THE AUTHOR:

Banks and FinTech companies now need to build an AML transaction monitoring system because financial activity has moved into faster, more fragmented, and higher-risk digital environments. Not long ago, payments moved through straightforward channels. Now, they flow through a multitude of services including mobile banking apps, digital wallets, cards, instant transfers, various embedded finance products, investment apps, marketplace payouts, crypto finance and cross-border payment services.

Anti money laundering monitoring can no longer afford to rely on delayed reviews, disconnected data on spreadsheets, or static rules that result in a barrage of low-value alerts for analysts.

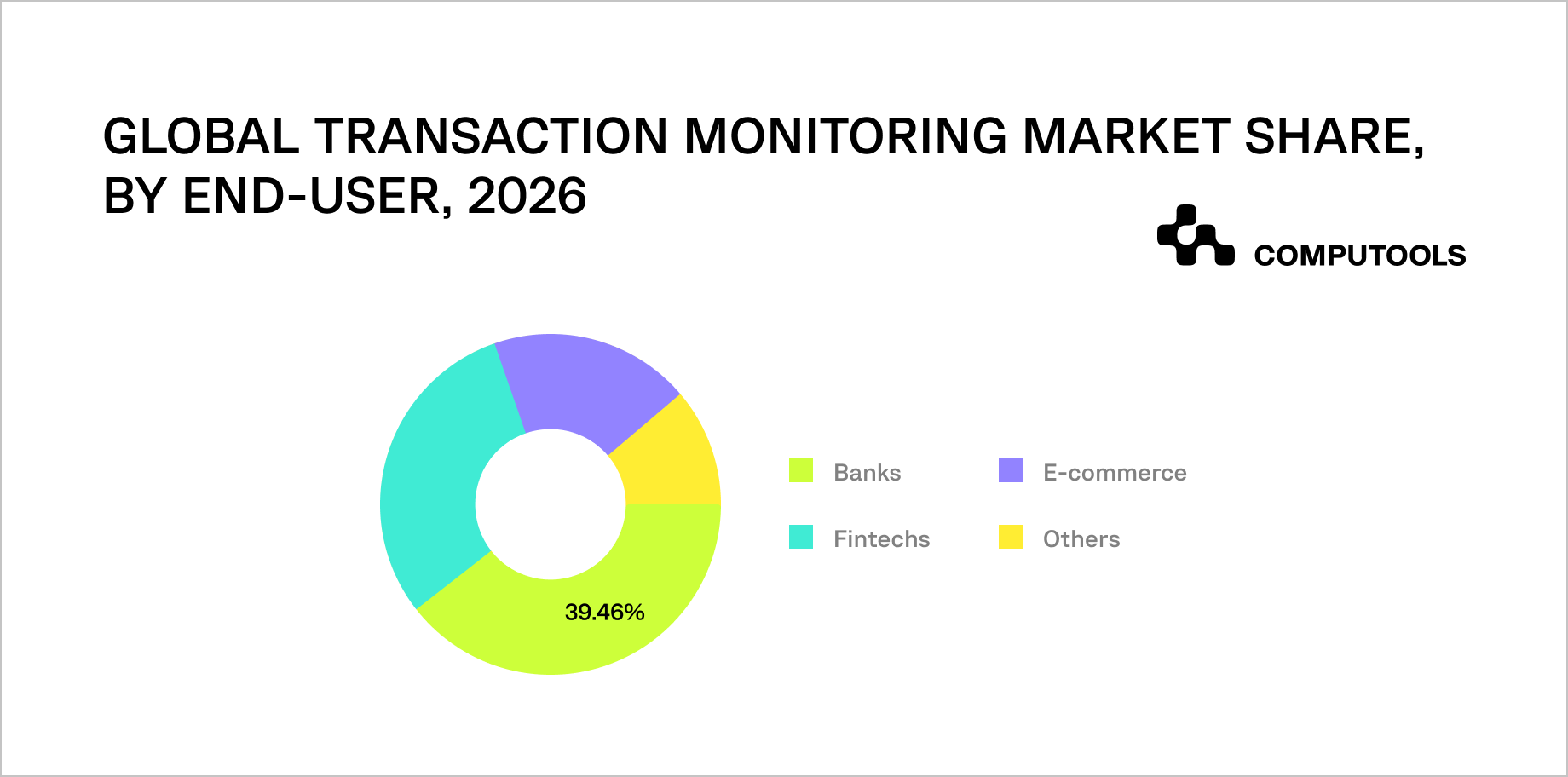

Market data demonstrates the massive investment shift. Fortune Business Insights evaluated the global transaction monitoring market at USD 20.27 billion by 2025, growing from USD 22.98 billion in 2026 to USD 62.44 billion in 2034, at a CAGR of 13.30%.

In 2025, North America was home to 37.26% of the global market due to an effective legal framework, high transaction volume, and a greater level of AI, machine learning, and big data techniques. The report goes on to say that in 2026, cloud computing will represent 75.63% of the market, and of that, the AML application market will represent 34.10%.

Technical pressure is rising just as fast. Cybercrime, phishing, identity crime, digital transaction authentication, fraud in digital payments and cryptocurrencies, and the growing use of mobile wallets represent critical market drivers. Most legacy systems fail because of the latency in reviewing activity, large margin thresholds, and a lack of customer context necessary in assessing risk.

Modern financial crime detection software needs to process high transaction volumes and enhance each event with KYC and customer data, perform a risk assessment in real time, and identify shifts in behavior while creating audit-ready documentation and presenting clear findings to support investigations.

What features should an AML transaction monitoring system include?

| Market driver | What it means for banks and FinTechs | Platform features and functionality it should influence |

| Rising SAR/STR volumes and stronger AML/CFT enforcement | Compliance teams must handle more reports, larger alert queues, and stricter expectations around investigation quality. | Automated alert triage, case prioritization, SAR/STR workflow support, SLA tracking, immutable audit logs, rule trigger history, and decision records. |

| Banks expected to hold 39.46% of the market in 2026 | Banks need monitoring systems that reduce fraud and regulatory exposure without damaging customer experience. | Core banking integrations, real-time risk checks, high-risk account prioritization, compliance reporting, role-based dashboards, and customer profile enrichment. |

| Real-time payments and rising cybercrime | Instant payments, phishing, identity theft, account takeover, and transaction tampering reduce the time available for manual review. | Low-latency risk scoring, real-time approve/flag/hold/reject logic, device intelligence, velocity checks, event streaming, and fallback review flows. |

| E-commerce expected to grow at a CAGR of 17.17% | Digital commerce increases exposure to fraudulent purchases, refund abuse, account misuse, and payment manipulation. | Merchant risk scoring, payment behavior analytics, buyer and seller protection workflows, fraud detection, and marketplace payout monitoring. |

| Growth of cryptocurrency and digital asset payments | Standard payment monitoring may miss risks linked to wallets, anonymous transfers, and digital asset flows. | Crypto transaction screening, wallet risk scoring, blockchain analytics integration, counterparty checks, and digital asset-specific monitoring rules. |

| Cross-border AML requirements | Companies operating across regions need controls that support multiple jurisdictions, payment rails, currencies, and reporting standards. | Multi-currency monitoring, jurisdiction risk scoring, sanctions and PEP screening, country-specific rules, cross-border payment transparency, and configurable compliance logic. |

| Behavioral biometrics and stronger identity-based monitoring | Identity signals are becoming part of transaction risk evaluation, especially in mobile banking and online payments. | Device fingerprinting, typing and touch behavior signals, session risk scoring, customer risk profiles, KYC enrichment, and account takeover detection. |

| AI adoption in transaction monitoring | Banks and FinTechs need faster detection across large datasets while cutting down on false positives. | ML-based anomaly detection, behavioral baselines, adaptive risk profiles, alert prioritization, explainable AI, and AI-assisted investigation summaries. |

| ESG and transaction-attribute risk scoring | Risk evaluation is expanding beyond transaction amount and location into broader customer, business, and counterparty context. | Multi-factor risk scoring, customer segmentation, business activity profiling, counterparty attributes, and configurable risk models. |

| Cloud deployment expected to capture 75.63% of the market in 2026 | Companies want faster deployment, remote access, continuous updates, and lower IT infrastructure friction. | Cloud-native or hybrid architecture, autoscaling, secure access, monitoring, backup, and zero-downtime updates. |

The most important question facing decision-makers is how to build an AML transaction monitoring system that enables growth without increasing compliance costs.

This article explains how to approach that platform strategically: what the business should decide first, which architecture choices matter, how data and AI affect detection quality, where integrations create operational value, and how Computools supports banks and FinTech companies in building AML platforms that reduce risk while improving scalability and control.

For financial companies planning broader risk controls, Computools also explains how to implement enterprise cybersecurity for financial companies across data, access, infrastructure, and compliance workflows.

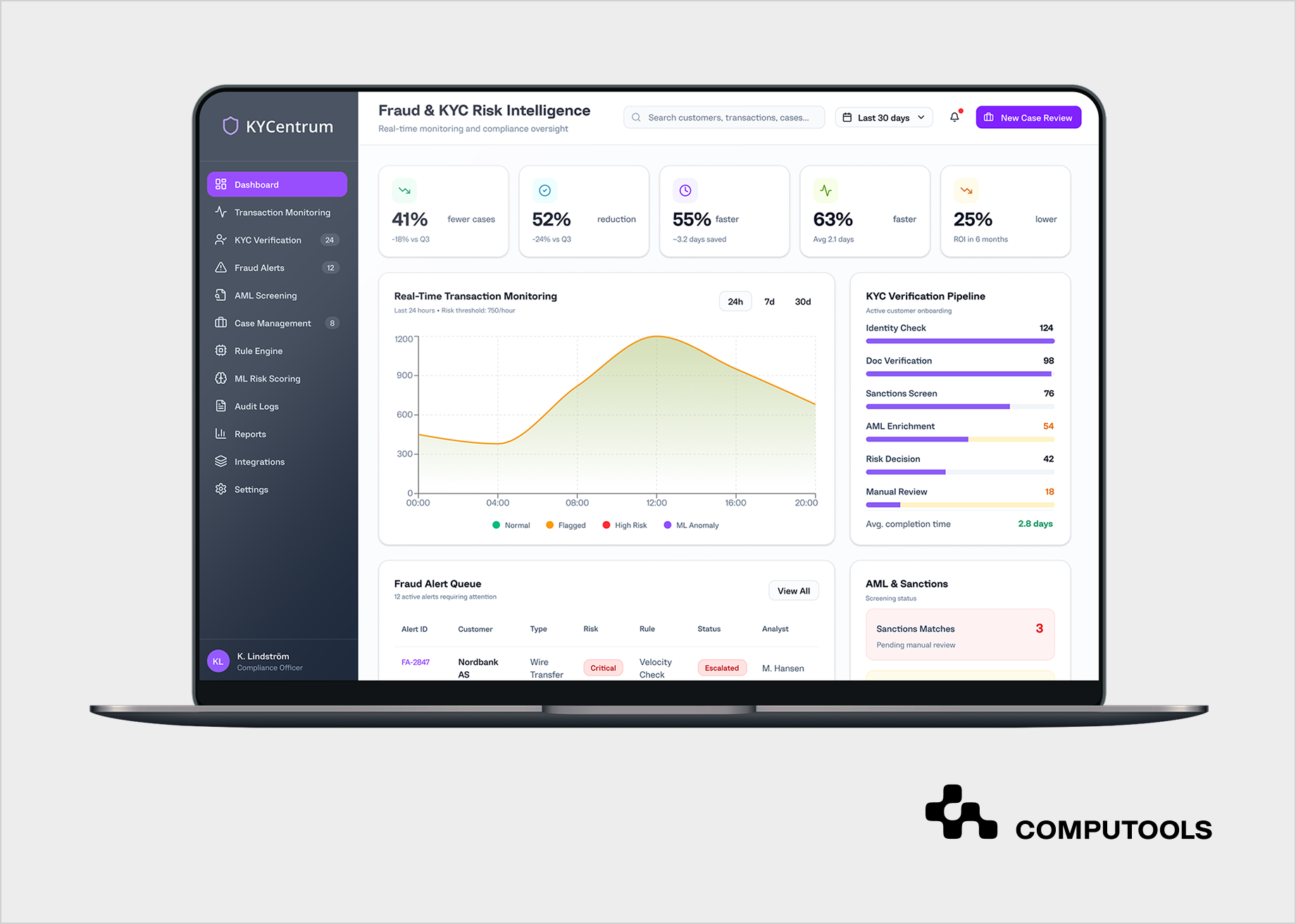

Build an AML transaction monitoring system with real-time risk control: KYCentrum example

A relevant case is KYCentrum, a fraud-prevention and compliance application we developed for a European financial services provider operating in Estonia, Latvia, and Lithuania. The client worked with private and business customers in banking, payments, cards, loans, leasing, savings and pensions, as well as investments and private banking. With the rising digital activity, the company required stronger control for fraud prevention, customer verification, AML checks, and compliance reporting.

The core business issue was fragmentation. Fraud detection was mainly based on static rules and relied on manual reviews. Analysts’ involvement in the KYC process was excessive. The compliance teams had to work with different tools to review alerts, perform document verification, check sanctions, prepare cases, and create an audit log.

All these significantly impacted service speed for client onboarding, increased operational expenses, and generated pressure on the risk and compliance teams.

Computools built a solution integrating real-time transaction monitoring, automated KYC, rule-based decisioning, ML-supported fraud scoring, anomaly detection, sanctions screening, AML case management, and audit reporting. The platform’s architecture was designed around the live processing of data with built-in workflows for regulatory compliance. This enabled analysts to assess flagged cases with the contextual information instead of evidence gathered through multiple, disconnected systems.

The technical stack supported both speed and control. Java and Spring Boot powered backend services, business logic, API orchestration, case workflows, and integrations. Python-based ML models supported anomaly detection, adaptive fraud scoring, and pattern recognition. Apache Kafka enabled real-time transaction streaming and event processing, allowing suspicious activity to be evaluated with minimal delay. PostgreSQL stored customer verification records, fraud events, decision logs, structured case data, and audit trails. A configurable rule engine supported fraud and compliance logic, while an explainable AI module showed why specific transactions, documents, or customer profiles were flagged.

Security and operational visibility were also part of the solution. TLS 1.3 and HSM key management protected sensitive customer and transaction data. Azure Monitor and Microsoft Sentinel support system monitoring, incident logging, and resilience tracking.

The business results were measurable. The platform reduced confirmed fraud cases by 41%, lowered false-positive alerts by 52%, shortened customer onboarding time by 50–60%, and made compliance case resolution 63% faster. Operational compliance costs also decreased by 20–30%, with ROI reached within six months.

The same logic applies when banks and FinTech companies build platforms that connect live transaction data, KYC, risk scoring, analyst workflows, ML reporting and audit trails into one controlled environment.

How to develop an AML transaction monitoring system step-by-step

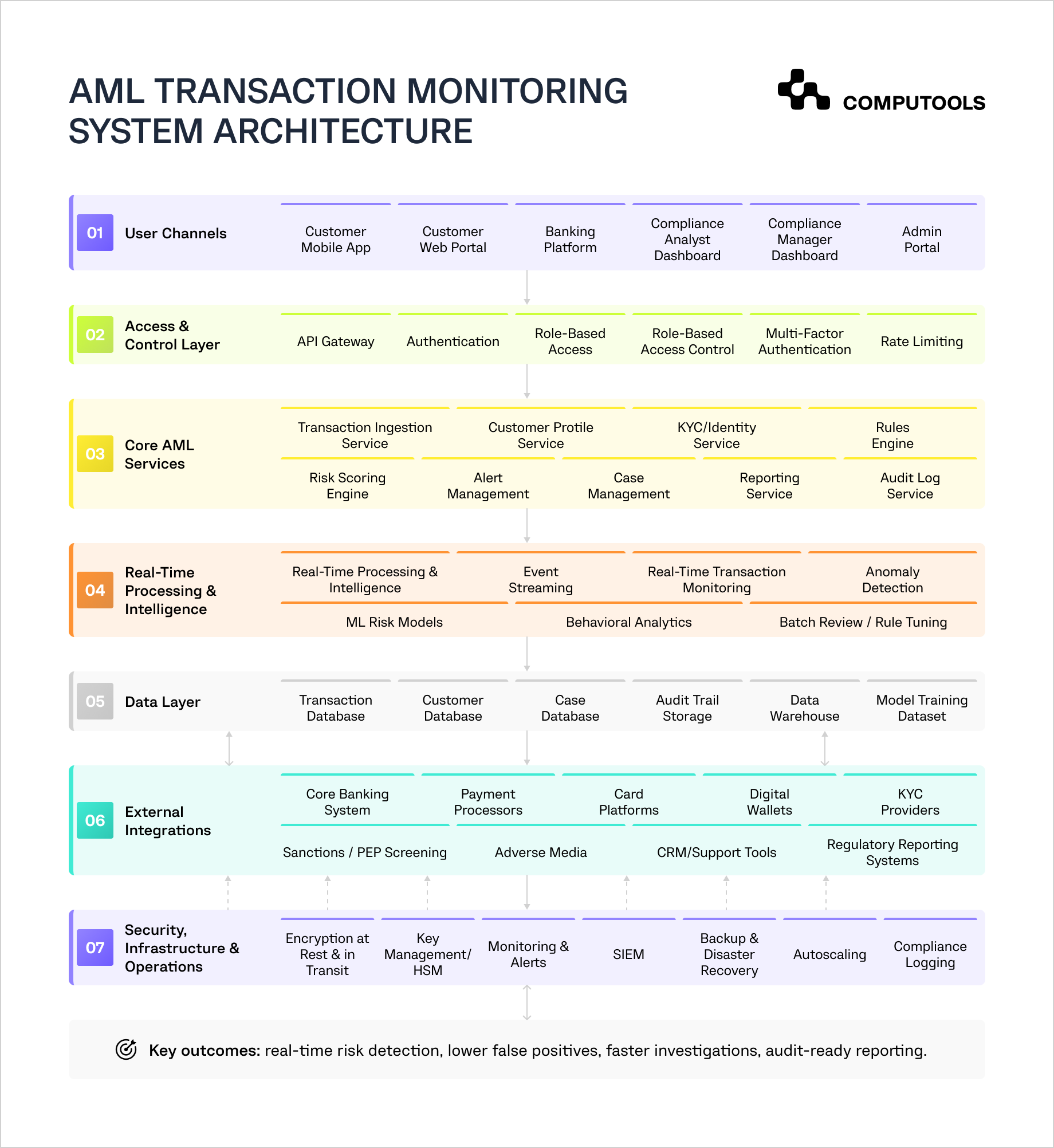

To build an AML transaction monitoring system that works in real banking and FinTech environments, the project should start with operational design. The platform has to know what transactions to monitor, what business risks are important, how alerts progress through the compliance teams, and how each decision will be captured for audit purposes. The solution has to be flexible enough to adjust to new products, regulations, fraud, and the volume of transactions.

1. Define the AML Operating Model First

Before deciding on the architecture or the features, the business has to decide what the AML platform is going to protect. A retail bank, a fintech lending business, a payment service provider, a digital wallet, a marketplace, and an embedded finance platform will all provide a different set of risk profiles.

Transaction monitoring for banks will focus on account activity, transfers, deposits, withdrawals, cash movements, and high-risk counterparties. FinTech transaction monitoring solutions often need to control faster payment flows, merchant payouts, wallet transfers, card activity, refunds, and multi-party transactions.

This decision matters because AML rules should reflect the company’s real operating model. A marketplace that pays sellers daily needs different suspicious transaction monitoring logic than a bank that serves corporate clients. A lending platform may need to monitor unusual repayment patterns, loan stacking, synthetic identity risks, and account takeover signals.

In practice, the team should define monitored entities such as customers, accounts, wallets, cards, merchants, beneficiaries, devices, counterparties, and transactions. Then the system should map expected behavior for each segment. For example, a corporate customer may process larger payments regularly, while the same volume from a newly onboarded retail customer may require review.

When this step is ignored, the AML compliance software often becomes too generic. It flags too much, misses business-specific risks, and forces analysts to manually interpret cases without enough system context.

If your product roadmap includes investment accounts, portfolio tools, or wealth management features, read Computools’ guide on how to build an investment management platform with secure data flows, user roles, reporting, and financial operations in mind.

2. Build a Data Model Around Customers, Transactions, Risk, and Cases

An AML risk detection platform is focused on the structure of the data it collects. For most use cases, a plain transaction record does not have enough context to determine suspicious activity. The system must relate the transaction details to the customer profile, KYC status, device signals, counterparty data, sanctions screening results, past alerts, case history, and the decisions made by the analysts.

The central data model should consist of customer profiles, accounts/wallets, transactions, counterparties, KYC data, risk scores, alerts, investigative cases, actions of investigators, history of escalations, and audit logs. Each record should provide clear ownership, be timestamped, have status changes, and contain references to related events.

For example, if a customer changes a beneficiary and sends several high-value payments within minutes, the platform should connect those events instead of treating them as separate records. If several accounts share a device, address, card, or beneficiary, the system should make those connections visible to investigators.

The data model should also support AML reporting and audit trails. It should retain every rule trigger, score change, manual override, case note, escalation, and decision. This protects the business during internal review and regulatory checks.

In the KYCentrum project, Computools used structured storage for customer verification records, fraud events, decision logs, case data, and audit trails. The same principle applies to AML software development because compliance teams need traceable evidence, not scattered records.

3. Design Real-Time Transaction Monitoring Logic

Real-time transaction monitoring is essential for rapid payments, digital wallets, card transactions, instant transfers, marketplace payouts, and cross-border payments. While some transactions can be reviewed retrospectively, the system has to score, pause, escalate, or perform a step-up verification on high-risk transactions immediately.

The algorithms need to determine which events can be evaluated in real time versus those that can be reviewed in near real time or batch processed. This affects the user experience and exposure to fraud, the costs incurred to operate the system, and the burden of compliance.

A real-time transaction flow may look like this: a transaction record is created, checked on KYC and customer data. After that, sanctions and watchlist screening occurs, followed by rules evaluation and risk scoring. The system can approve, flag, or place the transaction on hold, or decide to escalate verification, reject the transaction, or create a case for a manual review.

The risk logic requires an assessment that considers transaction details (amount, velocity, frequency, and geography), customer account profiling (age and device changes), beneficiary and customer segmentation, previous alerts, and counterparty risk.

If real-time logic is too weak, suspicious funds may leave the system before review. If it is too aggressive, legitimate customers face unnecessary blocks, support tickets increase, and revenue flow slows down. The platform should balance control with business continuity.

4. Combine Rules, Transaction Risk Scoring, and Explainable AI

AML systems still need rule-based detection. Rules are useful for known typologies, regulatory thresholds, jurisdiction risk, transaction limits, velocity checks, and clear business policies. However, rules alone often create high false-positive volumes because they cannot always understand behavioral context.

Transaction risk scoring adds more precision. Instead of treating every trigger equally, the system can assign weighted scores based on customer profile, transaction behavior, geography, counterparty, account history, KYC status, device signals, and previous cases. This gives analysts a clearer way to prioritize alerts.

AI can support suspicious activity detection when the data foundation is ready. It can identify unusual behavior, detect patterns across linked entities, prioritize alerts, support customer segmentation, and suggest investigation summaries. For example, a model can identify that a merchant’s payout behavior changed sharply after a period of stable activity, even if no single transaction breaks a fixed rule.

AI should remain explainable in AML workflows. Compliance teams need to understand why the system flagged an event. A useful alert should show the trigger logic, risk factors, related transactions, linked entities, and supporting evidence. Clean, structured data is essential. If customer records are duplicated, KYC fields are missing, or transaction categories are inconsistent, AI will produce weak results.

In the KYCentrum platform, Computools combined rule-based decisioning with ML-supported fraud scoring and anomaly detection. This balance matters because AML automation should improve analyst focus without removing control from compliance teams.

5. Connect KYC, AML, Sanctions Screening, Payments, and Core Systems

KYC and AML integration is one of the most important design decisions. AML monitoring becomes weaker when customer verification, transaction data, sanctions screening, payment processing, and case management are separated.

The platform must interface with existing systems that govern customer identities and the movement of funds. Examples include core banking systems, payment processors, card platforms, digital wallets, lending platforms, merchant systems, CRM, KYC providers, document verification tools, liveness checks, sanctions screening, PEP lists, adverse media databases, data warehouses, BI tools, and regulatory reporting systems.

Regarding technical design, secure APIs, data validation, and other methods of fallbacks and fail-safes should be implemented. Should a sanctions provider become unavailable for a time, the platform will queue the event for sanctions, mark it, and change the risk status accordingly. Should a KYC provider returns insufficient data, the platform will send the customer or transaction to the appropriate review.

This step directly affects operations. Strong integrations reduce manual checks, improve alert context, and prevent analysts from moving between several systems to build one case. Weak integrations create blind spots, duplicate work, and inconsistent decisions.

For a closer look at mobile banking architecture and third-party financial integrations, read Computools’ guide on how to build a FinTech mobile app with banking integrations.

6. Build AML Alert Management and Investigation Workflows

Detection represents just a single component of the system. Effective AML alert management ensures that compliance teams have both the authority and capability to act in a timely and uniform manner. Without an adequate AML investigation workflow, even the most diligent compliance teams still face operational challenges from the increased volume of detected alerts.

Adequate workflows for AML investigations should contain alert queues, severity ratings, reason codes, snapshots of customer profiles, transaction histories, and timelines, counterparty views, linked alerts, case notes, evidence, investigator assignments, and escalation paths. Additionally, the workflows should contain SLA indicators and tracking, as well as case decision documentation.

AML investigation workflows should be designed with compliance team operational hierarchies and roles in mind. For example, junior analysts may be tasked with reviewing low-risk alerts, whereas compliance managers may be responsible for clearing escalations or signing off on SARTs.

AML teams have historically demonstrated their ability to design custom workflows when a systems vendor fails to meet their needs. Unfortunately, the use of custom workflows designed outside of the system results in extremely poor audit records and increased friction to achieving case resolution.

Detection is only a facet of a system. AML alert management addresses whether or not compliance teams can act in a timely manner, uniformly, and decisively. Without an adequate AML investigative workflow, even valid alerts can become operational burdens.

The system in question must offer alert backlogs, severity levels, reason codes, customer snapshots and timelines, counterparty and transaction data, evidence notes, linked alerts, investigator assignments and escalation paths, SLA tracking, and final decisions. Analysts must understand the context of an alert, which data justifies an alert, and what actions are necessitated.

The workflow must be designed with roles in mind. Junior analysts may deal with low complexity and low risk alerts, while advanced cases may be dealt with exclusively by a Senior Investigator. Compliance Managers may be authorized to approve investigative escalations and suspicious activity reports, while auditors may only be given view access to case data and evidence.

If this workflow is ignored, teams often move investigations into spreadsheets, email threads, or separate ticketing systems. That slows resolution, increases inconsistency, and creates weak audit records.

7. Design Security, Access Control, and Reliability Into the Platform

AML Platforms deal with a wide array of sensitive data. Integrated security helps protect trust, revenue, and the system stability.

The architecture should contain encryption in transit and at rest, secure key management, role-based access control, multi-factor authentication, privileged access controls, session monitoring, secure API gateways, data masking, immutable audit logs, and environment separation. Administrative actions should be logged and reviewed.

Reliability is a concern as well. If transaction ingestion fails, the business is unaware of suspicious activity. If alert routing fails, the analysts will not see the alerts. If a third-party KYC or sanctions provider is down, the system should have some automation to replenish the queue and provide a default processing status.

The architecture should have support for queue processing, autoscaling, handling of repeated operations, dead letter queues, and the standard backup and recovery practices. Teams should monitor the system for latency, checks that have failed, delayed responses from providers, alert spikes, the backlog of cases, and data ingestion failures.

Security and reliability are business controls. They reduce fraud exposure, protect customer trust, lower support pressure, and keep compliance operations stable when transaction volume grows.

8. Test, Tune, and Improve the System After Launch

AML transaction monitoring requires regular adjustment to maintain accuracy. Customer behaviors change, fraudulent activities evolve, product lines expand, and regulations get updated. Systems need to anticipate these changes and be designed for ongoing improvement from the outset.

There are many aspects to be tested for system performance. These include the logic for rule interpretation, transaction processing, risk scoring, false-positive generation, alert distribution, case management workflows, access management, reporting and audit trails, system integrations, load handling, and high-volume transaction scenarios. Add to the list provider problems, event duplication, late event reporting, intermittent KYC responsiveness, and manual changes.

Business operations must be monitored post-deployment. Alert generation, false-positive reports, average case closure, SLA performance, fraud activity and trends, risk assessment and evaluation gaps, quality of transaction blocks, analyst workload, and accuracy of reports must be considered. These metrics show whether the platform improves operations or adds more complexity.

Rules should be tuned based on real investigation outcomes. ML models should be reviewed and retrained with confirmed cases. Segmentation should improve as more customer behavior data becomes available. Repetitive analyst actions should be automated where possible.

A strong AML automation platform becomes more accurate over time. It gives compliance teams better focus, gives executives clearer risk visibility, and gives the business a scalable foundation for new products, markets, and transaction channels.

Many banks also need AML modernization to work with older infrastructure. Computools explains how to modernize legacy banking systems without downtime while keeping critical operations stable.

Launch your AML transaction monitoring system within 1–3 months instead of years, and start detecting risk, automating compliance workflows, and scaling with confidence from day one.

Why choose Computools to build an AML transaction monitoring system

Banks and FinTech companies benefit from AML transaction monitoring when it cuts down on manual reviews, reduces false positives, increases detection accuracy, and gives compliance teams faster control over suspicious activity. Computools designs AML platforms around these outcomes, not isolated compliance features.

Computools connects transaction data, customer profiles, KYC results, sanctions screening, risk scoring, investigation workflows, reporting, and audit trails into one controlled environment. This reduces fragmented checks, increases analyst productivity, and gives leadership clearer visibility into financial crime risk.

Banks benefit from Computools’ banking software development services when they need secure core integrations, real-time transaction processing, access control, and audit-ready reporting. Financial organizations use Computools’ financial software development services to connect AML monitoring with onboarding, payments, customer operations, analytics, and executive reporting.

FinTech companies benefit from Computools’ fintech software development experience when they need scalable transaction controls for wallets, lending products, marketplaces, embedded finance, and high-volume payment flows. Computools builds the backend logic, integrations, and risk workflows needed to support faster product growth without losing compliance control.

The KYCentrum case shows this in practice. Computools connected real-time transaction monitoring, automated KYC verification, rule-based decisioning, ML-supported fraud scoring, anomaly detection, case management, and audit trails. The client reduced confirmed fraud cases, lowered false-positive alerts, shortened onboarding time, increased case resolution speed, and cut operational compliance costs.

Computools also strengthens the technical layers around the platform. Its web development services support analyst dashboards, admin panels, customer verification flows, and reporting interfaces. AI development improves anomaly detection, transaction risk scoring, alert prioritization, investigation summaries, and customer segmentation. Cybersecurity services protect customer data, transaction records, access rights, and investigation history.

Computools builds AML transaction monitoring systems that cut down on operational bottlenecks, increase fraud detection accuracy, protect revenue flow, and support audit readiness as banks and FinTechs scale.

If your team is comparing potential technology partners, Computools’ overview of the top FinTech software development companies can also support vendor research and selection.

Final thoughts

To build an AML transaction monitoring system that facilitates the growth of banks and FinTech firms, rules engines and compliance dashboards are insufficient. A monitoring system must combine transaction data with customer details, KYC results, sanctions screening, risk scoring, alert management, investigations, and audit trails into a single operating layer.

This approach to banking compliance software development enables staff to gain access to evidential data faster and reduces frequent reviews. This also leads to improved suspicious activity detection, active control of the risk of financial crime, and allows senior management to view the active cost of compliance, the potential exposure to fraud, the speed of customer onboarding, and the quality of reports.

Robust AML systems are designed to improve continuously. The platform has to be able to handle greater transaction volume and not slow down legitimate activity or generate excessive alerts.

Fragmented data, excessive false positives and manual investigations should not be the blockers to growth. Connect fraud detection, KYC, transaction risk scoring, and investigation workflows into one operational platform with Computools. Talk to our team at info@computools.com.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.