THE AUTHOR:

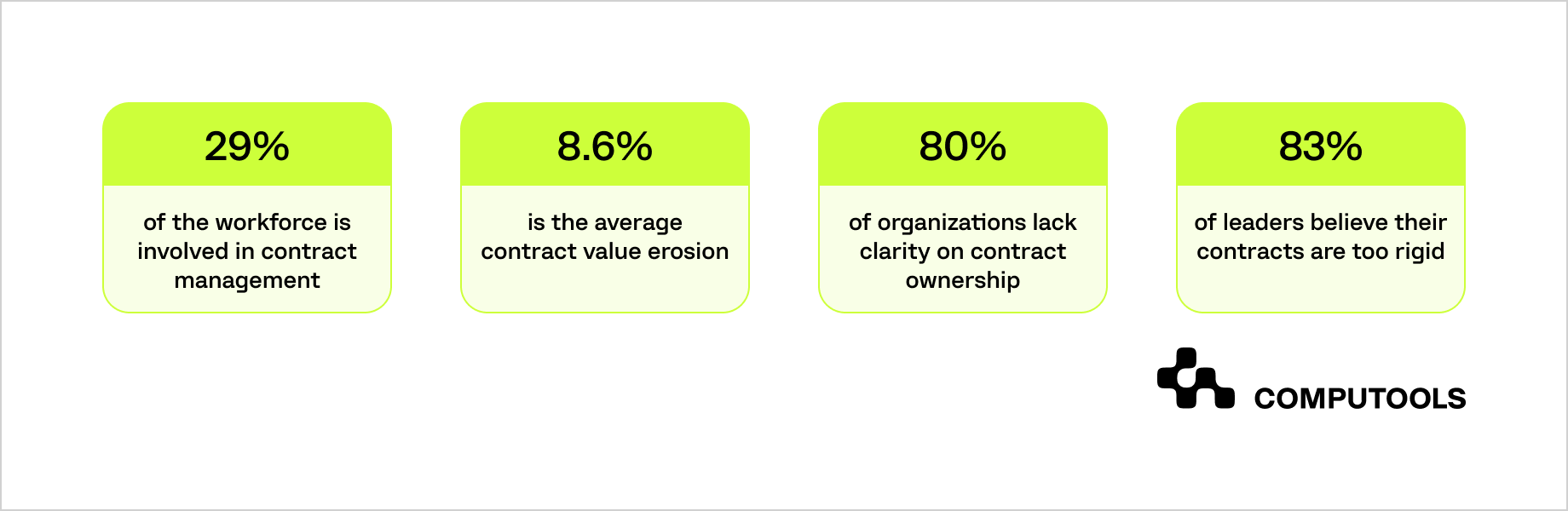

To build a banking contract management system that improves control rather than simply digitizing files, financial institutions must address the value leakage and data gaps embedded in fragmented contract processes. World Commerce & Contracting estimates an average 8.6% erosion in contract value, driven by weaknesses in contract creation, execution, and post-signature management.

The regulatory impact is equally significant. During the European Supervisory Authorities’ DORA dry run, only 6.5% of 947 contractual registers passed all 116 data quality checks. The exercise identified 235,000 failed checks, with missing mandatory information being the most common issue. These gaps make it harder to maintain reliable third-party oversight, prepare regulatory reports, and provide complete evidence during audits.

Modern contract management software for banks centralizes agreements, metadata, approval workflows, obligations, access rights, and audit records across the entire contract lifecycle. By replacing spreadsheets, email approvals, and disconnected repositories, digital contract management in banking gives legal, compliance, procurement, risk, and business teams a controlled source of information for drafting, review, execution, renewal, and termination.

How Computools helped a Swiss bank centralize contract workflows

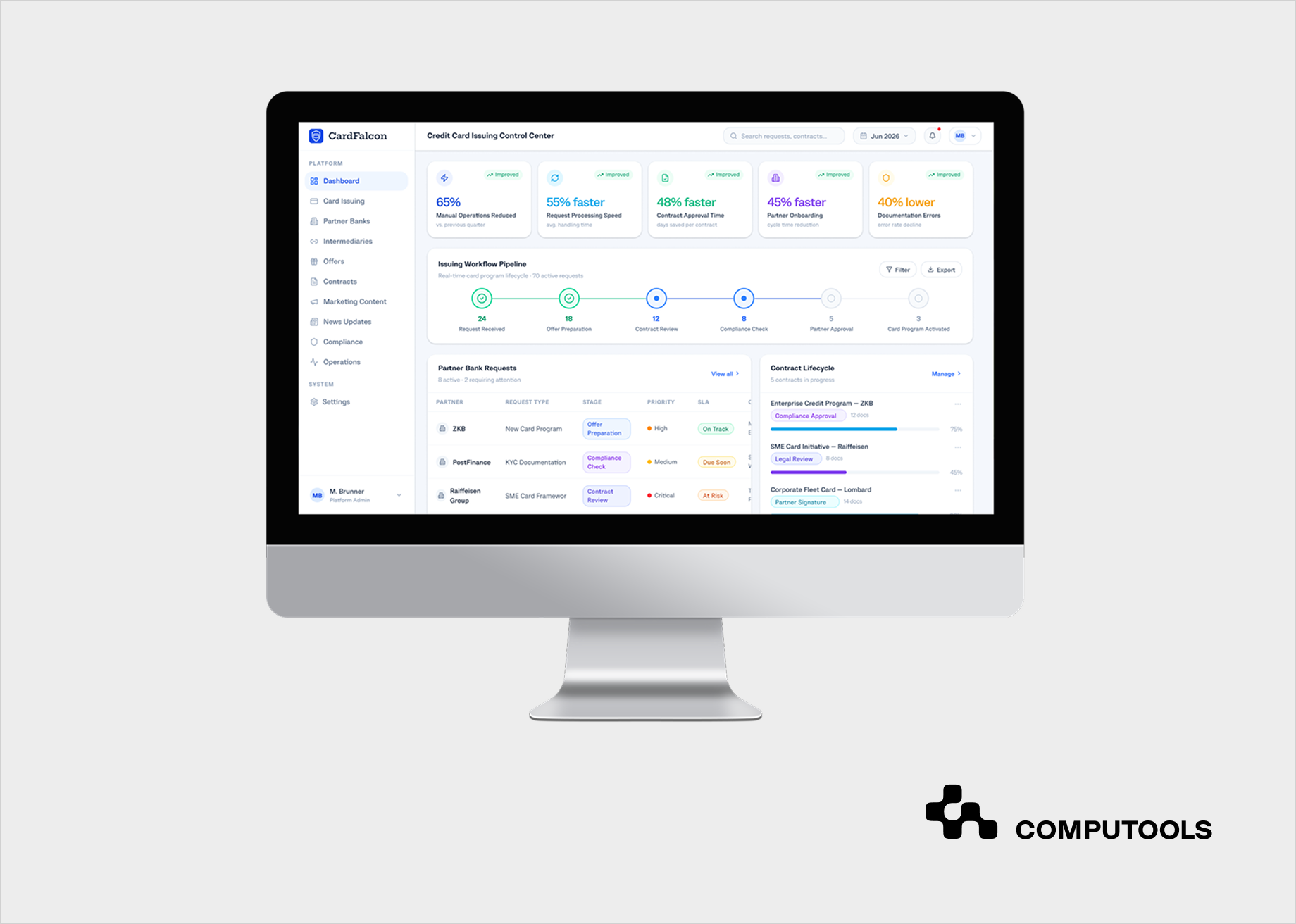

Through its banking software development services, Computools helped a Swiss banking institution replace fragmented contract processes spread across emails, PDFs, spreadsheets, and disconnected internal tools. The client needed a contract management platform for banking that could centralize agreements, offers, partner data, approvals, and operational requests, while supporting multiple user groups in a regulated credit card-issuing environment.

As part of the CardFalcon project, the team combined backend engineering with web development services to implement contracts and offer management functionality. The platform supported contract storage, lifecycle tracking, approval stages, status control, role-based access, and structured communication between internal bank teams, partner banks, and intermediaries. This created contract workflow automation in banking across the wider credit card issuing process and reduced reliance on manual coordination.

The centralized platform reduced manual operations by 65%, shortened contract approval time by 48%, accelerated partner onboarding by 45%, and decreased documentation errors by 40%. Banking request processing also became 55% faster.

The results show how centralized lifecycle control can improve operational visibility when contract records, approvals, partner information, and workflow statuses are managed within a single system.

How to build a contract management system for banking and financial services in 10 steps

A banking contract platform should be designed around the full lifecycle of an agreement, from request and drafting to approval, execution, obligation tracking, renewal, and termination. The development process must connect legal controls with operational workflows, structured data, security requirements, and measurable business KPIs.

Step 1. Define the contract scope, operational problems, and target KPIs

Begin with an inventory of the contracts the institution creates, receives, approves, and maintains. The scope may include agreements with partner banks, payment providers, technology vendors, outsourcing companies, corporate clients, intermediaries, and other third parties. Each category has different approval rules, confidentiality requirements, renewal conditions, regulatory dependencies, and business owners.

The discovery process should document current contract volumes, processing routes, systems, spreadsheets, shared folders, email approvals, and manual handoffs. Teams also need to identify where delays occur, which data must be entered repeatedly, how exceptions are handled, and which agreements create the highest financial or compliance exposure. This analysis prevents the first release from becoming an oversized repository with no clear operational priority.

A contract management solution for financial institutions should be tied to measurable KPIs before software architecture work begins.

Relevant indicators include:

- average drafting and approval time;

- number of manual actions per contract;

- percentage of contracts using approved templates;

- documentation error rate;

- missed renewal and notice deadlines;

- number of unresolved obligations;

- time required to retrieve audit evidence;

- cost per processed contract;

- user adoption across legal and business teams.

The first release should focus on a controlled area, such as partner agreements in a single jurisdiction or vendor contracts for a single business unit. A defined pilot creates a reliable baseline for measuring time savings, error reduction, workflow adoption, and expected ROI before broader implementation.

Step 2. Map the contract lifecycle and governance model

The bank should document every state through which a contract can move, including request, drafting, legal review, commercial review, compliance assessment, negotiation, approval, signature, activation, amendment, renewal, termination, and archival. Each state requires entry conditions, required data, permitted actions, responsible roles, SLA targets, and rules for moving to the next state.

The workflow map must include standard and exceptional paths. A low-risk agreement based on an approved template may pass through a streamlined approval process, whereas an agreement that contains nonstandard liability clauses, cross-border data processing, subcontracting rights, or material outsourcing terms may require additional review by compliance, risk, information security, and executive management.

Effective contract lifecycle management for financial services also depends on a clear governance model.

The platform should define:

- who can create or amend a contract;

- who owns the commercial relationship;

- who approves specific contract values or risk levels;

- who can accept clause deviations;

- who controls templates and policies;

- who may override a workflow;

- which actions require maker-checker approval;

- which responsibilities must remain separated.

These rules should be represented as configurable workflow logic rather than hardcoded into individual screens. The bank can then update approval thresholds, organizational roles, and jurisdiction-specific requirements without rebuilding the entire application. Clear governance reduces stalled agreements, undocumented approvals, and dependence on individual employees who understand an undocumented process.

Contract approvals operate within wider banking processes that include document validation, compliance checks, escalations, and system updates. For a broader implementation model, see our guide on how to develop a banking workflow automation system for financial operations.

Step 3. Design the contract data model and taxonomy

A contract should exist in the system as a structured business entity connected to documents, parties, obligations, approvals, and operational records. Storing a PDF with a filename and upload date is insufficient for search, automation, reporting, or regulatory control.

The canonical data model should define entities such as:

- contract;

- contract type;

- legal entity;

- counterparty;

- business owner;

- product or service;

- jurisdiction;

- clause;

- obligation;

- approval;

- amendment;

- renewal;

- supporting document;

- workflow event;

- audit event.

Each contract record should contain normalized metadata, including effective and expiry dates, governing law, value, currency, notice periods, confidentiality level, risk category, renewal model, responsible department, and current lifecycle status. Relationships should connect the original agreement with amendments, appendices, service schedules, and replacement contracts.

Strong data engineering establishes naming conventions, controlled vocabularies, mandatory fields, validation rules, identifiers, and data ownership across departments. It also determines which system owns counterparty information, which fields come from CRM or procurement tools, and how conflicting values are resolved.

The model should preserve data lineage. Users and auditors need to know whether a field was entered manually, imported from another system, extracted by AI, or updated through an integration. Validation rules can block incomplete records from advancing into approval or execution, reducing the missing data that later creates reporting and audit problems.

For a broader framework covering data ownership, quality, access, integrity, and governance responsibilities, see data governance in Fintech software development.

Step 4. Define the system architecture and security controls

The technical architecture should separate document storage, contract metadata, workflow orchestration, business rules, integrations, search, analytics, and identity management. A modular design allows the bank to change approval logic, add contract categories, or replace an external service without affecting the entire platform.

A typical architecture may include:

- object storage for contracts and supporting files;

- a relational database for structured contract records;

- a workflow or business process engine;

- a rules engine for routing and approval decisions;

- a search index for full-text and metadata search;

- an API layer for banking and third-party integrations;

- an event bus for asynchronous updates;

- an identity and access management layer;

- monitoring, logging, and audit services.

Requirements for secure document management for financial institutions should be defined before implementation begins. The platform may need role-based and attribute-based access controls, single sign-on, multifactor authentication, encryption in transit and at rest, managed encryption keys, document-level permissions, session controls, and restrictions based on legal entity or jurisdiction.

Sensitive actions require additional protection. Contract deletion, permission changes, approval overrides, document exports, and changes to retention rules should be logged with the user, timestamp, previous value, new value, and justification. Audit records must be protected from modification by ordinary users.

The architecture should also cover backup, disaster recovery, data residency, retention, legal holds, and secure disposal. These controls reduce unauthorized exposure and ensure that contracts remain accessible during audits, operational incidents, or disputes.

Step 5. Build the document repository and migration pipeline

The repository should provide a single controlled location for executed agreements, drafts, amendments, schedules, evidence of approval, correspondence, and related operational documents. Each file must remain linked to the structured contract record, the current lifecycle state, the responsible owner, and the complete version history.

Core repository capabilities should include:

- file classification;

- metadata-based and full-text search;

- version control;

- document comparison;

- amendment relationships;

- duplicate detection;

- checksums and integrity validation;

- retention and archival rules;

- legal holds;

- access history;

- download and export controls.

Centralized banking document management reduces the risk of employees reviewing outdated versions or storing executed documents in personal mailboxes and local folders. It also shortens the time required to retrieve the agreement, its approval history, and related evidence during a review.

Migration should run as a controlled data pipeline rather than a one-time bulk upload. The process should extract files and metadata from shared drives, CRM records, spreadsheets, legacy repositories, and email archives. Records then need classification, duplicate resolution, metadata normalization, ownership assignment, validation, and reconciliation against source systems.

Contracts with missing owners, dates, counterparties, or final versions should be moved to an exception queue for manual review. Migration dashboards should show imported records, rejected files, duplicate groups, incomplete metadata, and unresolved exceptions.

Step 6. Configure templates, clauses, approvals, and workflow automation

The system should provide controlled templates for recurring agreement categories. Templates may vary by jurisdiction, counterparty type, product, legal entity, contract value, and risk classification. Each template requires an owner, an approval date, a valid period, a version history, and rules defining where it may be used.

A clause library should store approved language, alternative clauses, fallback positions, prohibited wording, and mandatory provisions. When a user modifies a standard clause, the system should record the deviation and route it to the correct legal or compliance reviewer. This reduces repeated manual comparison and helps teams focus on material changes.

The workflow engine should support:

- sequential and parallel reviews;

- conditional routing;

- approval thresholds;

- delegated authority;

- maker-checker controls;

- return for revision;

- reassignment;

- SLA timers;

- escalation;

- approval expiry;

- override justification;

- electronic signature integration.

Workflow logic should rely on contract data. A low-value domestic agreement may follow a standard route, but a cross-border outsourcing agreement involving customer data access requires extra security, privacy, operational risk, and approvals.

Role-specific workspaces should show reviewers their pending tasks, deadlines, contract context, previous comments, clause deviations, and actions. Business users need clear status updates without accessing restricted legal or compliance information.

CardFalcon connected contract approvals with partner records, offers, operational requests, and user roles. The delivered system shortened contract approval time by 48% and reduced documentation errors by 40%, showing the operational effect of structured routing and centralized status control.

Step 7. Add obligation, renewal, and regulatory controls

Execution transfers a contract into active management. The platform should convert contractual commitments into structured obligations with an owner, due date, recurrence pattern, evidence requirement, status, and escalation route.

Trackable obligations may include:

- payment and pricing conditions;

- reporting deadlines;

- service-level commitments;

- security assessments;

- insurance requirements;

- audit rights;

- data deletion duties;

- subcontractor notifications;

- license renewals;

- termination notice periods;

- policy and compliance reviews.

A scheduler should generate tasks and reminders based on effective dates, review cycles, renewal windows, and notice periods. Escalation rules should notify the business owner and the relevant control function when an obligation becomes overdue or when evidence is not attached.

Effective contract compliance management for banks also requires a connection between obligations and their source clauses. Reviewers should be able to trace a task back to the exact contractual provision, document version, responsible party, and approval history. This traceability improves audit preparation and reduces disputes over why an action was required.

Regulatory controls should be configurable by contract category, jurisdiction, counterparty, and risk level. The system can require specific fields, clauses, assessments, approvals, and reports before a contract is signed or renewed. For ICT third-party arrangements, the platform may also maintain the structured data needed for DORA contractual registers and related oversight.

Compliance dashboards should show missing mandatory data, expired assessments, overdue obligations, high-risk deviations, contracts approaching renewal, and agreements without assigned owners. These views turn contract compliance into an ongoing operational process rather than a periodic manual review.

Step 8. Implement AI-assisted extraction and contract review

AI can reduce the time required to classify legacy contracts and populate structured records. The processing pipeline may combine optical character recognition, document parsing, language detection, entity extraction, clause classification, and comparison against approved language.

Use cases for banking legal document automation include extracting:

- parties and legal entities;

- effective and expiry dates;

- monetary values and currencies;

- governing law;

- renewal and termination terms;

- service obligations;

- data protection clauses;

- audit rights;

- subcontracting provisions;

- liability limits;

- change-of-control clauses.

The extracted data should include a confidence score and a reference to the exact page, paragraph, or clause from which it was obtained. Low-confidence fields and high-risk provisions should enter a review queue rather than be accepted automatically.

Clause comparison identifies differences between agreements and templates, while a retrieval layer helps users find similar clauses, past negotiations, or policies quickly. AI governance is essential because data can impact approvals, obligations, and reports. It should include versioning, access limits, redaction, evaluation datasets, output monitoring, and human correction records. Approved users are responsible for legal and compliance decisions.

The bank should measure AI performance by field and contract category rather than relying on a single overall accuracy score. Dates may be extracted reliably, while complex termination rights still require extensive review. This level of measurement helps determine which tasks can be automated and where manual control remains necessary.

Step 9. Integrate the platform with banking and enterprise systems

The contract platform should exchange data with the systems that create counterparties, initiate purchases, approve vendors, process payments, and monitor risk. Without these integrations, employees still have to copy contract information manually, and the institution retains multiple conflicting versions of the same record.

When contract workflows depend on counterparty verification, document checks, sanctions screening, and risk-based review, the integration should remain aligned with the wider compliance process. See how to develop an automated KYC verification system for financial institutions.

Common integration points include:

- CRM;

- core banking systems;

- procurement platforms;

- ERP and accounting tools;

- KYC and KYB systems;

- third-party risk management;

- identity and access management;

- e-signature services;

- payment and billing systems;

- data warehouses;

- regulatory reporting tools.

Experience in fintech software development is required to define data ownership and transaction behavior across these systems. The integration design should specify which platform is the source of truth for counterparties, legal entities, products, payment terms, and contract status.

Synchronous APIs can support actions that require an immediate response, while asynchronous events are better suited to contract status changes, completed signatures, new obligations, or updated counterparty risk ratings. Integration services should support authentication, authorization, schema validation, idempotency, retries, timeout handling, and dead-letter queues.

Each integration also needs reconciliation controls. The platform should detect contracts with missing counterparty records, payment terms that differ from the ERP, failed signature callbacks, or status updates that have not reached downstream systems. Operational dashboards help support teams resolve failures before they affect payments, renewals, or compliance reporting.

For CardFalcon, CRM-related functionality, contract logic, partner information, offers, workflow statuses, and database records were integrated into a single platform. Salesforce supported centralized partner and operational data, while Java, Spring, Angular, PostgreSQL, and Docker formed the application and infrastructure layers.

Step 10. Test the platform, launch a pilot, and scale by KPI

Testing should cover the complete contract lifecycle rather than isolated screens. End-to-end scenarios need to verify contract creation, template selection, clause changes, approvals, signatures, obligation generation, amendments, renewals, termination, and archival.

The test strategy should include:

- unit and integration testing;

- workflow and rules-engine testing;

- role and permission testing;

- migration reconciliation;

- API contract testing;

- performance and load testing;

- security testing;

- backup and recovery testing;

- user acceptance testing;

- audit-log validation.

Permission testing deserves particular attention. Teams should verify that users can access only the contracts, fields, documents, and actions permitted by their roles, legal entities, jurisdictions, and business relationships. Negative scenarios should confirm that unauthorized approvals, downloads, exports, and overrides are blocked and logged.

The pilot should cover one controlled contract portfolio with real users and integrations. Legal, compliance, procurement, risk, and business teams should test standard agreements, exceptions, incomplete data, rejected approvals, expired tasks, integration failures, and renewal scenarios. Observed issues can then be corrected before a wider rollout affects multiple departments.

A phased model for financial software development services reduces execution risk by linking each rollout stage to measurable acceptance criteria.

After the pilot, the institution should compare results against the original baselines:

- contract cycle time;

- approval duration;

- manual actions;

- documentation defects;

- obligation completion;

- renewal control;

- audit preparation time;

- user adoption;

- support volume.

The CardFalcon project used short delivery iterations and regular checkpoints to refine backend logic, approval flows, interfaces, database integration, and IT infrastructure before broader rollout.

Launch your banking contract management system within 1–3 months instead of years, giving every team a single source of truth for contracts, approvals, and compliance.

Key risks in banking contract management system implementation

| Risk | Business impact | How to reduce it |

| Poor contract data quality | Duplicate files, missing metadata, and outdated versions weaken search, automation, and reporting. | Validate, classify, deduplicate, and reconcile records before migration. |

| Rigid approval logic | Nonstandard clauses, high-risk agreements, and cross-border contracts may fall outside fixed workflows. | Use configurable routing, parallel reviews, escalation rules, and controlled overrides. |

| Unclear data ownership | Conflicting values across CRM, ERP, procurement, and contract systems create errors in payments, renewals, and reporting. | Define a source of truth for each data field and implement validation and reconciliation controls. |

| Weak security and audit controls | Broad permissions and incomplete logs increase the risk of unauthorized access and reduce audit readiness. | Apply role-based access, immutable audit trails, retention rules, legal holds, and traceable overrides through regulatory compliance software for banks. |

Addressing these risks pre-rollout ensures reliable contract data, functional approval workflows, and complete compliance evidence. A phased approach with validated migration, controlled integrations, and KPI checkpoints reduces manual work and prevents legacy failures from transferring to the new platform.

Why financial institutions choose Computools

Banking contract platforms have to meet regulatory, security, integration, and operational requirements before they can deliver measurable value. Computools reduces this execution risk through phased delivery, pilot validation, KPI-based checkpoints, and one delivery team covering product strategy, architecture, UX, automation, analytics, and launch.

This model is supported by 250+ experts, experience across 10+ banking projects, a 4.9 Clutch rating based on 95+ reviews, and the ability to launch a scoped first release within 1–3 months, depending on requirements and integration complexity.

Delivery is structured around phased implementation, pilot validation, and clear checkpoints. Computools first maps contract workflows, data sources, user roles, compliance dependencies, and target KPIs. The team then validates the architecture, workflow logic, and user experience within a controlled scope before expanding the system across additional contract types, departments, or jurisdictions. This approach limits the cost of late corrections and creates a clearer roadmap to ROI.

For banking contract platforms, Computools combines backend engineering, product design, analytics, AI development, and cybersecurity services into a single delivery model. AI can support metadata extraction, clause classification, and obligation detection, while security controls cover access management, encryption, audit trails, document handling, and traceable approvals. Legal and compliance decisions remain under authorized human review.

The delivery model is supported by measurable results. In the CardFalcon project, the implemented platform reduced manual operations by 65%, shortened contract approval time by 48%, decreased documentation errors by 40%, accelerated partner onboarding by 45%, and made banking request processing 55% faster.

In another project, platform and product engineering helped Caribbean Bank increase its market share among customers aged 18–30 by 12%.

Computools remains responsible for launch, validation, and post-release optimization. After deployment, the team tracks adoption, cycle time, exception rates, documentation quality, compliance performance, and operational savings against agreed KPIs.

Email us at info@computools.com to discuss how to reduce contract processing time, manual work, and implementation risk.

Conclusion

Effective banking contract lifecycle management provides financial institutions with consistent control over contract data, approvals, obligations, renewals, and evidence of compliance. A phased rollout tied to clear KPIs helps reduce manual work, shorten approval cycles, and scale contract operations without increasing operational risk.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.