THE AUTHOR:

Organizations are required to develop a risk scoring engine to adapt to the changing landscape of fraud, AML exposure, customer onboarding, and payment-related risks, which have gone beyond rigid rule-based analysis. The multitude of customer service channels and third-party integrations creates risk signals that jeopardize revenues, compliance, trust, and the ability to conduct business as usual.

This also requires strong banking compliance risk management and anti-money laundering risk scoring to ensure accurate evaluation of financial crime exposure.

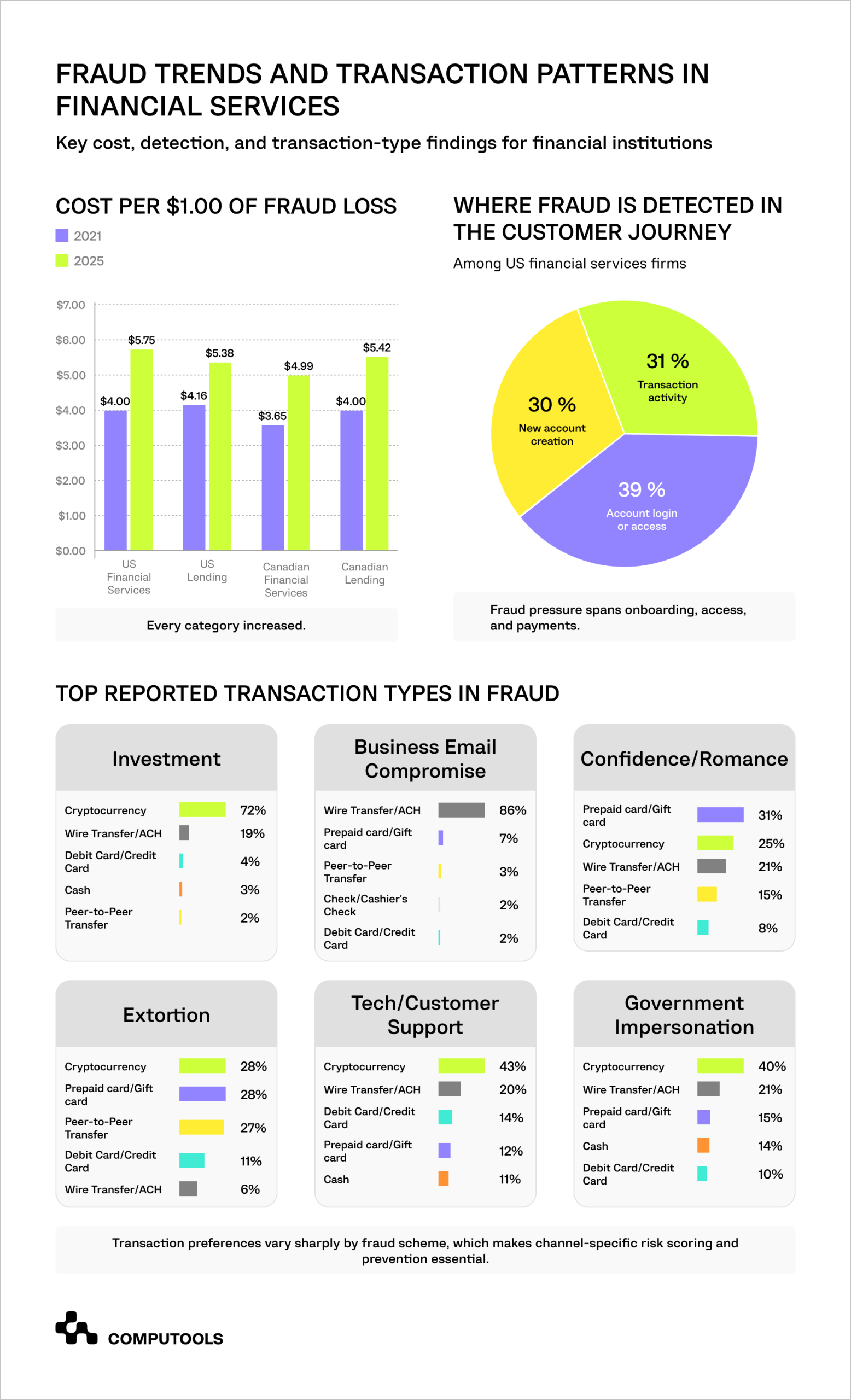

The pressure comes most from regulators and central banks, law enforcement, and financial intelligence units. The FBI’s 2025 Internet Crime Report states that cyber-enabled crimes caused just under $21 billion in economic loss in the U.S. Complaints involving cryptocurrency and violations aided by artificial intelligence ranked among the most expensive. The FTC cites that in 2025 U.S. consumers lost about $16 billion due to fraudulent schemes. This was the highest level of losses recorded and represented a 25% increase compared to 2024.

AML pressure is increasing as well. The UK Financial Intelligence Unit reported 866,616 Suspicious Activity Reports in 2024–25, showing the scale of financial crime monitoring workloads for regulated firms. At the same time, fraud techniques are becoming more automated.

According to INTERPOL’s 2026 Global Financial Fraud Threat Assessment, AI-enabled fraud is believed to be 4.5 times more lucrative than conventional fraud. Europol’s IOCTA 2026 also expresses concerns that online fraud will employ AI for social engineering, management of infrastructure, and more automated criminal workflows.

These figures describe the need for banks and fintech to employ complex risk scoring for evaluating transactions, customer profiles, devices, counterparties, AML alerts, and behavioral patterns in near real time. Static checks can still support compliance rules, but they are no longer enough to manage fast-moving fraud, payment risk, onboarding risk, and analyst workload.

What features should a risk scoring system for banking and finance have?

| Industry trend | What it means for banks and fintech companies | Features the risk scoring system should include |

| AI-driven fraud and scams are increasing | Fraudsters use automation, synthetic identities, deepfakes, and bot activity to test controls faster than manual teams can respond. | AI-powered risk scoring, anomaly detection, bot behavior analysis, device intelligence, behavioral profiling, and explainable fraud reasons. |

| Payment fraud is growing across credit transfers and card payments | Banks need to score transactions before approval, not only investigate them after losses occur. | Real-time transaction scoring, payment hold logic, velocity checks, counterparty risk scoring, step-up verification, instant alert routing. |

| Instant payments reduce reaction time | Fraud and AML controls must work within seconds while keeping legitimate transactions moving. | Stream processing, low-latency scoring APIs, automated decision bands, fallback rules, asynchronous enrichment, transaction risk queues. |

| Static AML rules create too many low-value alerts | Compliance teams need better prioritization instead of larger alert volumes. | AML risk scoring, customer clustering, rule tuning, false-positive tracking, alert prioritization, case scoring, analyst feedback loops. |

| Digital onboarding and eKYC adoption are growing | Customer verification quality now affects fraud exposure, onboarding completion, and future risk segmentation. | KYC data ingestion, document verification status, liveness check results, identity confidence score, onboarding risk score, reverification triggers. |

| Fraud often appears after onboarding | One-time KYC is not enough when risk changes during daily customer activity. | Continuous customer profile risk analysis, lifecycle scoring, device and session monitoring, customer behavior baselines, periodic risk refresh. |

| Banks are adopting AI for fraud, AML, profiling, and customer segmentation | AI can improve prediction and detection, but it needs governance, clean data, and explainable output. | Feature store, model monitoring, model versioning, reason codes, confidence scores, human review controls, drift detection. |

| Regulatory pressure requires traceable decisions | Risk teams must prove why a transaction was held, why a customer was escalated, or why an alert was closed. | Audit logs, decision history, rule versioning, model versioning, evidence storage, role-based access control, compliance reports. |

| Fraud teams face higher workload and support pressure | Manual reviews delay trusted customers and pull analysts away from high-risk cases. | Case management, SLA tracking, queue prioritization, analyst dashboards, AI-generated case summaries, escalation workflows. |

| Financial products depend on partner APIs and third-party data | Risk scoring must connect internal systems with KYC, AML, payment, fraud, CRM, and reporting tools. | API orchestration, provider fallback logic, data normalization, secure integrations, consent controls, integration monitoring. |

These trends explain why a banking risk scoring system should be designed around decisions, not alerts. The system should define what happens when risk appears: approve the transaction, request verification, create a case, hold payment, update the customer segment, or escalate to compliance.

The operational control benefit for leadership is clear. A risk scoring engine can decrease the number of reviews and approvals, allow faster customer onboarding, identify suspicious activity sooner, and provide better support to compliance units with evidence of risks. It also provides safer methods to accelerate the use of digital payments and embedded finance, customer lending, digital wallets, and marketplace transactions.

This article explains how to develop a risk scoring engine for banking transactions and customer profiles, what architecture decisions matter, how AI and rules should work together, and how Computools approaches scalable, secure, and commercially useful risk scoring platforms.

How to develop a risk scoring engine: Computools experience

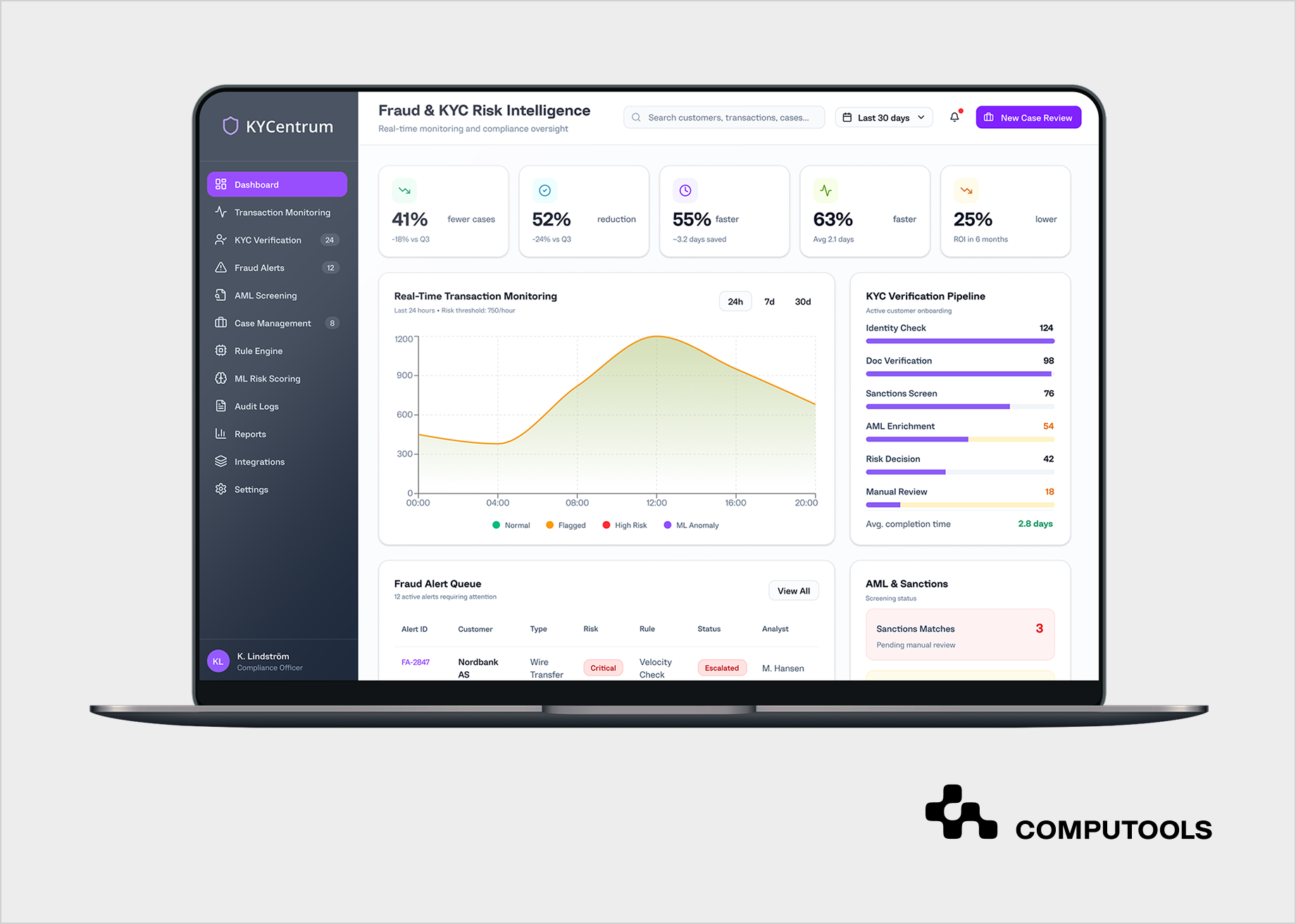

KYCentrum shows why risk scoring should work as part of a larger fraud, AML, KYC, and case management workflow, not as a separate scoring tool.

The client was a European finance institution operating in Estonia, Latvia, and Lithuania. They wanted to create a solution with better fraud prevention and customer verification for their full suite of digital banking services (including payments, cards, loans, leasing, savings, pensions, and private banking).

Fraud detection and risk scoring were based on static rules combined with manual case reviews. The client was not able to make fast decisions as the fraud alerts, KYC, and AML risk scoring, transaction data, and case history were not adequately connected. As a result, they had poor onboarding and a high rate of false positives, which created a larger workload for their analysts and an increase in costs for compliance.

Computools built the customer a fraud prevention and compliance platform that unites the real-time monitoring of transactions, automated KYC and AML, and rule-based decisioning with machine learning fraud scoring and case management.

For the backend development, we used Java and Spring Boot, while ML models were used for detecting anomalies, along with Apache Kafka for real-time data streams, PostgreSQL for structured data and audit trails, and Drools/Camunda for adaptive business rule logic. The system was built with explainable AI, secure APIs, and encrypted data transmission and monitoring, along with an audit-ready reporting capability.

Business result:

• confirmed cases of fraud dropped by 41%;

• false-positive alerts decreased by 52%;

• client onboarding time shortened by 50-60%;

• case resolution time increased by 63%;

• operational compliance costs fell by 20-30%.

The case study illustrates an essential development principle: the risk-scoring system must be integrated with client verification, transaction monitoring, and anti-money laundering (AML) processing, and linked directly to the analyst case workflow and audit trails.

This challenge solved in this project is closely connected to AML transaction monitoring, where banks need to detect suspicious behavior, prioritize alerts, and keep investigation records ready for compliance review.

Computools covers this process in more detail in its article on how to build an AML transaction monitoring system.

How to develop a risk scoring engine for banking transactions and customer profiles

To develop a risk scoring engine, start with the business decisions it must control. The system should not only calculate a score. It should decide what happens next: approve, hold, verify, decline, escalate, or send to manual review.

1. Define What the Score Should Decide

First, define where the risk score will affect operations. For banks and fintech companies, this may include onboarding, login, card payments, transfers, loan applications, merchant payouts, account recovery, or customer profile changes.

Each score should trigger a clear action. For example:

• low risk: approve automatically;

• medium risk: request step-up verification;

• high risk: send to analyst review;

• critical risk: block, hold, or escalate.

Risk, compliance, fraud, product, and operations teams of the customer should agree upon the rule logic before development begins, in order to avoid a situation in which the system provides scores that require manual interpretation.

From a system design perspective, this involves a decision matrix, configurable rules and thresholds, reason codes, and event-driven business rules. All decisions of the system should be captured along with the score, input parameters, business rule version, model version, timestamp, and the action taken.

2. Build a Unified Risk Data Model

A risk scoring engine for banking depends on connected data. Customer data, transactions, devices, KYC checks, AML screening, login behavior, and past fraud cases often sit in different systems. The engine needs a data model that brings these signals together.

The core data model should include:

• customer profile;

• account history;

• transaction records;

• device and session data;

• geolocation;

• counterparty data;

• KYC verification status;

• sanctions, PEP, and AML screening results;

• previous alerts;

• analyst decisions;

• audit logs.

This context improves scoring accuracy. A payment may look normal alone, but become risky when linked to a new device, an unusual country, a new beneficiary, a high-risk counterparty, and an incomplete KYC record.

In the KYCentrum project, Computools connected KYC, AML enrichment, fraud signals, transaction monitoring, and case history in one workflow. The same principle applies to any financial risk assessment software: the engine needs full customer and transaction context to support better decisions.

Computools explains this process in its guide on how to develop an automated KYC verification system.

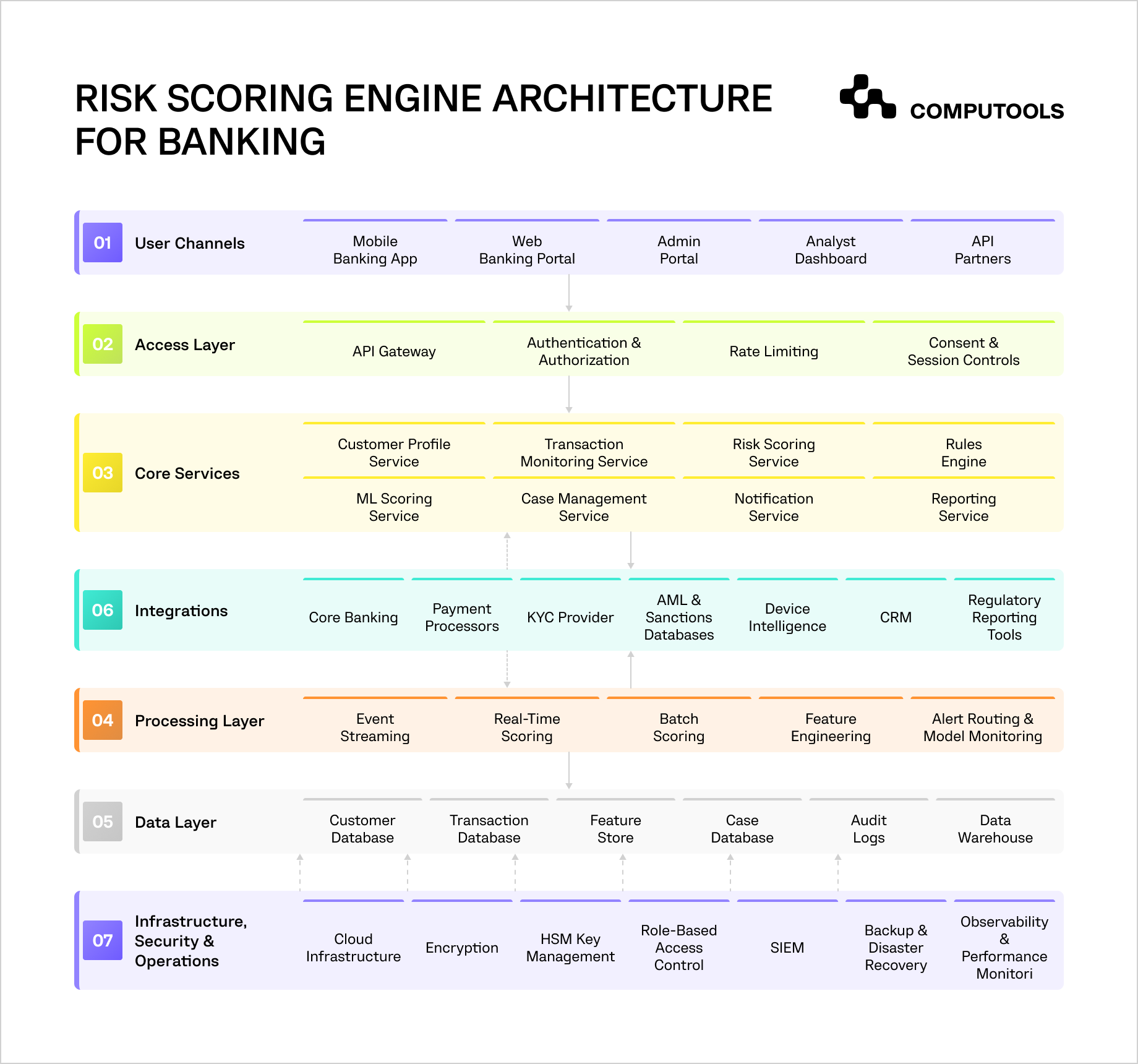

3. Choose Real-Time and Batch Scoring Logic

Next, decide which checks must happen instantly and which can run in the background. Real-time risk scoring is important for payments, logins, beneficiary changes, account recovery, and card transactions. Batch scoring works better for periodic customer reviews, profile refreshes, regulatory reporting, and model recalibration.

A practical architecture may include:

• API gateway for secure service access;

• event ingestion layer for transaction and customer events;

• stream processing for real-time scoring;

• rules engine for compliance and fraud logic;

• ML scoring service for anomaly detection;

• feature store for reusable risk signals;

• case management module for analysts;

• audit and reporting layer.

Latency is important. If the transaction risk scoring engine is too slow, customers wait during payments or onboarding. If scoring happens only after approval, fraud may pass before teams can react.

For high-risk actions, score the event before approval. For lower-risk events, score asynchronously and route suspicious activity to review.

4. Combine Rules With AI Models

Rules and AI should work together. Rules are best for clear compliance logic: sanctions hits, blocked countries, transaction limits, suspicious velocity, failed KYC, or known fraud patterns. AI models are useful for behavior that is harder to define manually, such as account takeover patterns, mule activity, synthetic identities, unusual transaction sequences, or sudden changes in customer behavior.

A practical hybrid model includes:

• rule-based score components;

• ML-based anomaly score;

• customer profile risk score;

• transaction risk score;

• AML risk score;

• final combined risk score.

The system should explain every high-risk decision. Analysts need reason codes, triggering signals, model version, confidence level, and rule history. For example, a transfer may be flagged because it comes from a new device, involves a high-risk counterparty, exceeds the customer’s normal amount, and follows several failed login attempts.

If the rules are too rigid, false positives increase. If AI is difficult to explain, compliance teams may reject the output. The goal is a controlled AI-powered risk scoring engine where automation improves detection without removing human accountability.

Computools also explains this approach in its guide on how to build a real-time fraud detection platform.

5. Design Customer Profile Risk Analysis

Customer risk can change for a variety of reasons after a customer has been onboarded. These risks may include changes in account ownership, the emergence of new counterparties, the presence of transactions that are inconsistent with a customer’s profile, multiple failed attempts to verify a customer, suspicious behavior of the device used to access the customer’s account, and more.

The customer risk scoring model should adjust after such key events:

• new device login;

• large transfer;

• cross-border payment;

• new beneficiary;

• failed identity check;

• sanctions or PEP match;

• repeated chargebacks;

• unusual business activity;

• suspicious counterparty activity.

This helps to optimize risk-based customer segmentation, where low-risk accounts go through the organizational workflows with minimal disruptions and high-risk clients are processed with intensified scrutiny.

From a system perspective, transaction monitoring software should capture the history of a profile score along with the risk factors, customer segment, review status, and what initiated the change. This will help the compliance function better understand the determinants of risk associated with a customer over time.

6. Add Predictive Analytics and Automation

Modern platforms offer predictive risk analytics for banking. However, AI relies on organized and clean data. Consistent records of transactions, defined case outcomes, dependable customer profiles, and standardized event data are prerequisites for integrating predictive analytics.

Useful features include:

• anomaly detection for unusual payments or account behavior;

• fraud detection based on customer behavior changes;

• alert prioritization by severity and business impact;

• customer segmentation by risk pattern;

• analyst summaries for flagged cases;

• smart search across customers, transactions, rules, entities, and cases;

• workload forecasting for compliance teams;

• automated regulatory reporting;

• personalized verification prompts for customers.

These are meant to decrease the manual workload. For instance, an AI-enhanced case summary should present the customer’s profile, transaction history, the signals and alerts that the case is built on, and the next action steps. The analyst is still responsible for the ultimate decision; however, the case is built and ready for a review.

7. Build Analyst Workflows and Admin Controls

Risk scoring becomes meaningful if the teams act upon the outcomes. An analyst workspace should contain an alert queue, case scoring, and transactional history, along with reason codes, supporting evidence and notes, escalation, SLAs, and a complete case history.

Risk managers also require administrative controls and permission for setting and adjusting business thresholds, rules and conditions, along with custom queues, as well as controls pertaining to case analytics and performance metrics.

They should be able to see:

• which rules create too many false positives;

• which customer segments carry the highest risk;

• which alerts are urgent;

• how long case resolution takes;

• which analysts are overloaded;

• which fraud patterns are increasing.

From a technical point of view, real-time risk scoring for banks and other financial institutions requires role-based permissions, workflow states, rule configuration, queue management, audit logging, and reporting dashboards. Without these workflows, the system may create more alerts without improving operations.

8. Secure, Test, and Improve the Engine After Launch

A risk scoring engine handles sensitive customer data, transaction data, identity records, fraud signals, and compliance evidence. Security should protect trust, continuity, and revenue.

The system should include:

• encryption in transit and at rest;

• role-based access control;

• secure API integrations;

• data masking;

• key management;

• audit logging;

• incident monitoring;

• backup and recovery;

• disaster recovery planning;

• model monitoring.

The testing process should cover rule accuracy, scoring latency, peak transaction load, provider failures, user permissions, audit trail consistency, false-positive rates, and model output quality.

After launch, track confirmed fraud, false positives, manual review volume, onboarding time, transaction approval latency, case resolution time, analyst workload, and model drift. Analyst feedback, confirmed fraud cases, and false positives should feed future rule tuning and model updates.

A banking risk scoring system should improve with every decision. The more structured the feedback loop, the stronger the system becomes over time.

Launch your AI-powered banking risk scoring engine within 1–3 months instead of years, equipping every transaction and customer decision with real-time intelligence, stronger fraud prevention, and enterprise-grade compliance from day one.

Why choose Computools for risk scoring engine development

Risk scoring fails when it stays separate from banking fraud prevention technology and daily operations. Computools designs it as a decision system that controls what happens after every score: approve, verify, hold, escalate, report, or review.

The work starts with the business logic behind risk. Computools maps where fraud, AML, onboarding, payments, and customer profile checks slow the organization down. Then the team turns those points into scoring rules, workflows, integrations, dashboards, and measurable KPIs.

This matters when teams face the same operational problems every day:

• analysts spend hours on weak alerts;

• good customers wait during onboarding;

• fraud teams lack full transaction context;

• compliance teams need clear evidence for decisions;

• risk managers cannot see which rules create noise;

• product teams need risk controls that scale with new payment flows.

Computools solves these problems by connecting the risk engine to the systems around it. Our financial software development services bring customer profiles, transaction history, KYC records, AML checks, fraud signals, and case history into one risk view. This gives risk teams the full context behind each score and reduces the time spent switching between tools.

Through our banking software development services, Computools helps companies turn data into traceable decision logic. We build scoring logic, rule engines, audit trails, and analyst workflows that keep decisions traceable. Low-risk activity moves faster. High-risk activity goes to the right queue with clear reasons and evidence.

For fintech products involving wallets, lending, payment, and marketplace platforms, Computools leverages its fintech software development expertise to integrate risk scoring with onboarding, transaction limit controls, payment and merchant payout approvals, partner API integrations, and customer segmentation. The integrated approach brings risk control to revenue-generating business flows, rather than distancing it to compliance functions.

Computools also builds the internal tools risk teams need to act faster. Through web development services, the team creates analyst dashboards, admin portals, case queues, SLA views, threshold controls, and reporting screens. Risk managers can see which alerts create false positives, which segments carry higher exposure, and where manual review slows the business.

With the additional value of AI development, Computools develops functional tools that bring a higher level of automation to anomaly detection, predictive scoring, prioritization and alerting, behavioral case analysis, and case summarization.

Computools’ cybersecurity services protect customer data, transaction records, identity checks, and compliance evidence through access control, encrypted data flows, secure APIs, audit logging, monitoring, and incident visibility.

The result is a risk scoring engine that does more than flag suspicious activity. It reduces fraud exposure, cuts unnecessary reviews, speeds up trusted customers, gives compliance teams defensible records, and gives leadership clearer control over risk, revenue, and operations.

Develop a risk scoring engine around decisions, not alerts

A risk scoring engine should change how the business reacts to risk. It should decide when to approve a payment, pause a transfer, request extra verification, send a case to an analyst, lower a customer limit, or trigger enhanced due diligence.

This matters because most risk problems are operational. Fraud teams lose time on weak alerts. Compliance teams need regulatory compliance automation with evidence for every decision. Product teams want fast onboarding without exposing the business to fraud. Operations leaders need fewer manual reviews, clearer queues, and better control over transaction flow.

A risk scoring engine that generates value for banking and fintech firms requires a variety of capabilities in addition to models and thresholds. These include the ability to connect data, real-time scoring, customer profile risk assessment, AML, anti-fraud logic, explainable decisions, analyst-friendly workflows, audit trails, and the ability to adjust and fine-tune the engine after it goes into production.

The objective is to approve trusted activity faster, stop risky activity earlier, and give teams enough context to act with confidence.

Every false positive costs you customers. Every false negative costs you money. Let’s rebalance both. Plan your risk scoring engine with Computools. Talk to our team at info@computools.com.

For companies comparing technology partners, Computools’ overview of top fintech software development companies gives a broader view of vendor capabilities in banking, payments, compliance, and financial product development.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.