THE AUTHOR:

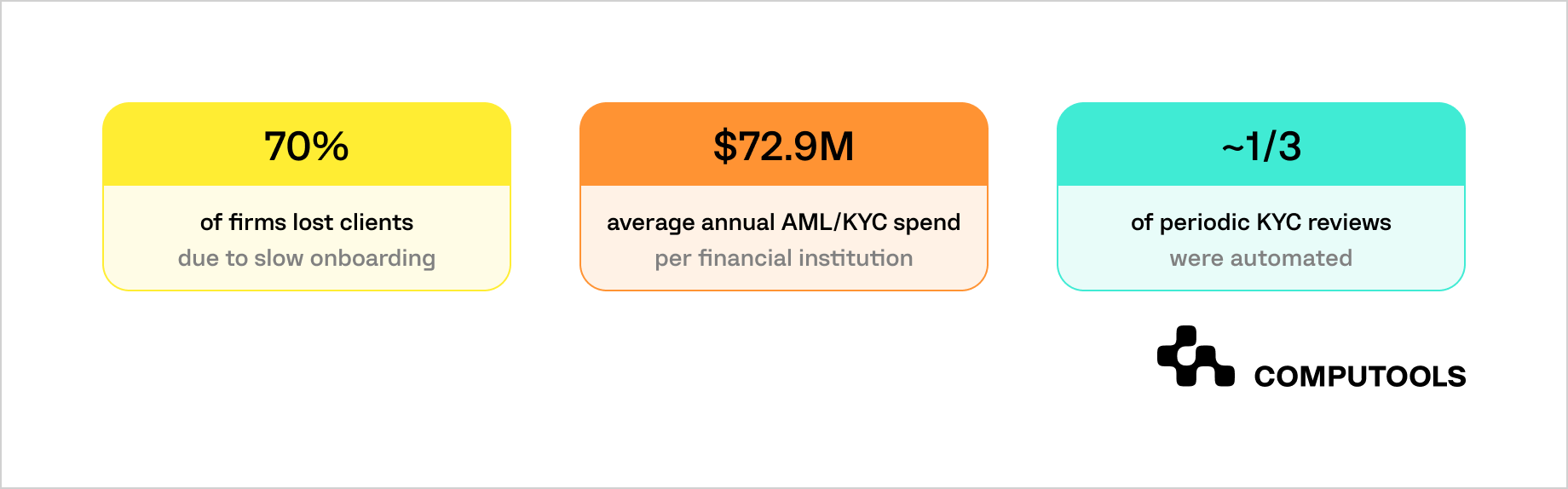

Fragmented and manual KYC workflows increase onboarding time, compliance workload, and customer drop-off. According to Fenergo’s 2025 survey of 600 senior decision-makers, 70% of surveyed financial institutions had lost clients because of slow onboarding, while average annual AML and KYC operating costs reached $72.9 million per institution. The same research found that automation covered only about one-third of periodic KYC reviews, leaving compliance teams responsible for recurring checks, exception handling, and evidence preparation.

To develop an automated KYC verification system, financial institutions need to integrate identity data collection, document and biometric verification, sanctions screening, customer risk assessment, analyst review, and audit records into a single controlled workflow. The platform should reduce manual processing while preserving decision transparency, security, regulatory traceability, and clear escalation paths for high-risk cases.

How Computools helps develop an automated KYC verification system

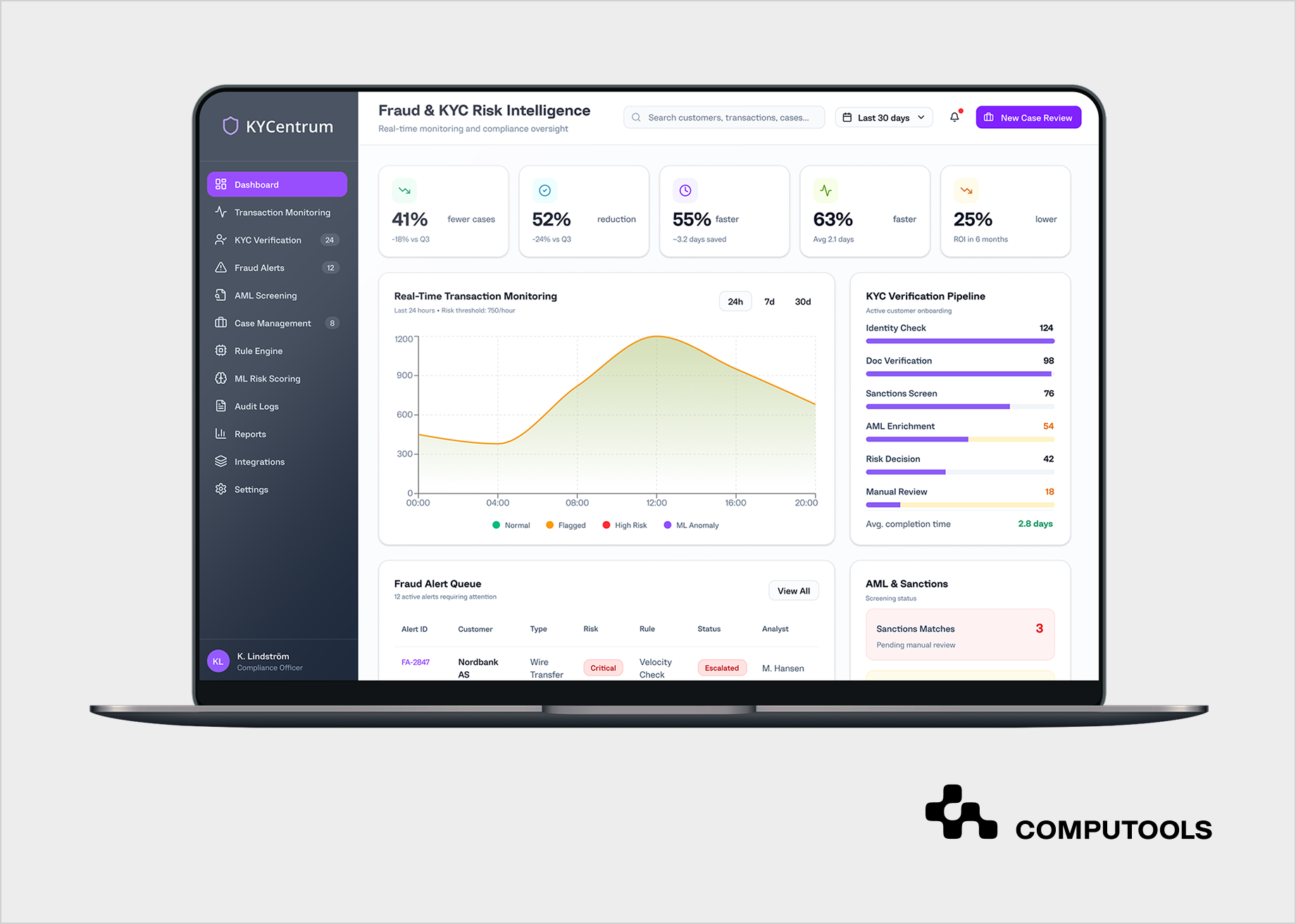

Computools helped a European finance provider replace fragmented KYC, AML, fraud monitoring, and case management processes with one controlled platform. The client needed to shorten customer onboarding, reduce manual reviews, improve fraud-detection accuracy, and give compliance teams clearer visibility into every verification decision. The project focused on measurable operational outcomes from the start, including onboarding speed, false-positive reduction, case resolution time, and compliance costs.

The delivered system connected document verification, liveness checks, sanctions screening, customer risk enrichment, transaction monitoring, configurable decision rules, and audit-ready case management. Computools applied its experience in banking software development services to integrate these workflows with the client’s existing financial infrastructure and ensure that customer data, verification results, alerts, and analyst actions remained traceable within a single operational flow.

The platform also used AI development expertise to support anomaly detection, adaptive fraud scoring, and explainable decisions. Analysts could see which rules, customer signals, verification results, and transaction patterns influenced each case, helping them review high-risk profiles faster and avoid unnecessary checks. Security controls, encrypted data exchange, secure key management, monitoring, and structured audit trails reflected the requirements typically covered by cybersecurity services for regulated financial systems.

The implementation reduced customer onboarding time by 50–60%, lowered false-positive alerts by 52%, accelerated compliance case resolution by 63%, and decreased operational compliance costs by 20–30%.

These results show how financial institutions can develop an automated KYC verification system grounded in clear KPIs, phased validation, secure integrations, and a practical roadmap to ROI, rather than treating automation as a standalone technical upgrade.

How to develop an automated KYC verification system for financial institutions in 9 steps

1. Define compliance requirements and measurable business targets

Start by defining the jurisdictions, customer segments, financial products, and onboarding channels the system must support. Verification requirements may differ for individual customers, legal entities, beneficial owners, non-residents, politically exposed persons, and applicants associated with higher-risk jurisdictions or products.

The compliance scope should cover initial customer identification, beneficial ownership checks, enhanced due diligence triggers, periodic reviews, ongoing monitoring, record retention, and escalation procedures. FATF Recommendation 10 requires financial institutions to identify and verify customers and beneficial owners, understand the purpose and nature of the business relationship, and conduct ongoing risk-based due diligence.

Convert the regulatory scope into functional rules and measurable KPIs. Relevant indicators include:

- onboarding time;

- straight-through processing;

- manual review volume;

- false-positive rate;

- verification completion rate;

- case resolution time;

- cost per completed verification.

This gives financial institution KYC compliance a clear delivery framework. Product, engineering, risk, and compliance teams can evaluate whether each release reduces manual work and processing time while preserving verification quality, decision traceability, and regulatory control.

For KYCentrum, the client prioritized shorter onboarding, fewer manual reviews, more accurate fraud detection, lower false-positive volumes, and faster compliance investigations. These targets shaped the platform architecture, workflow logic, and decision model before implementation began.

2. Map the current KYC process and design risk-based customer journeys

Document the complete current-state process before deciding what to automate. The process map should show how customer information is collected, which systems and providers perform each check, where analysts intervene, how additional evidence is requested, and where final decisions are stored.

Identify the steps that create the greatest operational friction:

- duplicated data entry;

- spreadsheet-based tracking;

- separate verification portals;

- repeated document checks;

- unclear ownership between teams;

- cases that return to the same queue;

- manual preparation of audit evidence.

These gaps increase onboarding time, create inconsistent decisions, and make it harder to reconstruct why a customer was approved, rejected, or escalated.

The target process should route customers according to risk level, product, jurisdiction, and evidence quality. A low-risk retail applicant with consistent identity data may pass through automated verification, while a corporate customer with a complex ownership structure may require beneficial ownership checks and enhanced due diligence. A sanctions match, a failed liveness check, a damaged document, or a conflicting customer attribute should trigger a defined exception route with a clear owner and the required next action.

EBA guidance requires financial institutions that use remote onboarding solutions to maintain risk-sensitive policies and to assess whether the selected technologies are reliable and appropriate for customer due diligence. The workflow should therefore reflect both regulatory obligations and the institution’s internal risk policy.

Effective KYC automation for financial institutions depends on redesigning the process before automating it. The target model should reduce unnecessary handoffs, separate standard cases from high-risk reviews, and provide analysts with the full context needed to resolve exceptions.

Before KYCentrum was implemented, KYC, AML, fraud monitoring, and compliance reporting relied on legacy rules, manual reviews, and disconnected tools. Computools consolidated these activities into a single operational workflow, enabling verification results and risk signals to flow directly into decisioning, analyst review, and case management.

3. Design the platform architecture and customer data model

Break the platform into modules that can be developed, tested, and updated independently.

A typical architecture may include:

- customer onboarding interfaces;

- identity and document verification services;

- biometric verification;

- sanctions and watchlist screening;

- customer risk assessment;

- a configurable decision engine;

- analyst case management;

- audit and reporting services;

- notification services;

- an API and integration layer;

- operational monitoring and analytics.

A modular digital KYC verification platform gives the financial institution greater control over vendors and future changes. Verification providers, screening databases, or biometric services can be replaced without rebuilding the complete onboarding process. New products and jurisdictions can also be added through configuration and new workflow rules rather than separate systems.

The customer data model should connect every profile with its documents, beneficial owners, verification attempts, biometric sessions, screening results, risk factors, analyst actions, and final decisions. Each record should preserve timestamps, provider responses, rule versions, model versions, confidence scores, overrides, and supporting evidence.

This structure is essential for auditability. A financial institution may need to explain a decision months or years later, after verification providers, internal rules, or risk models have changed. Storing only the final status, such as “approved” or “rejected,” does not provide enough evidence to reconstruct that decision.

KYCentrum used Java and Spring Boot for backend services and workflow logic, Apache Kafka for real-time event processing, and PostgreSQL for structured records of customers, cases, fraud, and decisions. External KYC and AML services were connected through an integration layer, while audit trails preserved the relationship between verification results and analyst actions.

Financial institutions that depend on legacy infrastructure may need to introduce the KYC layer incrementally rather than replace core systems. See our guide on modernizing legacy banking systems without service downtime for a phased approach to architecture, integration, data migration, and rollout.

4. Automate document capture and identity verification

The document workflow should begin with capture quality. Web and mobile interfaces need to detect blur, glare, cropped edges, missing pages, low resolution, and unsupported document types before files are submitted. Resolving these problems immediately reduces failed checks and avoids sending preventable exceptions to analysts.

The verification module should:

- identify the document type and issuing country;

- extract names, dates, addresses, and document numbers;

- validate machine-readable zones or barcodes;

- check expiration and issue dates;

- inspect available security features;

- detect signs of tampering or image manipulation;

- compare extracted data with the customer’s application;

- check whether the same document has appeared in another profile.

The National Institute of Standards and Technology (NIST) separates identity proofing into identity resolution, evidence validation, attribute validation, identity verification, and enrollment. Evidence validation confirms that the submitted document is genuine and accurate, while identity verification confirms that it belongs to the applicant.

The platform should assign confidence levels to each result. An application supported by a clear document and consistent customer data may proceed automatically, while a suspected alteration, an unreadable security feature, an inconsistent date of birth, low extraction confidence, or a possible duplicate should trigger a reason-coded exception.

Reliable identity document verification reduces data entry, accelerates straightforward applications, and focuses compliance resources on cases with meaningful uncertainty. It also creates structured customer attributes that can be reused for screening, risk assessment, and downstream banking systems.

In KYCentrum, automated document checks were connected with liveness verification, sanctions screening, customer risk data, and case management. Results were entered into the same customer record rather than remaining in an external provider’s portal, giving analysts a complete view of the verification process.

5. Add biometric verification and onboarding fraud controls

Biometric checks help confirm that the person completing the onboarding flow is the owner of the submitted identity document. A common process compares the document portrait with a live selfie or video and performs liveness detection to identify printed photos, screen replays, masks, manipulated images, or injected media.

The system should retain separate results for facial similarity, liveness confidence, image quality, and detected attack indicators. A single pass-or-fail response gives analysts too little information to assess a disputed or borderline case.

NIST’s current digital identity guidance addresses threats such as falsified identity images, forged videos, and morphed media used to defeat evidence validation and biometric comparison. It also recognizes different identity assurance levels and verification models, including remote unattended and remote attended processes.

The workflow should define:

- minimum facial match and liveness thresholds;

- retry limits;

- fallback verification methods;

- accessibility alternatives;

- customer consent requirements;

- manual review criteria;

- retention rules for biometric data.

Effective biometric identity verification should also be combined with device and session signals. Repeated applications from one device, inconsistent IP locations, emulator use, automated form completion, or multiple identities linked to the same contact details can reveal fraud that document and facial checks miss individually.

For the KYCentrum client, liveness results were assessed together with customer information, fraud indicators, transaction patterns, and configurable rules. This broader decision context helped reduce confirmed fraud cases by 41% while lowering false-positive alerts by 52%, according to the project results.

Identity checks become more effective when document and biometric results are evaluated together with behavioral, device, and transaction signals. Our guide to building a real-time fraud detection platform for banks explains how these signals can be connected through real-time scoring and analyst workflows.

6. Integrate AML screening and ongoing customer due diligence

The platform should connect customer identity data with the screening sources required by the institution’s markets and internal risk policy.

Depending on the operating model, this may include:

- sanctions lists;

- politically exposed persons;

- relatives and close associates;

- internal watchlists;

- adverse media sources;

- beneficial ownership databases;

- higher-risk jurisdiction lists.

Before matching, the system should standardize names, dates, countries, addresses, and identifiers. Matching logic needs to account for transliteration, aliases, alternative name order, spelling variations, incomplete records, and different date formats. Exact matching will miss relevant records, while loose matching can overwhelm analysts with weak alerts.

Every potential match should contain enough context for review: the source, matched fields, similarity level, customer details, list record, risk category, and reason for escalation. Analysts should be able to confirm or dismiss the match and preserve their reasoning in the audit history.

AML and KYC automation must also continue after onboarding. Customer information and risk exposure change over time. An expired document, a new beneficial owner, a sanctions update, an unusual transaction pattern, an address change, or movement into a higher-risk category may require re-screening or enhanced due diligence.

FATF guidance recognizes that digital identity can support both customer identification at account opening and ongoing due diligence. EU requirements similarly cover identity verification, transaction monitoring, and suspicious activity reporting across the customer relationship.

KYCentrum connected automated customer checks with sanctions screening, AML enrichment, and real-time transaction monitoring. A new transactional or screening risk signal could therefore be assessed against the customer’s verification history within the same case environment.

7. Build decision logic and analyst review workflows

Create a decision engine that combines document results, biometric outcomes, screening matches, customer attributes, product risk, geographic exposure, fraud indicators, and internal compliance rules.

The system should produce clear outcomes, such as:

- approve automatically;

- request additional evidence;

- send for manual review;

- initiate enhanced due diligence;

- restrict account capabilities;

- reject the application.

Rules should have owners, effective dates, version histories, test scenarios, and approval procedures. Compliance teams need a controlled way to change thresholds or routing logic without requiring a complete software release. Previous decisions must remain linked to the rule version active at that time.

An automated compliance verification workflow should route unresolved or high-risk cases into a structured analyst workspace. Customer data, documents, biometric results, screening matches, risk scores, previous attempts, and communication history should remain available within one case record.

Queue prioritization, case ownership, escalation paths, service-level timers, and four-eyes approval help analysts resolve ambiguous cases consistently and prevent high-risk applications from remaining in general review queues.

KYCentrum combined transparent rule-based logic with ML-supported fraud scoring and centralized case management. Analysts received the relevant evidence and risk context in a single workflow, helping the client resolve compliance cases 63% faster.

8. Integrate the system with banking infrastructure and security controls

The KYC platform must exchange data with the systems that manage the wider customer relationship. These may include core banking, CRM, lending, cards, payments, document storage, electronic signatures, customer communication, support, analytics, and regulatory reporting.

Define which system owns each customer attribute and how updates propagate. The KYC layer should return structured outputs, including:

- verification status;

- customer risk level;

- decision reasons;

- approved products or limits;

- account restrictions;

- review dates;

- identifiers for supporting evidence.

A digital customer onboarding platform also needs resilient integration behavior. Each connection should include authentication, schema validation, idempotency, timeout handling, retry logic, reconciliation, and manual recovery procedures. A verification-provider outage should pause or reroute an application without losing customer data or creating duplicate profiles.

Sensitive identity and financial information should be protected through encryption in transit and at rest, role-based access, privileged access controls, secure key management, retention policies, and detailed activity logs. Monitoring should identify failed integrations, unusual access, delayed events, security incidents, and growing processing queues.

Computools developed the API orchestration required to connect KYCentrum with the client’s banking infrastructure and external verification and AML providers. TLS 1.3 protected data transmission, hardware-backed key management supported sensitive data protection, and Azure Monitor and Microsoft Sentinel provided operational and security visibility.

KYC workflows also need to operate reliably within the broader financial product architecture. Our guide to building a fintech mobile app with secure banking integrations covers compliance controls, identity provider integrations, banking APIs, and backend orchestration.

9. Validate the system through a pilot and measure ROI

Launch the first release for a controlled customer segment, product, jurisdiction, or onboarding channel. A limited pilot provides enough application and verification volume to evaluate the platform without exposing the entire customer base to untested rules, integrations, or risk thresholds.

Before launch, test successful and unsuccessful scenarios, including:

- forged or expired documents;

- inconsistent customer attributes;

- false-positive sanctions matches;

- failed biometric checks;

- duplicated submissions;

- unavailable external providers;

- delayed events;

- analyst overrides;

- incomplete audit records;

- access-control violations;

- recovery after infrastructure failures.

Compliance officers should validate rule behavior and case evidence. Security teams should review data access and protection. Operations teams should confirm that common exceptions can be resolved without engineering support.

Compare pilot performance against the baseline defined in the first step. Focus on onboarding speed, straight-through processing, manual review volume, alert quality, operating costs, and fraud outcomes.

Use the results to adjust thresholds, customer instructions, workflows, provider routing, and review queues before expanding the automated KYC verification system. Each rollout phase should have clear checkpoints and acceptance criteria tied to operational and financial value.

KYCentrum was delivered iteratively, allowing compliance specialists to validate verification modules, decision rules, streaming components, and investigation workflows before the complete rollout. The implemented platform reduced onboarding time by 50–60%, lowered operational compliance costs by 20–30%, and reached ROI within six months, according to the case results.

How explainable KYC decisioning reduces compliance risk

Explainable decisioning reduces compliance risk by making every automated KYC outcome traceable, reviewable, and consistent with internal policy. Financial institutions need to understand which verification signals, rules, and risk factors led to an approval, rejection, or escalation, especially when AI and automated scoring are involved.

FATF recommends assessing digital identity systems through a risk-based approach to customer due diligence.

The EBA similarly requires financial institutions to implement risk-sensitive remote onboarding policies and evaluate whether the technologies they use are reliable and appropriate for their AML/CFT obligations.

1. Combine verification signals in one decision flow

The decision engine should process structured results from across the onboarding journey:

- document authenticity and extracted identity data;

- biometric match and liveness results;

- sanctions, PEP, and watchlist screening;

- customer, product, and jurisdiction risk;

- device and session indicators;

- duplicate identity signals;

- previous applications and transaction history.

For automated customer identity verification, detailed result codes are more useful than a general pass-or-fail response. They allow the system to distinguish among low image quality, inconsistent customer data, suspected document tampering, and possible duplicate identities and assign the correct next action.

2. Separate rules, risk scoring, and AI

A controlled decision model should combine several layers:

| Decision layer | Role |

| Deterministic rules | Apply mandatory regulatory and internal controls |

| Risk scoring | Combine customer, product, and verification signals |

| Machine learning | Detect anomalies and hidden relationships |

| Human review | Resolve complex or high-risk cases |

Rules should cover clear requirements such as expired documents, prohibited jurisdictions, confirmed sanctions matches, or missing beneficial ownership data. Risk scoring helps evaluate combinations of weaker signals that collectively become significant.

An AI-powered KYC solution can support anomaly detection, duplicate profile identification, and case prioritization. Each output should include the model version, confidence level, and factors that influenced the score so analysts can evaluate the recommendation.

3. Connect KYC and fraud signals

A customer may pass document and biometric checks while still presenting an elevated risk. Multiple applications from one device, reused contact details, inconsistent geolocation, or links to confirmed fraud can indicate synthetic identity activity or account-opening abuse.

Connecting identity checks with fraud prevention in banking gives compliance and fraud teams one customer risk profile. This improves early detection and prevents separate systems from producing conflicting assessments.

4. Explain each decision outcome

The platform should record why it selected automatic approval, additional evidence, manual review, enhanced due diligence, account restrictions, or rejection. Each outcome should include the triggered rules, relevant risk scores, provider responses, and supporting evidence. This allows analysts and auditors to understand the basis of the decision without reconstructing it across separate systems.

5. Control analyst overrides

Manual overrides should require a reason code, written justification, and, for high-risk cases, four-eyes approval. The platform should retain both the original automated recommendation and the final analyst decision. Comparing these records helps compliance teams identify recurring overrides, weak rules, and poorly calibrated risk thresholds.

6. Preserve an audit-ready decision record

Every decision should include:

- input data and evidence;

- provider and screening responses;

- active rule and model versions;

- risk and confidence scores;

- analyst actions and overrides;

- timestamps;

- final outcome and rationale.

This record allows compliance teams to reproduce historical decisions and show that comparable customers were assessed consistently. Operational metrics such as manual review rates, override frequency, processing time, and false positives also reveal where decision logic requires improvement.

In the KYCentrum project, Computools integrated document verification, liveness checks, sanctions screening, customer data, transaction signals, configurable rules, and ML-supported fraud scoring into a single decision environment.

The explainability module showed analysts why a customer profile or transaction had been flagged and provided the evidence required for review. This contributed to a 52% reduction in false-positive alerts and helped compliance teams resolve cases 63% faster.

Launch your automated KYC platform within 1–3 months instead of years, and accelerate customer onboarding while maintaining enterprise-grade compliance and trust.

How to measure the impact of KYC automation

Once decision logic, exception handling, and audit controls are in place, the institution needs to measure whether automation improves operational, compliance, and financial performance. Before launch, define baseline performance for the current process and compare it with the results after implementation.

Track the following metrics:

- Average onboarding time: Measures how long it takes to move from application submission to a final decision. Effective KYC onboarding automation should shorten this cycle without increasing verification errors.

- Straight-through processing rate: Shows the percentage of customers approved without analyst involvement. A higher rate indicates that standard, low-risk cases are being handled efficiently.

- Manual review rate: Tracks how many applications still require human intervention. This helps identify poorly calibrated rules, weak provider responses, or workflows that continue to create unnecessary analyst work.

- False-positive rate: Measures how often sanctions, PEP, fraud, or identity alerts are dismissed after review. Lower false positives reduce compliance workload and allow teams to focus on genuinely high-risk cases.

- Verification completion rate: Shows how many customers successfully finish document, biometric, and data checks. Low completion may indicate unclear instructions, technical failures, or excessive verification steps.

- Customer abandonment rate: Measures the percentage of applicants who leave before onboarding is complete. This is a critical indicator for evaluating whether stronger controls are creating avoidable friction.

- Cost per verification: Includes external provider fees, infrastructure costs, manual review time, and operational support. In custom KYC software development, this metric helps assess whether automation is reducing the total cost of customer verification.

- Average case resolution time: Tracks how quickly analysts close escalated, ambiguous, or high-risk cases. Faster resolution improves customer experience and reduces compliance backlogs.

- Compliance exception rate: Measures incomplete records, unsupported decisions, missing evidence, or broken audit trails. This KPI shows whether the platform supports consistent AML compliance across automated and manual workflows.

- Fraud and risk outcomes: Tracks confirmed fraud, duplicate identities, suspicious accounts, and post-onboarding incidents. These results reveal whether faster processing is being achieved without weakening controls.

- ROI: Compares implementation and operating costs with savings from reduced manual work, fewer false positives, faster onboarding, lower fraud losses, and improved analyst productivity.

These metrics should be reviewed by customer segment, product, jurisdiction, and risk level. This makes it easier to identify where the system performs well, where rules require adjustment, and where further identity verification system development can deliver additional operational value.

Why choose Computools for KYC automation development?

Computools approaches custom KYC software development through measurable operational outcomes: faster onboarding, fewer false positives, lower analyst workload, and stronger control over customer risk. In KYCentrum, the delivered platform reduced onboarding time by 50–60% and lowered false-positive alerts by 52%, showing that automation improved both processing speed and decision quality.

Through financial software development services, Computools can connect identity verification, AML screening, fraud monitoring, decision logic, case management, and audit reporting within one controlled system. In the KYCentrum project, this unified workflow helped compliance teams resolve cases 63% faster and reduced operational compliance costs by 20–30%.

Computools delivers fintech KYC solutions for neobanks, payment platforms, lending products, digital wallets, and embedded finance services that need to scale verification without expanding manual review at the same rate. In KYCentrum, automated document checks, liveness verification, sanctions screening, and ML-supported risk scoring contributed to a 41% reduction in confirmed fraud cases.

For growing financial products, fintech software development should connect onboarding decisions with fraud and transaction risk from the beginning. Computools builds configurable rules, API integrations, event-processing pipelines, and explainable scoring models that allow compliance teams to adapt workflows as customer volumes and risk patterns change. In KYCentrum, this approach reduced false-positive alerts by 52% and confirmed fraud cases by 41%.

Through web development services, Computools can create onboarding interfaces, analyst dashboards, case review workspaces, admin panels, and reporting views that consolidate verification evidence and decision history into a single environment. In KYCentrum, centralized case management and clearer access to risk signals helped analysts complete compliance investigations 63% faster.

Computools reduces delivery risk through phased implementation, early validation of data flows and decision rules, clear checkpoints, and KPI-based rollout. The KYCentrum platform achieved ROI within six months, demonstrating how technical delivery can be directly tied to onboarding efficiency, compliance productivity, fraud reduction, and operating costs.

Contact Computools at info@computools.com to discuss a KYC platform designed around measurable compliance, onboarding, and risk-management outcomes.

Financial institutions comparing delivery partners can also review our overview of the top KYC software development firms for fintech platforms, including the technical, compliance, integration, and delivery criteria used in the evaluation.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.