THE AUTHOR:

Banks and FinTech companies are finding it necessary to integrate AI agents for financial workflow automation as manual processes can no longer keep pace with the speed, volume, and complexity of modern financial services. Customer onboarding, KYC checks, loan intakes, payment exceptions, reconciliation, fraud alerts, support requests, and compliance require quick and complex inter-system decisions. If these workflows depend on employees to move between CRM’s, core banking systems, document storage, spreadsheets, email compliance systems, and portals, the business ultimately loses time, control, and visibility.

Agentic AI has the capacity to change the workflow model. A generative AI assistant can respond to requests. An AI agent can do much more. It can move work forward by asking for and retrieving the missing information, customer data and policy and even classify documents, compare records, initiate approved actions, and escalate anything outside of approvals. Unlike traditional systems that produce one output, agentic systems integrate many specialized agents to operate within defined business goals to plan, make decisions, carry out tasks, and enhance processes.

Types of AI agents used in finance and banking

| AI Agent Type | Primary Function | Where It Is Used | Business Value |

| KYC / Onboarding Agent | Validates identity documents, checks missing data, prepares onboarding cases | Banking onboarding, FinTech account creation | Reduces onboarding time, lowers manual verification load |

| Loan Processing Agent | Reviews applications, extracts key data, prepares underwriting summaries | Lending workflows, credit platforms | Speeds up approval cycles, reduces bottlenecks |

| Fraud Triage Agent | Detects anomalies, prioritizes alerts, summarizes risk signals | Fraud monitoring systems, transaction analysis | Improves fraud detection speed and accuracy |

| Compliance / AML Agent | Maps transactions to rules, prepares compliance cases, supports AML reviews | AML monitoring, regulatory reporting | Reduces compliance workload and escalation time |

| Payment Exception Agent | Investigates failed or delayed payments, checks status, suggests actions | Payment gateways, banking operations | Reduces payment resolution time and support load |

| Customer Support Agent | Retrieves account context, drafts responses, routes complex cases | Banking support, FinTech apps | Improves response speed and consistency |

| Reconciliation Agent | Matches transactions across systems, identifies mismatches | Accounting, treasury operations | Reduces reconciliation errors and manual checks |

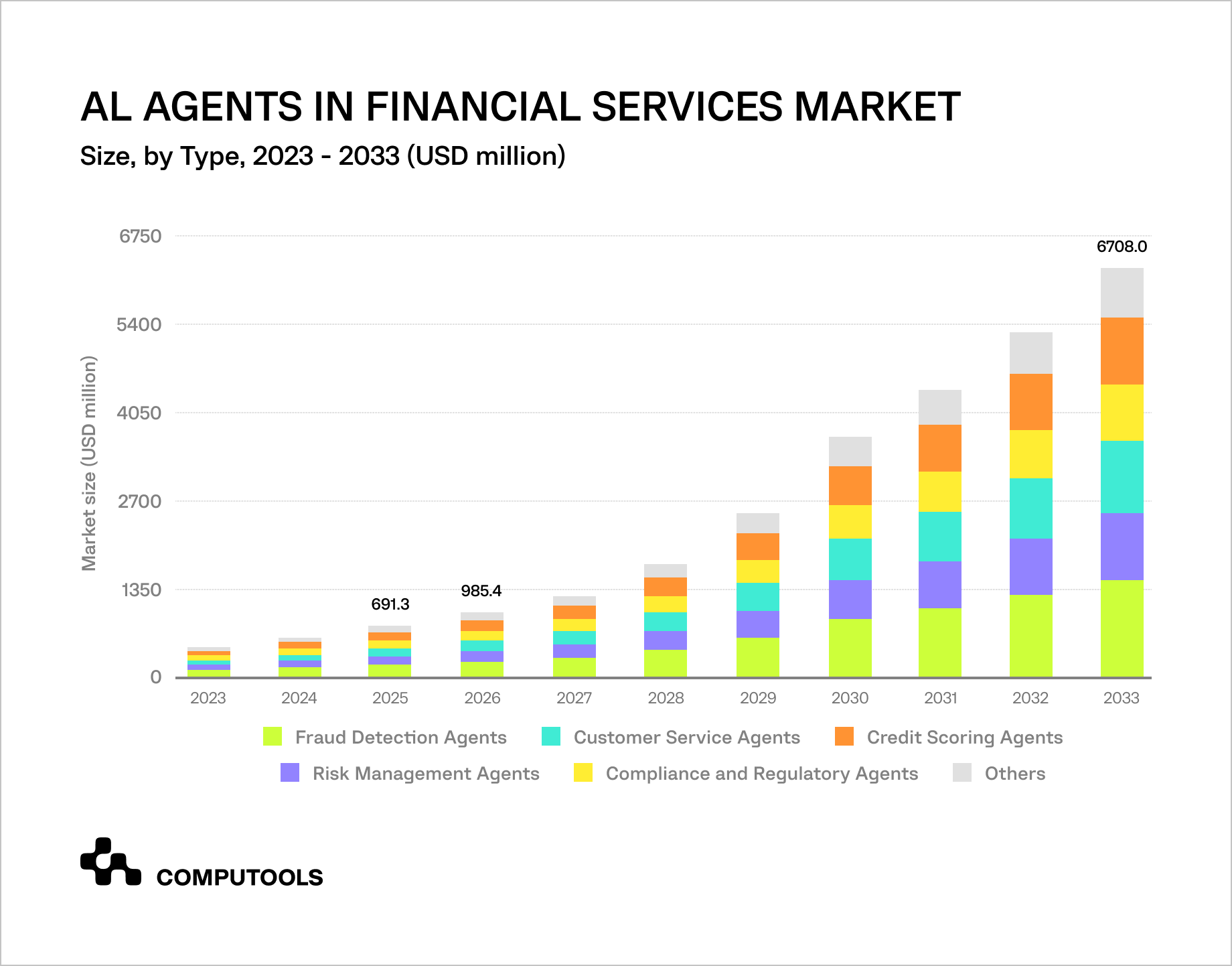

Grand View Research estimates the AI agents in the financial services market will grow from USD 985.4 million in 2026 to USD 6.7 billion by 2033, increasing at a CAGR of 31.5%. It is clear the market is reacting to real operational pressure, evidenced by the speed of AI agent adoption in workflows where the visibility and quality of decisions and risks impact a firm’s financials.

The AI agents’ segment for fraud detection is indicative of this market speed, capturing 33.8% of segment share in 2025, and shows that financial services firms are quickly adopting AI agents to monitor, detect, and assess suspicious activities, anomalies, risk, and prioritize alerts.

The scope for AI agents is expanding further into customer service, compliance, accounting, reporting, lending, credit underwriting, and all other core banking operations. The more an AI agent is embedded in enterprise systems (core banking, ERP, CRM, payment systems, and compliance frameworks) the more valuable the agent becomes, since it enables the agent to pull real-time information, automate reporting, dynamically route cases, generate documents, and facilitate decision support across all front, middle, and back-office operations.

Traditional banks accounted for the largest institutional share at 45.5% in 2025, while FinTech companies are expected to grow significantly as they apply agents to fraud detection, risk management, customer support, and real-time operational insight. These numbers show that AI agents are becoming practical workflow operators in financial services, especially where manual review, fragmented data, and slow handoffs limit scale.

This article explains how to build AI agents for workflow automation in fintech and banking, how to define their roles and boundaries, how to connect them with financial data and systems, and how to keep them secure, auditable, and commercially useful.

Financial institutions that are still structuring the workflow layer can also review Computools’ guide on how to develop a banking workflow automation system before defining which AI agents should handle intake, validation, routing, approvals, and exception management.

Computools case study: Avelion’s AI Agents for financial workflow automation

The Avelion AI Agents case illustrates how financial firms can implement AI agents to ease operational demands while maintaining control over customer dialogue, compliance, and service levels. The client was a multiregional firm located in the United Kingdom that offered regulated financial products and advisory services. The company’s sales and support teams carried out between 8,000 and 10,000 customer interactions on a monthly basis through telephone and non-telephone channels, including chat, email, instant messaging, and social media.

This overwhelmed the sales and support teams and increased the risk of providing inconsistent information to customers.

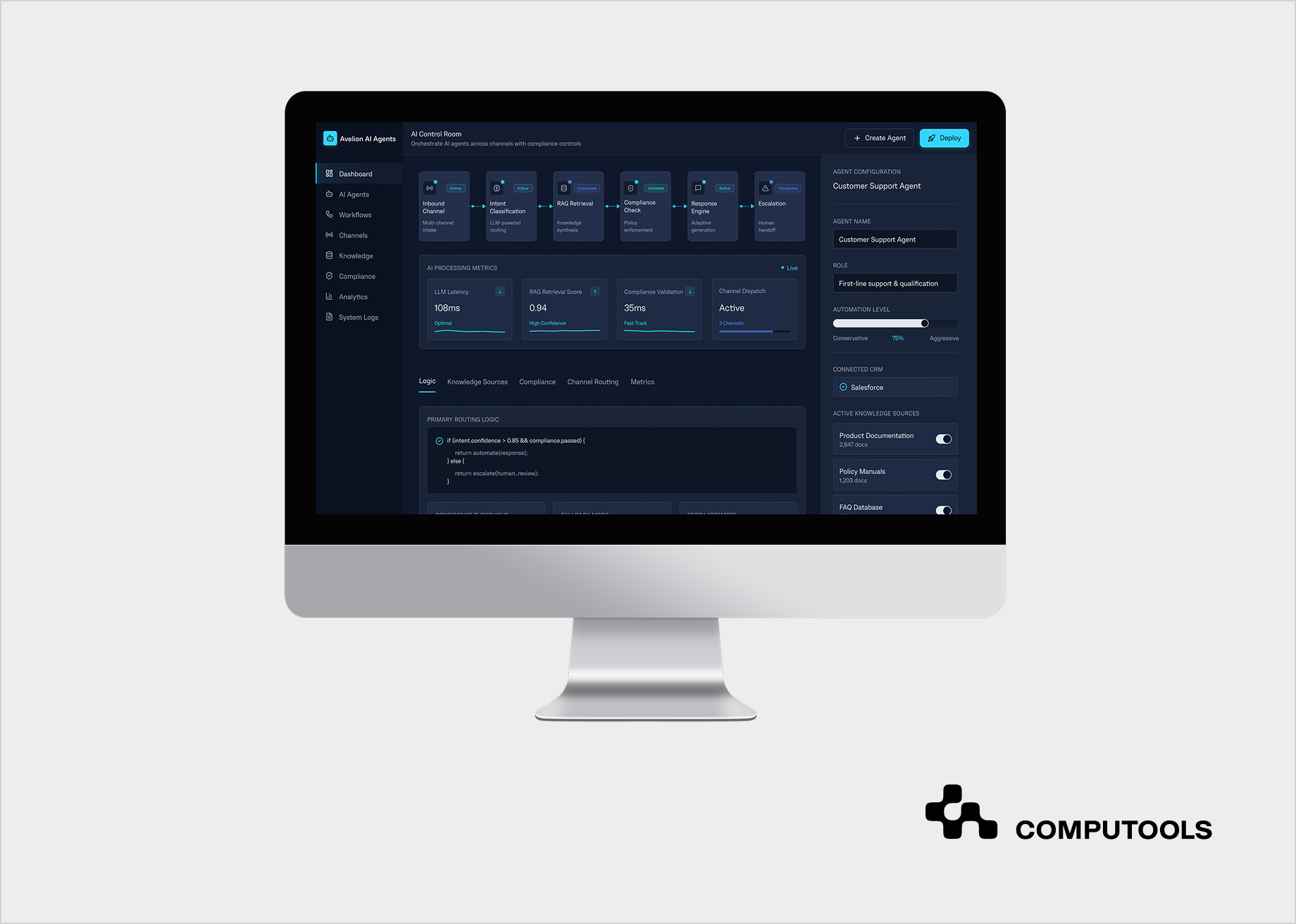

Computools designed a multi-channel AI agent framework that automated the majority of routine sales and support processes, while leaving the control of sensitive and/or complex cases to the human teams. The agents were developed to carry out automated communications through chat, email, instant messaging, social media, and voice. They were built using LLMs enhanced with RAG, function calling, and multimodal processing, which helped them retrieve the context, understand customer intent, formulate appropriate responses, and identify the need for case referral to a human for review.

The solution integrated with the client’s CRM, internal databases, product catalogs, knowledge bases, and compliance systems. This was critical because financial process automation depends on trusted data. An AI agent cannot support regulated communication properly if it works from disconnected scripts or outdated documents. It needs access to approved information sources, clear process logic, and defined limits on what it can say or do.

Computools also created a no-code orchestration layer to empower teams outside of software engineering to alter workflows, rules, and the behavior of agents in the system. This layer removed the dependency on engineering changes. The operator console granted employees the ability to view agent conversations, audit trails, performance, and workflow logic.

The results were operationally significant. Customer satisfaction increased by around 25%.

The AI agents:

- automated more than 50% of routine sales and support interactions;

- made response times up to 90% faster;

- supported 2x scalability during peak periods;

- reduced operational workload by 40–60.

How to build AI agents for financial workflow automation

Building AI agents for finance and banking workflow automation starts with a practical business question: which financial tasks should agents perform, and under what level of control?

When working with AI or planning to introduce AI into your product offerings, banks and FinTech companies should avoid beginning with a high-level, vague objective, such as “add AI to operations.” AI agents prove useful when performing specific tasks, such as verifying missing data, retrieving policies, drafting case summaries, prioritizing alerts, composing messages, creating tasks, and routing exceptions within a defined business process.

1. Define the Financial Workflow the Agent Will Support

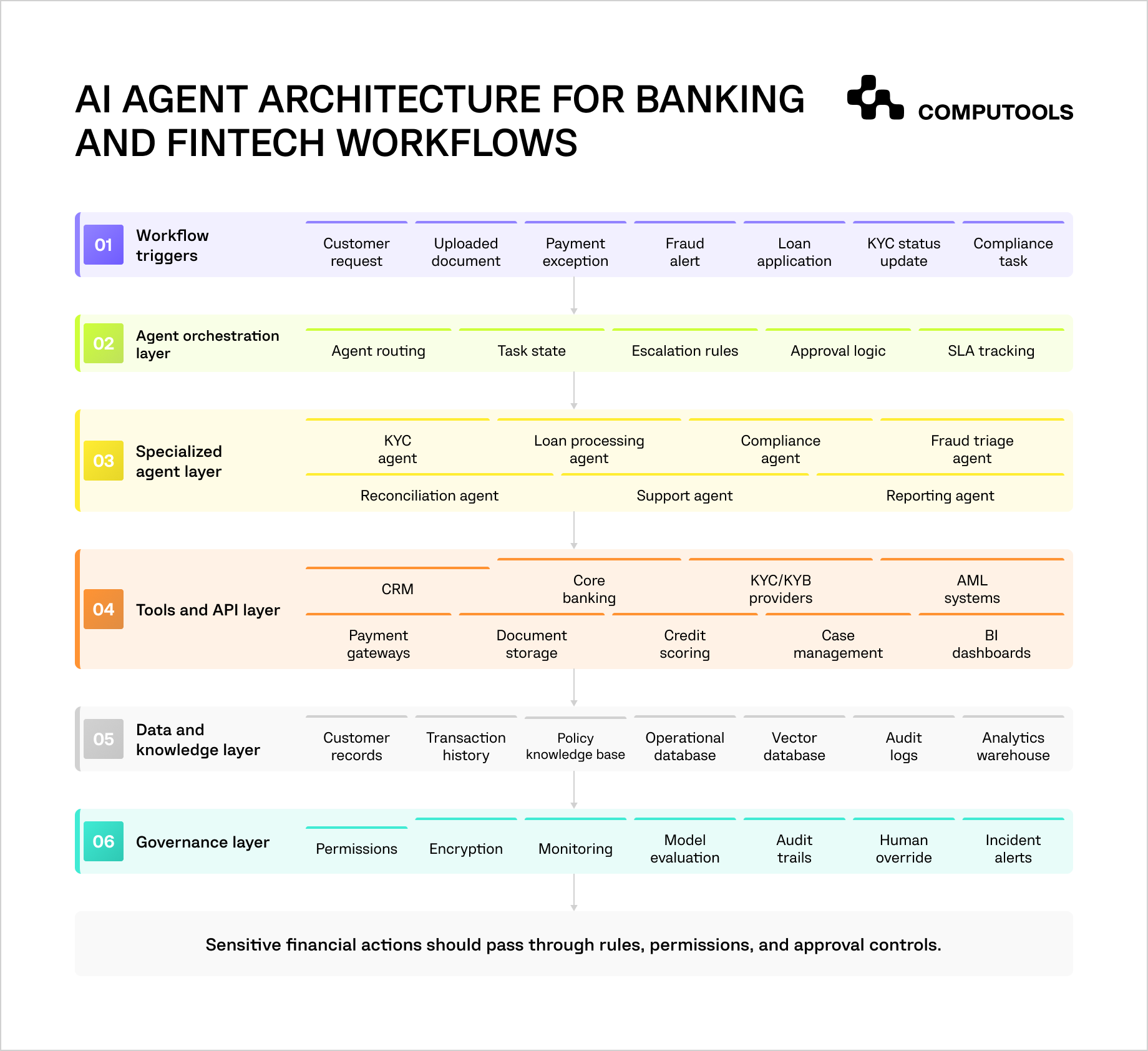

The first step is selecting the workflows where the use of AI agents will decrease manual work and simultaneously increase the speed of decisions being made. Processes that fit this description best generally involve heightened repetition, manual steps, and established escalation protocols along with observable lag times. For example, KYC verification, customer and loan onboarding, payment exceptions, reconciliation, fraud, chargeback work, compliance case prep, and triaging customer support cases.

The business should map the workflow before defining the agent. This includes the workflow trigger, required inputs, source systems, decision points, responsible teams, approval steps, exception paths, and final output.

For instance, a workflow for failed payments should capture significantly more than communicating to an agent that the payment has failed. The trigger should generate a structured event containing the following fields: payment ID, customer ID, failure reason, payment method, number of retry attempts, transaction amount, and failed attempts history, case status, and next steps. With this information, a payment exception agent can assess the problem, pull up the customer record, verify the payment retry rules, write the customer notification, or create a task in finance operations.

The same logic applies to loan processing automation. A loan intake agent should receive structured data such as applicant ID, application type, uploaded documents, missing fields, credit policy version, current status, and assigned underwriter. Without this context, the agent may produce a useful-looking summary but fail to move the actual workflow forward.

If this step is ignored, companies often build agents that answer questions but do not reduce operational workload. The agent may handle surface-level communication while employees still switch between CRM records, spreadsheets, document folders, compliance portals, and banking systems to complete the real work.

2. Define Agent Roles, Permissions, and Autonomy Levels

AI agents in banking and FinTech should be task-specific. One general-purpose agent for all financial operations creates too much risk because every workflow has different data needs, business rules, and compliance exposure.

A financial company may need several specialized agents:

- KYC intake agent;

- document analysis agent;

- compliance workflow agent;

- loan processing agent;

- fraud triage agent;

- reconciliation agent;

- customer support agent;

- reporting agent.

Each agent should have a written responsibility profile. This profile should define what the agent can access, what it can recommend, what it can change, which tools it can use, and when it must escalate the case to a human employee.

For example, a KYC agent may be allowed to read customer profiles, uploaded identity documents, KYC policy documents, and verification provider results. It may be allowed to create a case note or request missing documents. It should not approve a high-risk customer unless a separate compliance workflow allows that action.

A practical way to manage risk is to define autonomy levels:

Level 1: The agent retrieves information and drafts a summary.

Level 2: The agent recommends the next action.

Level 3: The agent creates a task or updates a case status.

Level 4: The agent triggers a low-risk approved workflow action.

Level 5: The agent completes a narrow process without staff review.

Most AI-powered financial workflows should start at Levels 1–3. For example, a fraud triage agent can prioritize suspicious alerts and prepare investigation notes, but account restrictions should follow approved risk rules and staff review. A loan processing agent can summarize an application and flag missing documents, but final credit decisions need controlled logic and accountability.

This structure prevents agents from acting outside their operational role. It also makes testing, monitoring, compliance review, and post-launch optimization easier.

3. Build the Agent Knowledge Layer Around Trusted Financial Data

AI agents depend on the quality of the data they can access. In financial workflow automation, the knowledge layer should include current policies, customer records, transaction histories, product terms, KYC rules, AML procedures, workflow histories, previous case outcomes, and support guidelines.

The technical architecture should separate operational records from knowledge retrieval. Structured databases should store customer records, workflow statuses, transaction data, approvals, risk scores, timestamps, and audit logs. Document storage should keep uploaded files, contracts, compliance documents, and customer evidence. A vector database can support retrieval across internal policies, support scripts, product rules, and historical cases.

The vector database should not become the source of truth for regulated financial records. It should support retrieval, while core systems and structured databases remain authoritative for balances, application status, approvals, customer identity, transaction history, and audit evidence.

For RAG-based agents, retrieval needs strict controls. The agent should retrieve only from approved document collections. Each document should have metadata such as document type, version, region, product line, effective date, owner, and compliance status. This matters because a lending policy for one country, product, or customer segment may not apply to another.

A KYC workflow automation agent, for example, should retrieve the latest policy version for the customer’s region, compare it with uploaded documents, check the verification provider response, detect missing fields, and prepare a structured review note for compliance staff.

In the Avelion AI Agents project, Computools connected agents with CRM, internal databases, product catalogs, knowledge bases, and compliance systems. The same data discipline is critical for AI agents in banking because the quality of agent output depends on the quality of connected sources.

4. Design Agent Reasoning and Action Logic Separately

A common mistake is giving an AI agent too much freedom too early. Financial workflow management needs a clear separation between what an agent can reason about and what it can do in connected systems.

Reasoning logic covers what the agent understands, prepares, and recommends. This may include intent recognition, document classification, information extraction, policy matching, missing field detection, case summarization, risk indicator identification, and next-step recommendations.

Action logic details what actions the agent can perform. Actions can be: case creation, workflow status updates, task assignments, document requests, customer responses, internal notifications, etc.

Agents are expected to provide outputs in a structured format. For example, a compliance agent reviewing a KYC case should return:

- case summary;

- missing documents;

- risk indicators;

- policy rules matched;

- confidence score;

- recommended next action;

- escalation reason;

- source references.

There are several benefits to structured outputs. The outputs can easily be validated. They can be displayed in operator consoles and can be stored in audit logs. They can be utilized in subsequent workflows. As a bonus, staff reviewing the work of agents will face less uncertainty.

Determining if an action can be taken is the responsibility of the workflow engine, combined with the agent. The agent can suggest the escalation of a case, but the workflow rules will determine if the case must be escalated. The agent can create a message for a customer, but the notification service will ensure the message follows the approved template and the message is approved before the message is sent.

This division provides additional safeguards for the finance and banking process automation. It prevents unapproved financial actions, ensures consistent business communication, and legal compliance.

5. Connect Agents With Financial Systems Through Controlled Tools and APIs

AI agents generate value when they integrate with existing software. In the case of banking and FinTech, AI agents can integrate with systems like CRM, core banking platforms, KYC/KYB, AML, payment services, credit scoring, document management, accounting, support tools, case management, and BI dashboards.

Agents should not be given the ability to issue open-ended commands to these systems. Instead, they should be able to utilize functions with prescribed constraints on inputs and outputs, such as:

`get_customer_profile(customer_id)`

`check_kyc_status(customer_id)`

`retrieve_payment_status(payment_id)`

`create_compliance_case(customer_id, reason, evidence)`

`update_case_status(case_id, status)`

`draft_customer_notification(case_id, template_type)`

`assign_task(case_id, team_id, priority)`

These functions should validate inputs, check permissions, log the request, and return structured data. They should also prevent actions that are out of the agent’s reach.

High-volume scenarios typically require event-driven logic. For example, failed payments, uploaded documents, fraud alerts, chargeback requests, and loan application updates trigger automatic task routing to specific agents. A workflow engine or orchestration service can handle the event, route the task, and apply state management and escalation logic.

Message queues that include Kafka, RabbitMQ, or AWS SQS support the range of communication events and protect downstream systems from overload. This gives operational control to teams on tasks that may be executed later and helps handle exceptions such as delays and document upload spikes, payment exceptions, fraud alerts, and support requests.

Managing each integration requires retry logic, timeout handling, idempotency, and rate limiting with error tracking. Failure to do this will lead to inconsistent communication with customers, missed status updates, broken audit trails, and duplicate cases.

6. Build Security, Compliance, and Auditability Into Every Agent

Cybersecurity design should prioritize financial risk. Insufficient control of an agent can lead to data breaches, improper system actions, increased opportunities for fraud, and a worsening of the explainability problem for regulatory compliance.

Usage of session-lifetime logging, source tracking, approval records, and the ability for a human to override the system should be considered mandatory, in addition to:

- role-based access control;

- least-privilege access;

- encryption (in-transit and at-rest);

- secure API authentication;

- masking of sensitive data.

The system should prevent agents from retrieving data unrelated to the active case. For example, a support agent handling a payment status question should not access full credit history, unrelated KYC documents, or internal risk notes.

Auditability should be designed from the start. Every agent action should generate a log entry with:

- agent name;

- case ID;

- workflow trigger;

- data sources accessed;

- tool calls made;

- prompt version;

- model version;

- retrieved source references;

- output;

- confidence score;

- escalation reason;

- final human decision, where relevant.

The importance is heightened in the case of compliance workflow automation. The organization should be able to identify the source documents, the compliance policy rule, the risk assessment indicators, the agent’s recommendation, the reviewer of the recommendation, and the reviewer’s final decision.

In the Avelion project, Computools used controlled workflows, operator visibility, dual-model validation, and compliance-connected systems. The same principle matters in AI automation in banking, where agent behavior must be explainable, limited, and reviewable.

In AML workflows, AI agents can support alert prioritization, evidence collection, suspicious pattern summaries, and analyst handoffs.

For the transaction monitoring layer behind these workflows, read Computools’ guide on how to build an AML transaction monitoring system.

7. Test Agents With Real Financial Scenarios Before Expanding Automation

AI agents should be tested against real operating conditions before they receive wider responsibility. Real cases include missing documents, conflicting customer records, unclear messages, outdated files, duplicate requests, failed integrations, slow provider responses, prompt injection attempts, and edge-case compliance issues.

Testing should cover:

- historical case replay;

- incomplete document checks;

- outdated policy retrieval;

- conflicting data scenarios;

- failed API calls;

- duplicate event handling;

- security testing;

- prompt behavior testing;

- performance testing;

- human review comparison;

- low-confidence outputs.

For example, a KYC agent should be tested against expired IDs, unreadable files, mismatched names, unsupported document types, customers from different regulatory regions, and cases with partial verification provider responses.

Monitoring should track both system health and business performance. Technical metrics should include latency, failed tool calls, queue length, timeout rate, retrieval accuracy, model error rate, and integration failures. Business metrics should include automation rate, escalation rate, manual review time, average case handling time, false positives, false negatives, customer response time, and compliance review backlog.

Customer-facing FinTech products need secure banking integrations before advanced automation can deliver value. Account access, payment status, user authentication, transaction history, and mobile performance all affect operational reliability.

Computools explains these requirements in its guide on how to build a FinTech mobile app with banking integrations.

Launch your banking AI agents within 1–3 months instead of years, and automate complex financial workflows with enterprise-grade accuracy and control.

Why choose Computools for building AI agents for financial workflow automation

Computools is a strong fit for financial services automation when AI agents need to work with real financial data, regulated communication, internal systems, and measurable operational targets.

The company’s financial software development services include the same building blocks AI agents need: KYC logic, fraud signals, AML enrichment, case management, audit trails, API integrations, operator interfaces, and structured financial data.

Computools supports these with 250+ engineers, 400+ delivered projects, ISO 9001 and ISO 27001 certifications, GDPR and HIPAA compliance, and Microsoft and AWS Partner status. This gives financial clients the delivery capacity and security discipline needed for sensitive workflows.

In KYCentrum, Computools developed fraud prevention and compliance functionality covering transaction monitoring, automated KYC verification, fraud scoring, sanctions screening, AML enrichment, case management, and compliance reporting. This supports agent use cases such as customer file review, fraud alert prioritization, compliance case preparation, and exception routing.

CardFalcon is an example of our banking software development services. The platform centralized credit card issuing operations for a Swiss banking institution, connecting partner banks, internal teams, contracts, offers, approvals, and operational requests. This is relevant for AI agents in banking because they need role-based workflows, approval paths, status control, document accuracy, and staff visibility.

Our experience of intelligent workflow automation for finance translates into practical agent use cases: KYC intake agents, support agents, loan processing agents, compliance workflow agents, payment exception agents, and fraud triage agents.

For fintech software development, Computools also brings strong integration experience in cash flow management and financial operations platforms. This matters because financial AI agents need controlled access to account data, payment events, customer records, transaction statuses, and external financial services. Without secure integrations, agents can summarize information, but they cannot move real workflows forward.

Computools also covers the technical layers around agent adoption. Our web development services support operator consoles, review screens, dashboards, and admin tools where teams can monitor agent actions and approve sensitive steps. Our AI development expertise includes RAG, function calling, model validation, and agent behavior design. Our data engineering work enables clean records, retrieval pipelines, audit logs, analytics, and model-ready financial data.

The result is a practical delivery model for automated financial operations: AI agents that perform specific financial tasks, work with trusted systems, produce reviewable outputs, and stay visible to the teams responsible for compliance, operations, customer experience, and revenue control.

Final thoughts

AI agents for financial workflow automation should be designed as controlled operational components inside banking and FinTech workflows. Their value depends on how well they handle real tasks, such as checking KYC files, preparing loan application summaries, prioritizing fraud alerts, routing compliance cases, resolving payment exceptions, supporting reconciliation, and reducing repetitive customer communication.

The agents need access to verified data, defined permissions, structured outputs, API-based actions, escalation rules, audit logs, and monitoring. This is especially important in banking and fintech workflow automation, where speed only creates value when accuracy, compliance, and accountability remain intact.

A well-built agent does not replace the process/service owner. It reduces the manual load on them. It collects background information, verifies data, drafts recommendations, identifies anomalies, creates assignments, prepares templated messages, and shows teams what needs the most focus. This improves processing speed while keeping sensitive decisions under business control.

Banks and FinTech companies that invest in AI agents should treat them as part of the operating model. The right architecture can achieve optimal speed and visibility in onboarding, lending, payment, compliance, and fraud operations, as well as customer support.

Computools builds AI agents that automate particular tasks within finance, integrate with trusted systems, and maintain a clear audit trail. If you are looking for secure, well-integrated, and ready-to-use banking and FinTech AI operations, reach out to see how we can help get your agents up and running quickly.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.