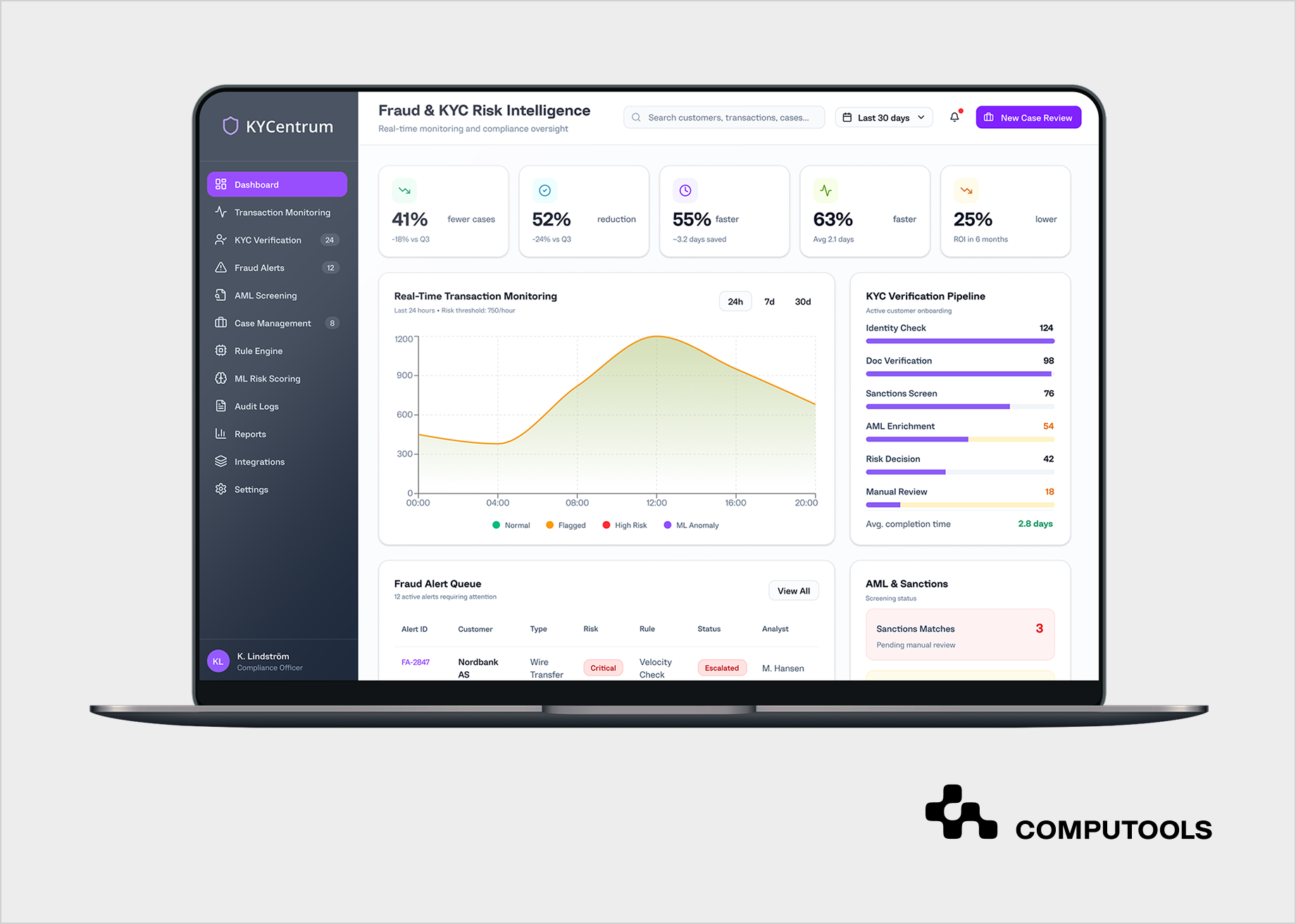

In the KYCentrum project, Computools applied its banking software development services experience to help build a platform for real-time transaction monitoring, automated verification, risk decisioning, and analyst case review.

The client operated across Estonia, Latvia, and Lithuania, serving private and business customers through payments, cards, loans, leasing, savings, pensions, investments, and private banking services. As digital activity grew, static fraud rules and manual KYC checks became harder to scale without increasing operational risk.

Computools developed a platform that combined configurable, rule-based logic; ML-supported fraud scoring; AML and KYC automation; sanctions screening; case management; explainable decision logic; audit trails; and compliance-ready reporting. The solution also used AI development expertise to support anomaly detection, adaptive fraud scoring, and explainable risk signals for compliance teams.

Security was built into the platform architecture through encrypted data exchange, controlled access, secure key management, monitoring, and incident visibility. These controls made cybersecurity services relevant to platform reliability in a regulated banking environment.

The solution reduced confirmed fraud cases by 41%, lowered false-positive alerts by 52%, shortened customer onboarding time by 50–60%, and helped compliance teams resolve cases 63% faster.

How to build a real-time fraud detection platform for digital banking: step by step

Step 1. Define fraud scenarios for digital banking

Before development starts, the bank needs to define which fraud scenarios the platform must detect first. Digital banking fraud detection covers several operational scenarios. A mobile login from a new device, a high-value transfer to a new beneficiary, a failed liveness check during onboarding, and a sudden chain of small outgoing payments are different risk scenarios. Each one requires different data, rules, risk signals, and response logic.

At this stage, the bank should create a fraud taxonomy. It should separate the main types of fraud that affect digital banking operations: account takeover, authorized push payment fraud, suspicious beneficiary creation, mule account activity, synthetic identity, onboarding fraud, card-not-present fraud, loan application fraud, and suspicious account behavior following a customer profile change. This taxonomy helps risk, compliance, product, and engineering teams use the same definitions rather than interpreting “suspicious activity” differently across departments.

Each fraud scenario should then be mapped to specific customer actions. Account takeover may start with several failed login attempts, followed by a successful login on a new device, a password reset, or the creation of a new beneficiary. Mule account activity may appear as frequent incoming transfers followed by fast outgoing payments. Onboarding fraud may involve document inconsistencies, failed liveness checks, mismatched customer data, or risky IP and device signals. These patterns should be documented before the team designs rules, models, or case workflows.

The bank also needs to define what happens after each scenario is detected. Low-risk activity may pass without friction. Medium-risk activity may trigger step-up authentication. High-risk transactions may be held for review. Critical cases may require temporary account restrictions, escalation to fraud analysts, or compliance investigation. This decision logic should be agreed upon before development starts because it affects customer experience, analyst workload, and regulatory exposure.

In the KYCentrum project, this first step mattered because the client operated across several financial products: payments, cards, loans, leasing, savings, pensions, investments, and private banking services. Fraud risks were not limited to a single transaction type or customer journey. The solution had to support fraud and KYC logic across digital payments, remote onboarding, customer verification, AML checks, and compliance reporting.

Result of this step: the bank has a documented fraud taxonomy, mapped risk scenarios, required data points, response actions, and clear ownership for each fraud type. This becomes the foundation for software architecture, transaction monitoring, fraud scoring, AI models, and analyst workflows.

Step 2. Design the platform around operational decisions

After the bank defines fraud scenarios, the next step is to design how the platform will process data, evaluate risk, and return decisions to digital banking workflows. Every key customer action should have a clear path: event capture, data enrichment, risk evaluation, decision, analyst review if needed, and audit record.

The fraud detection platform architecture should integrate banking channels, payment systems, customer profiles, authentication events, device data, KYC and AML services, rule logic, scoring models, case management, reporting, and security controls into a single, controlled flow. This allows the platform to detect risks, explain its decisions, and maintain a complete record for compliance and investigation teams.

The architecture also needs to define how fast each decision must be returned. A card payment, account transfer, or beneficiary creation may require a near-instant response. A remote onboarding case, a document verification issue, or an enhanced due diligence workflow may require more time for review. These differences affect IT infrastructure choices, queue design, fallback logic, API orchestration, and analyst escalation rules.

A strong architecture should also include failure scenarios. If a KYC provider, sanctions screening service, device intelligence tool, or internal banking system is temporarily unavailable, the platform needs a predefined response. It may allow low-risk activity, delay higher-risk operations, request additional verification, or route the case to manual review. These rules should be agreed with the product, risk, compliance, engineering, and customer support teams before implementation.

Security and traceability also belong at this stage. The platform will process sensitive customer data, transaction records, identity verification results, risk signals, and analyst decisions. Access control, encryption, secure API communication, audit logs, monitoring, and incident visibility should be part of the architecture from the beginning. Adding them later usually creates expensive rework and weakens compliance readiness.

In the KYCentrum project, Computools treated the solution as an integrated fraud prevention and compliance platform. The system had to process live financial data, support analyst decisions, protect sensitive customer information, and provide transparent records for internal and external review. Computools contributed to backend services, API orchestration, rule-based workflows, case management, audit trail and reporting logic, and secure data handling.

Result of this step: the bank has a documented architecture that shows how data enters the platform, how risk is evaluated, how decisions are returned, how analysts review cases, how security is enforced, and how every action remains traceable for compliance.

For banks still working with fragmented or legacy systems, Computools also explains how to modernize legacy banking systems without service downtime, a related topic for institutions that need fraud monitoring without disrupting daily operations.

Step 3. Connect reliable banking data sources

After the architecture is defined, the team needs to connect the platform to the data sources that explain customer activity, transaction context, identity status, and risk history. Fraud detection cannot rely only on the transaction amount, currency, and timestamp. These fields show what happened, but they rarely explain whether the action is normal, unusual, manipulated, or clearly suspicious.

A transaction monitoring system needs data from core banking systems, payment processors, card systems, mobile and web banking channels, authentication services, customer profiles, device intelligence tools, CRM systems, onboarding systems, KYC providers, AML screening services, sanctions lists, case management records, and prior fraud outcomes. Each source adds context. A new beneficiary may be harmless to one customer but high-risk to another if it appears after a password reset, a new device login, several failed authentication attempts, or a sudden change in transaction behavior.

Data mapping should be completed before rules and scoring logic are built. The team needs to define which fields are required for each fraud scenario, where they come from, how often they are updated, and whether they are available in real time. This includes customer ID, account ID, transaction ID, device ID, IP address, geolocation, session data, recipient data, verification status, customer risk level, sanctions screening result, and previous alert history.

Data quality is also part of this step. Inconsistent IDs, delayed events, missing timestamps, duplicated records, or disconnected KYC results can distort risk evaluation. If the platform receives incomplete or unreliable data, even strict rules and models will produce weak decisions. Before development moves further, the team should check data freshness, format consistency, ownership, access rights, and retention requirements.

The bank should also separate the data needed for automated decisions from the data needed for analyst review. A payment flow may require fast access to recipient status, device risk, customer behavior, and authentication history. A manual investigation may need deeper context: previous cases, full onboarding history, document verification results, related accounts, analyst comments, and audit records. This separation keeps real-time decisions fast while still giving analysts enough information for investigation.

In the KYCentrum project, this integration layer was central to the solution. Computools worked on backend services, transaction-monitoring logic, API orchestration between internal systems and external verification services, rule-based workflows, case-management functionality, audit-trail logic, reporting logic, and secure data handling. The platform consolidated fraud alerts, KYC checks, sanctions screening, AML enrichment, and case review into a single operational flow, reducing fragmentation across fraud and compliance teams.

Result of this step: the bank has a reliable data foundation for fraud detection. The platform can connect customer behavior, transaction context, device signals, identity checks, AML results, previous alerts, and case records before rules, scoring models, and analyst workflows are added.

If fraud detection is part of a wider mobile banking product, Computools’ guide on how to build a fintech mobile app with secure banking integrations explains how secure integrations shape digital finance products.

Step 4. Set up real-time event processing

Once the data sources are connected, the platform needs to process customer actions as events. In digital banking, risk can appear during a login attempt, password reset, new device registration, beneficiary creation, transaction initiation, document upload, failed authentication, account limit change, or verification result. Each of these actions should be captured, enriched, evaluated, and either approved or escalated before the customer journey moves too far.

This is the point where real-time transaction monitoring becomes part of the banking flow. The system receives an event, adds customer and risk context, checks it against rules and scoring logic, and returns a decision. Low-risk activity can continue without friction. Medium-risk activity may trigger step-up authentication. High-risk transactions may be paused for analyst review. Critical cases may require blocking the action or restricting account activity.

The design should reflect different latency requirements. Card payments, instant transfers, and beneficiary creation usually need fast automated decisions. Onboarding, document verification, enhanced due diligence, and complex customer profile review may allow more time for checks. The platform architecture should support both types of workflows without forcing every risk decision into the same timing model.

Event processing also needs fallback logic. If a KYC provider, sanctions screening service, device intelligence tool, or internal banking service becomes unavailable, the bank needs a predefined response. Low-risk actions may continue. Higher-risk actions may be delayed, challenged, or routed to review. These rules should be documented before launch because vague fallback behavior creates operational and compliance risk.

In the KYCentrum project, Apache Kafka supported real-time transaction streaming and event processing, enabling the platform to analyze transaction activity with minimal delay. This helped the client move from delayed manual checks to risk evaluation inside active banking and compliance workflows.

Result of this step: the bank has an event-processing flow that captures relevant customer actions, enriches them with risk context, applies decision logic, and sends the appropriate response before suspicious activity becomes a confirmed loss or requires manual remediation.

Step 5. Build transparent scoring and decision logic

Once real-time events are available, the platform needs a scoring model to translate risk signals into decisions. The bank should define which signals affect risk: transaction amount, payment velocity, new recipient status, device change, unusual session behavior, failed authentication attempts, IP risk, geolocation mismatch, sanctions match, onboarding inconsistency, previous alerts, and historical customer behavior.

A strong fraud risk scoring layer helps the bank rank suspicious activity by severity. This is important because fraud teams rarely have unlimited analyst capacity. If every alert enters the same queue with the same priority, teams spend too much time on low-risk cases while high-risk activity waits. Scoring helps separate routine friction from serious operational risk.

The scoring logic should combine clear rules with contextual risk signals. Rules are useful for known patterns, such as a high-value transfer to a new beneficiary after a password reset. Contextual scoring helps evaluate less obvious combinations, such as a normal transaction amount that becomes suspicious due to changes in device, location, session, or recipient.

Explainability is essential. Analysts need to see why a score was assigned, which signals increased risk, which rule was triggered, and what data supported the decision. A score without evidence creates more work for fraud and compliance teams because they still have to reconstruct the logic manually.

In KYCentrum, the platform used fraud scoring based on behavioral, transactional, and rule-based signals. It also provided explainable decision logic for flagged transactions and customer profiles, helping compliance teams understand why each case required attention.

Result of this step: the bank has a scoring and decision layer that prioritizes suspicious activity, supports proportional responses, and gives analysts clear evidence for every flagged case.

Step 6. Add models after the rules are stable

Rules are the right starting point for known fraud patterns, but they cannot cover every changing behavior. Once the platform has reliable data, confirmed case outcomes, and stable baseline rules, the team can add models that identify anomalies, detect hidden patterns, support adaptive scoring, and help prioritize alerts.

Machine learning fraud detection works best when it supports the decision flow rather than replacing it. Rules can handle explicit policies and known scenarios. Models can detect weaker signals across transactions, devices, customer behavior, verification history, and past fraud patterns. Together, they improve detection accuracy while keeping the platform manageable for risk and compliance teams.

The bank should define how models will be trained, validated, monitored, and updated. Fraud patterns change, customer behavior changes, and model quality can degrade over time. The platform needs to be monitored for drift, false positives, missed cases, and performance changes. Without this governance, model quality can decline after launch as fraud patterns change.

Model outputs should also remain explainable. If a transaction, customer profile, or document is flagged, analysts need to understand the main factors behind the result. This is especially important when decisions affect payments, onboarding, account access, or compliance reporting.

In KYCentrum, Python-based ML models supported anomaly detection, adaptive scoring, pattern recognition, and periodic updates. The platform also included an explainable AI module that helped compliance teams understand why specific transactions, documents, or customer profiles were flagged.

Result of this step: the bank has a model layer that improves risk detection, supports evolving fraud scenarios, and remains governed, monitored, and explainable.

Step 7. Connect identity verification and compliance checks

Fraud detection becomes stronger when customer verification and compliance checks are part of the same operational workflow. Many risks appear before a transaction happens: during onboarding, document upload, liveness checks, customer profile changes, beneficiary creation, or account limit updates. If identity data sits in a separate system, fraud teams lose context during investigation and cannot connect customer risk with transaction behavior.

The platform should bring together document verification, liveness checks, sanctions screening, watchlist matching, customer risk enrichment, transaction alerts, and case review. This creates a stronger financial crime prevention layer because the bank can evaluate identity risk, transaction risk, and compliance risk in one flow instead of treating them as separate operational tasks.

The workflow should support different review paths. Low-risk customers can pass automated checks quickly. Higher-risk profiles may require enhanced due diligence, manual review, transaction limits, or additional verification. These paths should be configurable, traceable, and aligned with internal policies, so compliance teams can control the process without asking engineering to rebuild rules after every operational change.

The platform also needs to connect verification results to future transaction decisions. A failed liveness check, sanctions match, inconsistent document, risky beneficiary, or high-risk customer profile should influence later scoring and case prioritization. This creates continuity between onboarding, compliance monitoring, and fraud prevention.

In KYCentrum, Computools helped combine automated document verification, liveness checks, sanctions screening, AML enrichment, fraud alerts, case review, and compliance reporting. The unified flow reduced manual reviews, accelerated onboarding, and improved operational control for risk and compliance teams.

Result of this step: the bank has a connected identity, compliance, and fraud workflow that supports faster onboarding, stronger customer verification, and more complete risk decisions.

For lending platforms, the article on building a peer-to-peer lending platform for emerging markets can support the section on borrower verification, customer risk checks, and transaction controls.

Step 8. Build analyst workflows and investigation screens

A fraud platform only creates value if analysts can act on its output. Alerts, scores, and model results need to be translated into a workspace where teams can quickly investigate cases, understand the evidence, make decisions, and maintain a complete record of their actions.

A fraud analytics platform should give analysts access to alert priority, customer profile, transaction timeline, device and session data, verification results, triggered rules, score explanation, related accounts, case comments, evidence, escalation history, and final decision status. This context helps teams distinguish confirmed fraud from false positives without jumping across disconnected tools.

The interface should support daily fraud operations. Analysts need to filter alerts, assign cases, escalate suspicious activity, request additional checks, close false positives, prepare evidence, and document final decisions. The dashboard should focus on the evidence analysts need to make fast, consistent decisions.

Workflow design also affects compliance. Every case should have a clear timeline: when the alert appeared, which signals triggered it, who reviewed it, what decision was made, and what evidence supported the action. This record becomes important for audit preparation, internal review, and customer dispute handling.

In KYCentrum, UX design focused on investigation speed, decision clarity, and reduced cognitive load. The platform organized fraud alerts, KYC checks, AML screening, case review, and compliance reporting in one data-focused environment for fraud and compliance teams.

Result of this step: the bank has an analyst workspace that enables faster reviews, clearer decisions, reduced false-positive pressure, and better traceability across fraud and compliance cases.

Step 9. Build audit, security, and compliance controls

Compliance controls should be designed before production launch. The platform will process sensitive customer data, transaction records, identity verification results, fraud signals, analyst decisions, and audit evidence. This requires strong access control, encryption, secure API communication, logging, monitoring, incident visibility, and clear data retention rules.

As banking compliance software, the platform should help teams prove how risk decisions were made. Compliance officers need to see which data was used, which rule or score triggered the alert, who reviewed the case, what action was taken, and whether the process followed internal policy and regulatory requirements.

Audit readiness depends on traceability. Each transaction alert, KYC check, AML screening result, analyst comment, decision change, escalation, and final resolution should be recorded. Without this record, the bank may detect suspicious activity but still struggle to explain its own actions during review. A system that cannot explain itself is not a compliance asset; it creates review gaps and weakens audit readiness.

Security should also cover operational resilience. The platform needs monitoring, incident logging, access reviews, secure key handling, and controlled integrations with external services. These controls reduce exposure when the system exchanges data with KYC providers, AML tools, payment systems, and internal banking infrastructure.

In KYCentrum, the platform supported audit trails, compliance-ready reporting, explainable decision logic, secure data handling, TLS 1.3, HSM key management, Azure Monitor, and Microsoft Sentinel. The client also improved audit readiness through complete traceability and centralized records for fraud and KYC workflows.

Result of this step: the bank has a platform that supports fraud prevention, regulatory review, secure operations, and traceable decision-making from the first release.

Step 10. Launch in phases and improve the platform continuously

A fraud platform should be delivered in controlled stages. The bank can start with the highest-risk scenarios, connect the most important data sources, build baseline rules, validate event flows, add scoring, test analyst workflows, and then expand coverage across more products, channels, and risk types.

Fraud detection software engineering should include technical, operational, and compliance validation. The team needs to test event-processing speed, rule accuracy, model behavior, KYC and AML integrations, analyst workflows, audit trail consistency, access control, monitoring, and incident handling. A rushed launch can create new risks rather than reduce existing exposure.

The rollout should also include measurable KPIs. Important metrics include confirmed fraud rate, false-positive rate, alert volume, manual review rate, average case resolution time, onboarding time, decision latency, model drift, blocked fraud value, and analyst workload. These indicators help teams understand whether the platform improves fraud prevention without creating unnecessary friction for legitimate customers.

After launch, the platform should be adjusted continuously. Rules need updates, models need monitoring, new fraud scenarios need coverage, and analysts need better workflows as case volumes change. Feedback from confirmed fraud, false positives, manual reviews, customer support, and compliance checks should be returned to the platform roadmap.

In KYCentrum, Scrum supported iterative delivery of ML models, streaming pipeline components, verification modules, and investigation dashboards. This phased rollout helped the client validate fraud, KYC, compliance, and analyst workflows before scaling the platform further.

Result of this step: the bank has a controlled rollout plan, measurable fraud and compliance KPIs, and a feedback loop for improving detection accuracy, analyst productivity, and regulatory readiness.

What features should a real-time fraud detection platform include?

A real-time fraud detection platform should combine automated risk evaluation with tools for analyst review, compliance control, and continuous improvement.

The core feature set usually includes:

1. Real-time event capture

The platform should capture customer and transaction activity as it happens: logins, password resets, beneficiary creation, payments, onboarding actions, authentication attempts, document uploads, and customer profile changes.

2. Transaction and customer data enrichment

Each event should be enriched with customer history, device signals, IP and location data, authentication status, recipient information, KYC results, AML checks, and previous case outcomes.

3. Scoring engine

A fraud scoring engine converts risk signals into a clear score or risk level. This score helps the bank decide whether to approve the action, request step-up verification, delay the transaction, send it for review, or block the operation.

4. Customer behavior analysis

Behavioral analytics for fraud detection helps the platform compare current activity with normal customer behavior. A transaction may look harmless on its own, but become suspicious after a new device login, an unusual navigation pattern, the creation of a new beneficiary, or a sudden change in payment frequency.

5. Cross-channel transaction control

Suspicious transaction monitoring should cover cards, transfers, account changes, onboarding, lending, and customer profile updates. A unified view helps teams detect connected risk patterns instead of reviewing each event separately.

6. Anomaly detection

Anomaly detection in banking helps identify unusual patterns that static rules may miss, especially when fraud behavior changes quickly or depends on several weak signals appearing together.

7. Configurable rule engine

Risk teams should be able to adjust thresholds, add rules, change escalation logic, and test new fraud scenarios without waiting for a full development cycle.

8. Case management workspace

Analysts need a clear workspace with alert priority, customer profile, transaction timeline, verification results, triggered rules, risk explanation, related accounts, comments, evidence, escalation history, and final decision status.

9. Audit trails and explainable decisions

Every alert, score, rule trigger, analyst action, and final decision should be traceable. This supports compliance review, internal audits, customer disputes, and regulatory reporting.

10. Dashboards and performance reporting

The platform should show fraud trends, alert quality, false positives, review workload, onboarding impact, case resolution speed, and compliance performance.

Launch your real-time fraud detection platform within 1–3 months instead of years, and stop fraud before it impacts customer trust, revenue, and brand reputation.

What compliance and security controls should a fraud detection platform include?

A digital banking fraud detection platform handles sensitive customer data, payment records, identity documents, risk scores, analyst comments, and compliance decisions. Security and compliance controls must be set before launch, as the platform impacts live financial operations and may later require internal reviews, audits, incident investigations, and regulatory reports.

A strong financial fraud detection solution should include role-based access control, strong authentication, encryption in transit and at rest, secure API communication, audit logs, data retention rules, and controlled access to case records. These controls help protect customer and transaction data across banking systems, KYC providers, AML tools, payment infrastructure, and analyst workspaces.

Traceability is just as important as detection accuracy. Compliance teams need to see which data was used, which rule or model influenced the score, who reviewed the case, what action was taken, and how the final decision was recorded. This is especially important when a transaction is delayed, a customer is challenged, or an account action is restricted.

Explainability should also be treated as a compliance requirement. Analysts need visible risk signals, triggered rules, model explanations, verification results, and case history in one place. If the system flags an action but cannot explain why, the bank may still face delays, review gaps, and customer disputes.

In the KYCentrum project, Computools supported secure data handling, audit trails, compliance-ready reporting, explainable decision logic, TLS 1.3, HSM key management, Azure Monitor, and Microsoft Sentinel. These controls helped the client keep fraud and KYC workflows traceable, secure, and ready for internal or external review.

For broader security planning, read Computools’ article on how to implement enterprise cybersecurity for financial services companies, which explains how financial organizations can protect customer data, reduce operational risk, and meet regulatory requirements.

How should banks measure the performance of fraud detection platforms?

A fraud detection platform should be measured by its impact on fraud risk, analyst workload, customer experience, and compliance operations. More alerts do not always mean better protection. A strong banking fraud prevention platform should help teams detect real fraud faster, reduce false positives, and keep legitimate customer activity moving with less friction.

| Metric | What to track |

| Confirmed fraud rate | Whether actual fraud cases decrease after the launch |

| False-positive rate | How often is legitimate customer activity flagged |

| Alert volume | How many alerts does the platform create for analysts |

| Manual review rate | How many cases still require human investigation |

| Case resolution time | How quickly do teams close fraud and compliance cases |

| Onboarding time | Whether automated checks speed up customer verification |

| Decision latency | Whether risk decisions are fast enough for live banking flows |

| Model drift | Whether scoring quality changes as fraud patterns evolve |

| Operational compliance cost | Whether automation reduces manual review and reporting work |

| ROI timeline | When the platform starts creating measurable business value |

False positives and decision latency deserve special attention. If the system flags too many legitimate transactions, analysts lose time, and customers face unnecessary friction. If scoring is accurate but too slow, the platform still fails the business process.

Why choose Computools for fraud detection platform development?

For fraud detection projects, Computools’ value should be measured by business impact: lower fraud exposure, fewer false positives, faster verification, lower compliance workload, and faster ROI. In KYCentrum, these outcomes were already measured across fraud and compliance operations.

| Client priority | Result achieved in KYCentrum |

| Reduce fraud exposure | 41% fewer confirmed fraud cases |

| Improve alert quality | 52% fewer false-positive alerts |

| Speed up verification | 50–60% shorter customer onboarding |

| Increase compliance productivity | 63% faster case resolution |

| Lower compliance workload | 20–30% lower operational compliance costs |

| Prove value faster | ROI within 6 months |

These results show how Computools ties fraud platform delivery to operational KPIs, not only technical output. Through financial software development services, Computools can help turn fragmented fraud, KYC, AML, and reporting workflows into a controlled platform with measurable KPIs, phased delivery, and clear operational checkpoints.

For fintech companies, fintech software development should support fraud prevention before transaction volumes become difficult to manage manually. Wallets, lending platforms, neobanks, payment products, and embedded finance solutions need automated risk checks, fast customer verification, scalable review workflows, and clear reporting from the early stages of growth.

Computools also connects product usability with fraud operations. Through web development services, the team can build analyst dashboards, case review workspaces, admin panels, and reporting views that help risk and compliance teams work faster, review evidence clearly, and reduce manual switching between tools.

For AI fraud detection in banking, Computools can support adaptive scoring, anomaly detection, explainable risk signals, and model monitoring. In practice, this connects AI work to business metrics: higher fraud-detection accuracy, fewer false positives, faster analyst decisions, and stronger control over evolving fraud patterns.

For clients, this means a lower-risk delivery model: start with the most critical fraud and verification workflows, validate data flows, test decision logic, track agreed KPIs, and expand the platform after the first operational scenario proves value.

Contact Computools at info@computools.com to discuss how a real-time fraud detection platform can reduce fraud risk, false positives, manual compliance work, and onboarding delays in your digital banking operations.

Conclusion

A real-time fraud detection platform gives banks and fintech companies a controlled way to detect risky activity before it becomes a confirmed loss. The strongest systems combine transaction monitoring, fraud scoring, behavioral analytics, AI models, analyst workflows, audit trails, and compliance controls into a single operational flow.

For digital banking teams, this means faster risk decisions, fewer false positives, lower manual workload, and stronger control over fraud, KYC, AML, and reporting processes.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.