THE AUTHOR:

Blockchain has emerged as a huge technological narrative over the last decade, captivating everyone’s attention. However, despite all the discussions, there often is a lack of clear understanding of the nature and purpose of blockchain technology.

Yet, at its core, the blockchain’s concept is quite straightforward. This technology allows any person or business worldwide to conduct transactions directly with others securely, bypassing middlemen.

The current state of blockchain development is still in its early stages. Nonetheless, Gartner forecasts that by 2030, blockchain could unlock up to US$3.1 trillion in new business value.

In order to help you answer the question “What is blockchain?” we have created this comprehensive overview that explains its distinct advantages for businesses beyond other technologies and forecasts its progression over the coming decade.

The History of Blockchain

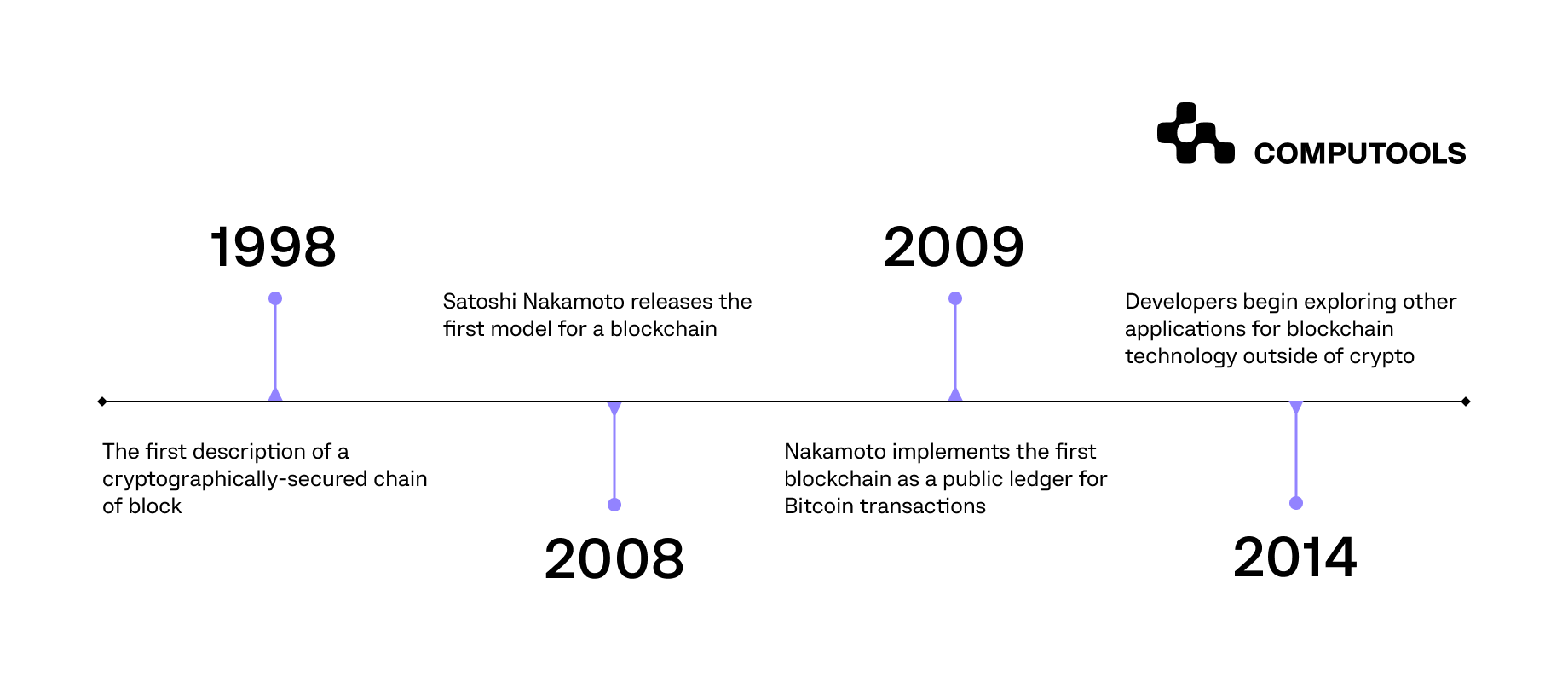

Stuart Haber and W. Scott Stornetta first introduced the idea of a secure chain of blocks in 1991. However, the real innovation occurred in 2008 when Satoshi Nakamoto, the anonymous creator of Bitcoin, shared the first detailed outline of blockchain technology.

Nakamoto then put this theory into practice by launching the Bitcoin blockchain in 2009, positioning the technology as a distributed ledger for cryptocurrency transactions.

By 2014, the tech community began looking beyond cryptocurrency, exploring the broader potential of blockchain.

This led to the creation of the Ethereum blockchain, which introduced smart contracts — a significant innovation that we’ll discuss later.

Today, blockchain is used across various business sectors, extending far beyond its original application.

With its growing popularity, we are constantly discovering new and exciting ways to apply blockchain in order to address complex challenges, enhance efficiency, and transform business practices globally.

How Blockchain Works

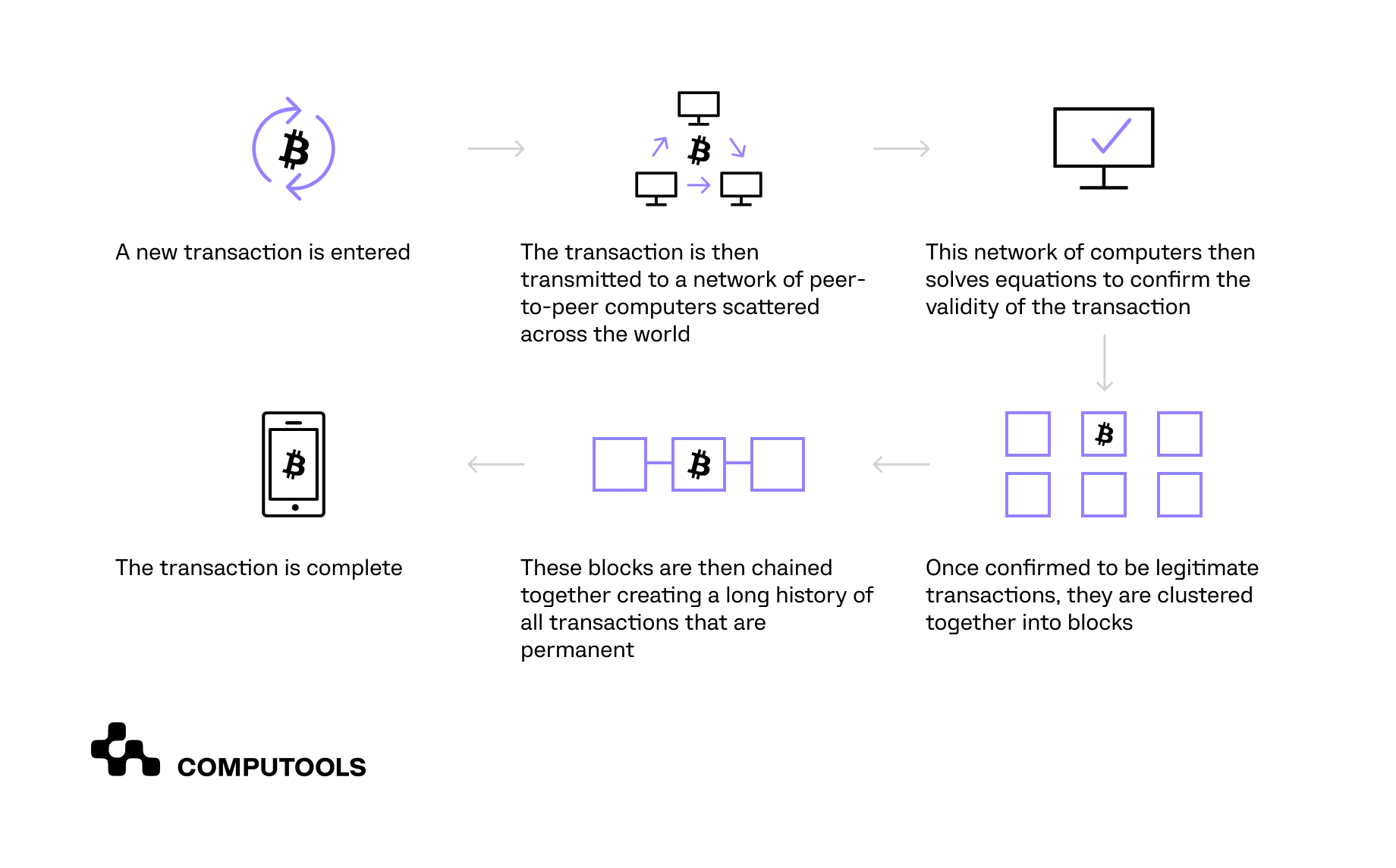

You may already be familiar with spreadsheets or databases. Blockchain operates on a similar principle as it’s a form of database where information is recorded and stored.

However, what sets blockchain apart is its unique data structure and access methods.

Blockchain uses scripts, or programs, for typical database operations like inputting, retrieving, saving, and securing data. It’s a distributed system, meaning its data is replicated across numerous machines, and these copies must all be identical for the data to be considered valid.

Blockchain compiles transaction data into blocks, much like entering data into a spreadsheet cell. When a block reaches its capacity, it passes through an encryption algorithm, generating a unique hexadecimal number called a hash.

This hash is then added to the next block’s header and encrypted alongside the block’s other data. This process effectively links the blocks together, forming a chain.

Essential Blockchain Terminology

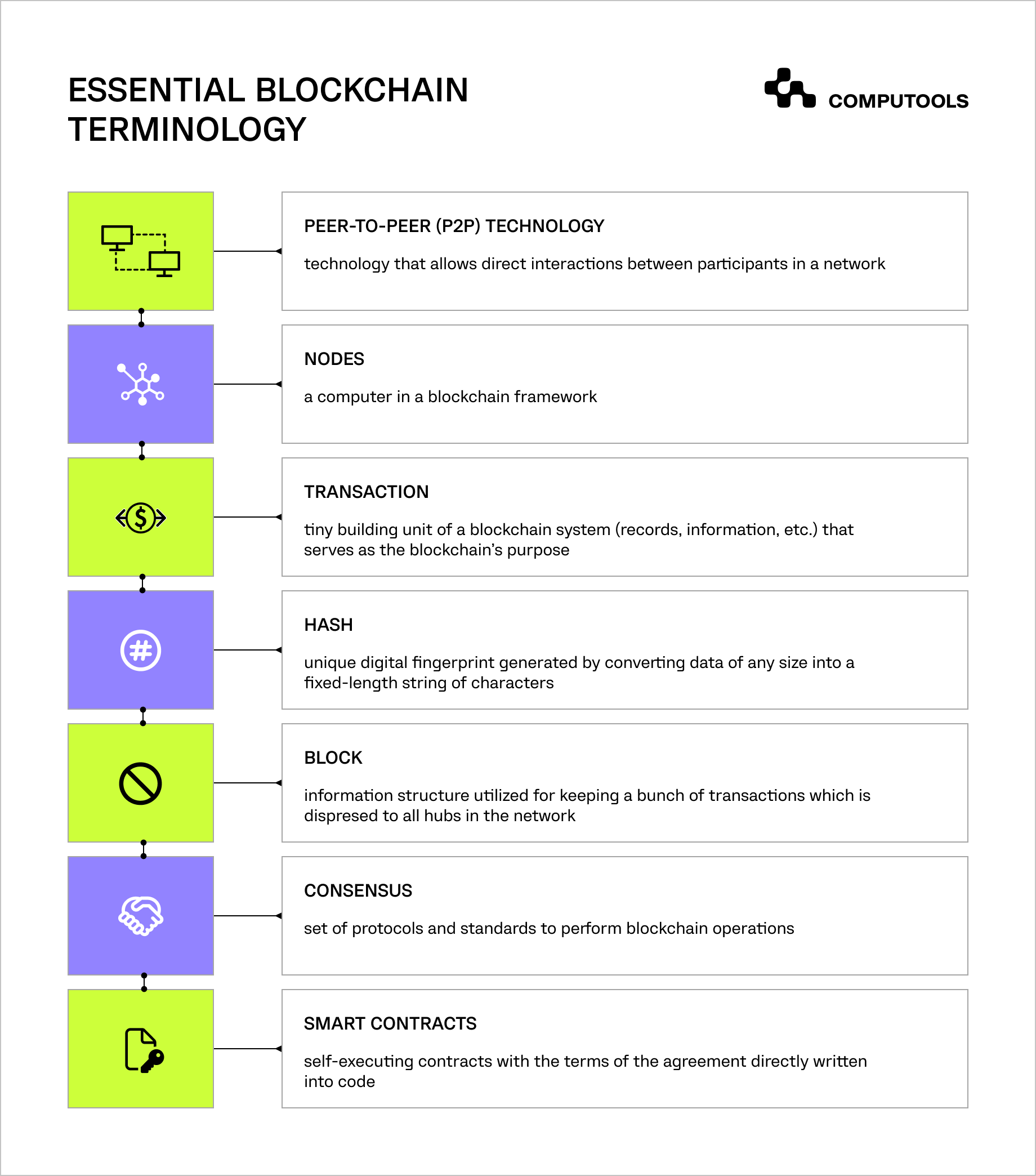

To understand blockchain technology, you need to know its core concepts. Below is a list of the most important blockchain terms.

1. Peer-to-Peer (P2P) technology

Integral to blockchain’s decentralised structure, P2P technology enables direct data exchange among users without middlemen or central authorities.

P2P networks consist of interconnected nodes or devices supporting direct communication, transaction processing, and secure, transparent transaction recording.

2. Nodes

In the blockchain network, each individual computer is called a node, and it holds a complete copy of the blockchain.

Nodes work together to confirm transactions and determine the current status of the ledger. There are two main types of nodes:

1. Full nodes: These nodes store the entire blockchain, verify transactions, and play a role in reaching a consensus among nodes.

2. Light nodes: These nodes store only parts of the blockchain and depend on full nodes to verify transactions.

3. Transaction

A blockchain transaction is an action recorded on a block, covering financial transactions, contracts, or data sharing. Verified transactions are permanently recorded on a block.

4. Hash

A unique digital signature identifying each block and its contents. Changes to block content alter the hash, which is important for maintaining blockchain integrity.

5. Block

Transactions are grouped into blocks, forming a linked sequence known as the blockchain. Each block contains transactions and a distinct hash derived from its transactions and the previous block’s hash, securely linking all blocks.

6. Consensus

A method ensuring node agreement on the blockchain’s state, validating transactions and their sequence when adding to the blockchain.

Notable mechanisms include Proof of Stake (PoS), Proof of Work (PoW), and Delegated Proof of Stake (DPoS), each determining the node responsible for adding a new block uniquely.

7. Smart contracts

Smart contracts on the blockchain automatically enforce agreement terms when certain conditions are met, allowing transactions to occur without intermediaries.

These contracts are written in languages specifically designed for blockchain systems.

Core Components of Blockchain

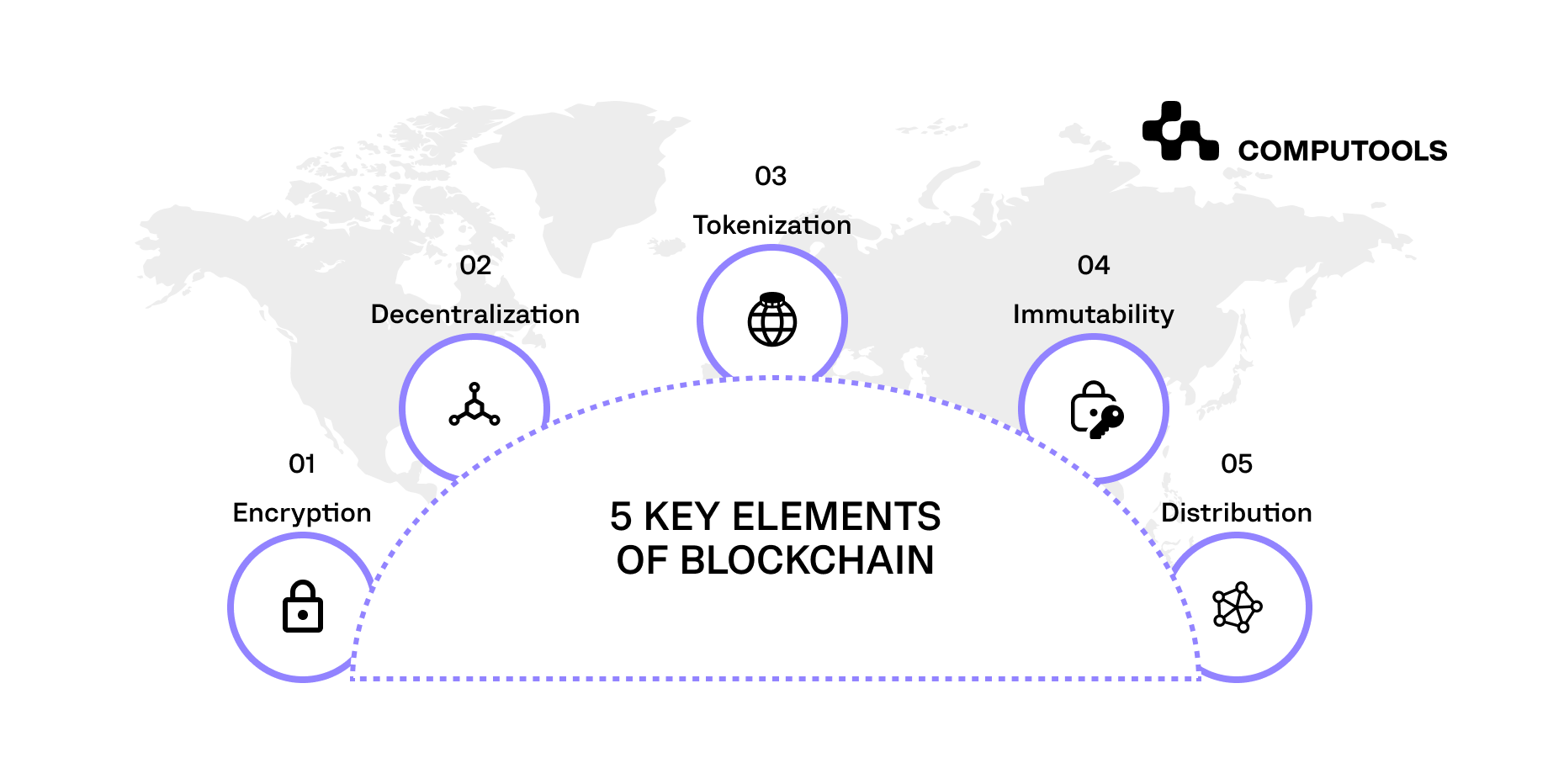

Blockchain network relies on five core design elements to confirm user identities, approve transactions and safeguard the ledger’s data, ensuring its integrity and resilience against corruption.

1. Encryption

Encryption safeguards transactions and upholds data integrity on the blockchain. It uses public-key encryption to verify identities through digital signatures.

Users sign transactions using their private keys, while public keys validate these signatures’ authenticity.

2. Decentralisation

Blockchain’s decentralised nature allows for no central authority. Control and verification are distributed among numerous network nodes, improving security and reducing risks associated with centralised points of failure.

3. Tokenisation

Tokenisation is the process of turning real-world assets or rights into digital tokens on the blockchain. This allows for ownership of physical items, voting privileges, or access to services in a digital format.

It also enables decentralised applications and provides a way to represent value digitally.

4. Immutability

The immutability of blockchain means that once data is recorded, it can’t be changed or deleted. This is because blocks are securely linked together through encryption and any changes would require agreement from many nodes in the network, making blockchain a dependable system for keeping records.

5. Distribution

The blockchain ledger acts as a distributed database, meaning it’s shared among all network nodes. This design enhances security and data accessibility by eliminating single failure points, enabling the network to remain operational even during node disruptions or security threats.

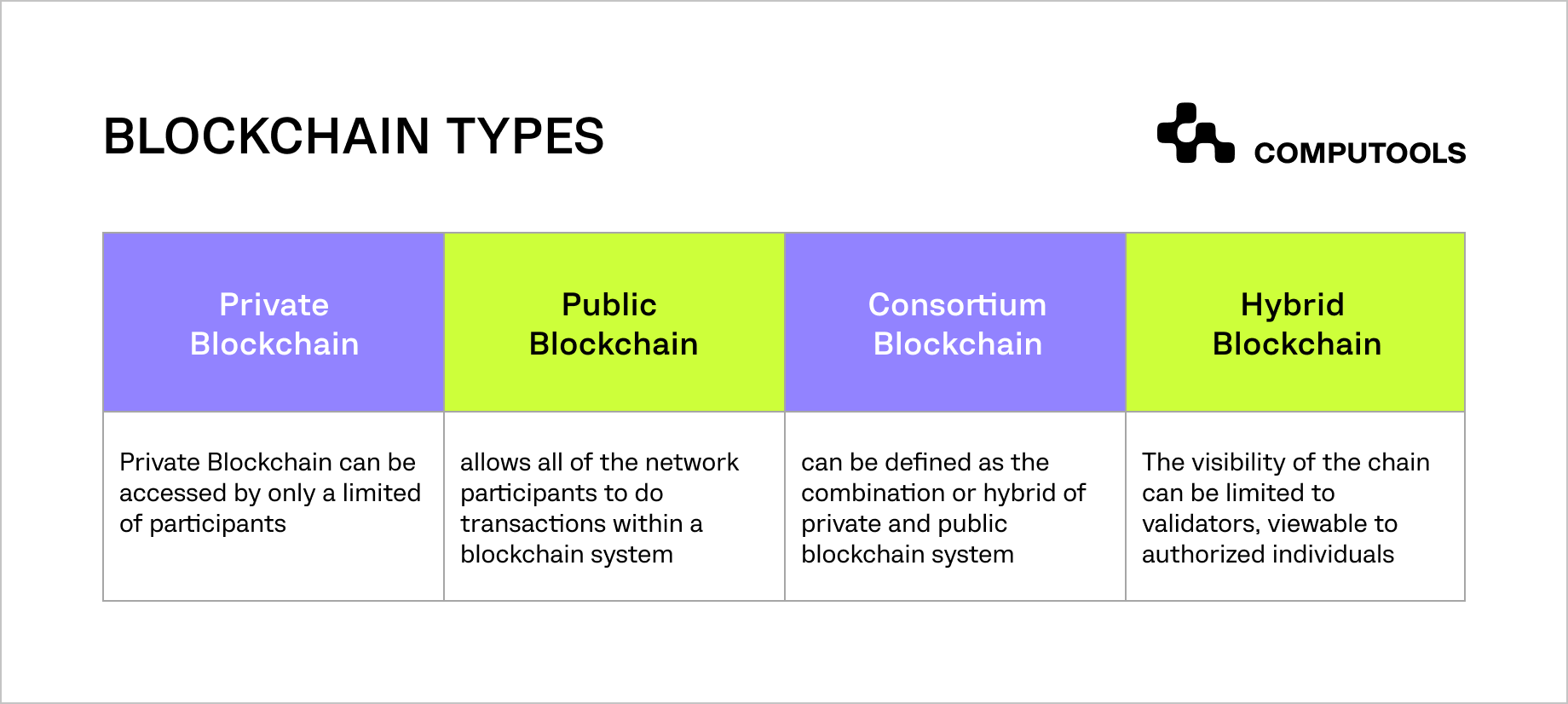

Types of Blockchain

Blockchain comes in various forms, primarily categorised as permissioned and permissionless.

All other blockchains can be classified under one or both of these primary categories.

- Permissioned blockchain restricts certain nodes from accessing the network and controls the network rights of participating nodes. Users on permissioned blockchain networks share their identities.

- Permissionless blockchain provides pseudo-anonymous access to all users. Anyone can become a node and enjoy unrestricted network rights. Permissionless networks are often more secure than permissioned ones, as they have more nodes validating transactions.

Now, let’s discuss the four key subtypes of blockchain networks:

1. Private

Also known as managed blockchain, a private blockchain is governed by a central authority, typically an organisation. This authority controls node access and grants different rights for various functions.

The public generally doesn’t have access to private blockchain networks, making them only partially decentralised.

2. Public

Public blockchain networks are entirely decentralised and open to everyone. All nodes have equal access rights, allowing them to create and validate blocks freely.

3. Hybrid

A hybrid blockchain blends characteristics of both private and public blockchain. While a single authority manages them like a private blockchain, there’s also public oversight.

4. Consortium

A consortium blockchain involves multiple organisations collectively managing the network, making it more decentralised than a private blockchain.

Setting up a consortium blockchain requires cooperation among various structures, potentially leading to logistical challenges.

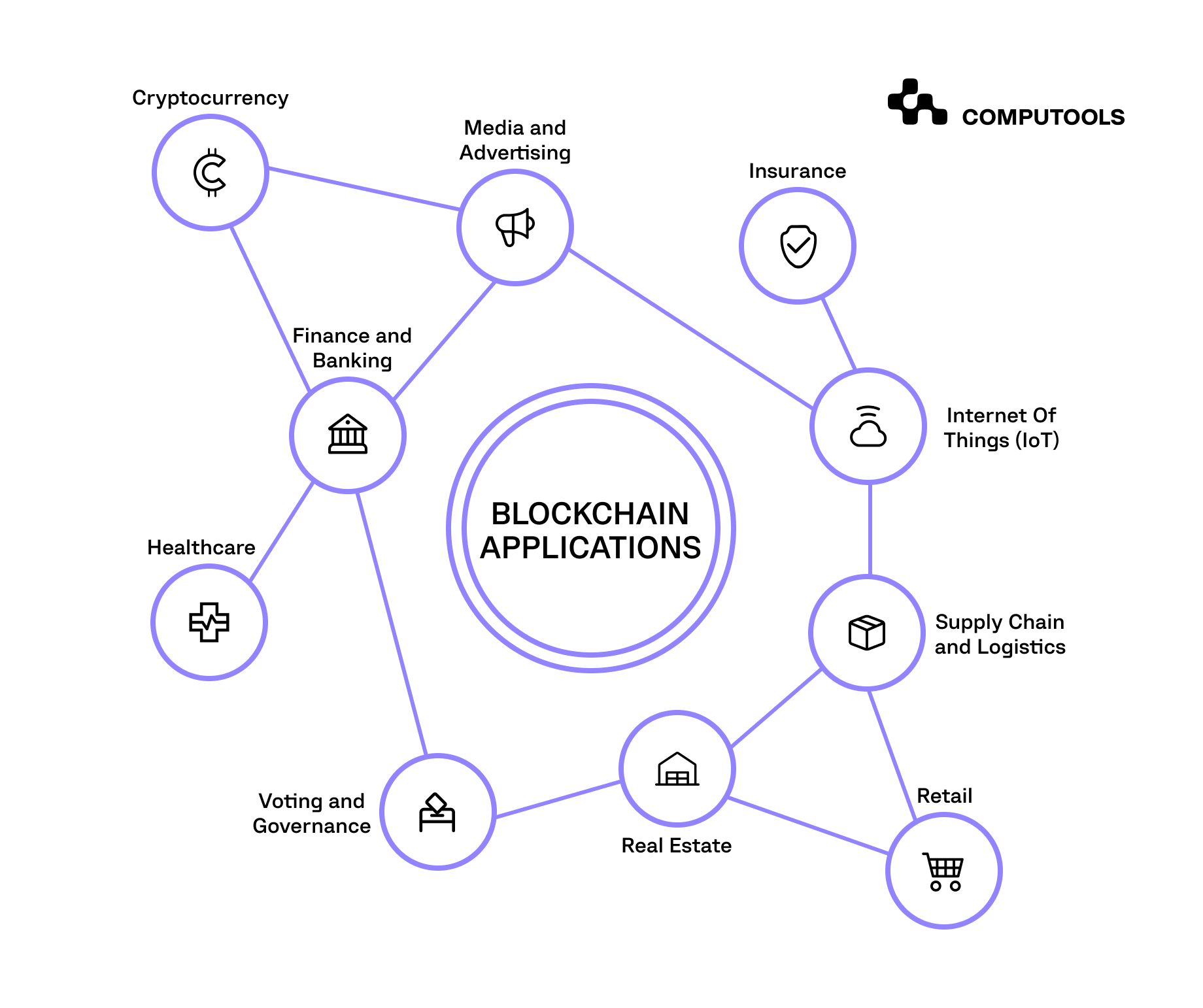

Blockchain Applications

Industries like banking, logistics, healthcare, and the public sector are increasingly adopting blockchain development services.

Blockchain’s security and reliability make it an attractive option for these sectors, serving numerous purposes.

1. Finance

Unlike traditional methods, which are slow and costly, especially for international transactions, blockchain enables quick and cheaper money transfers, often within minutes.

In lending, blockchain-based smart contracts support automatic loan processing, speeding up operations, reducing costs, and attracting more borrowers.

For insurance, these smart contracts improve transparency and expedite claim payments.

Additionally, blockchain enables the creation of decentralised financial exchanges, offering faster transactions and greater control to investors without the need for a central authority.

2. Governance

In governance, blockchain has the potential to transform voting by preventing fraud, ensuring voter eligibility, and streamlining the process through mobile devices.

Blockchain can also enhance welfare programs by reducing operational costs, ensuring that funds reach the intended recipients more effectively.

3. Supply Chain Management

Blockchain greatly benefits supply chain management by providing a reliable record of every transaction, which improves service quality and simplifies internal processes.

With blockchain’s transparency, business owners can quickly identify issues, prevent delays, and automate operations.

4. Healthcare

In healthcare, blockchain ensures the secure storage of medical records. Once a record is created and recorded on the blockchain, it becomes tamper-proof, giving patients confidence in the integrity of their records.

These records can be encrypted and accessed only by authorised personnel, ensuring patient privacy.

5. IoT

In the Internet of Things (IoT), blockchain helps speed up its adoption while tackling security issues. It ensures that connected devices stay both functional and secure by using encryption and transparency, making IoT practices much safer overall.

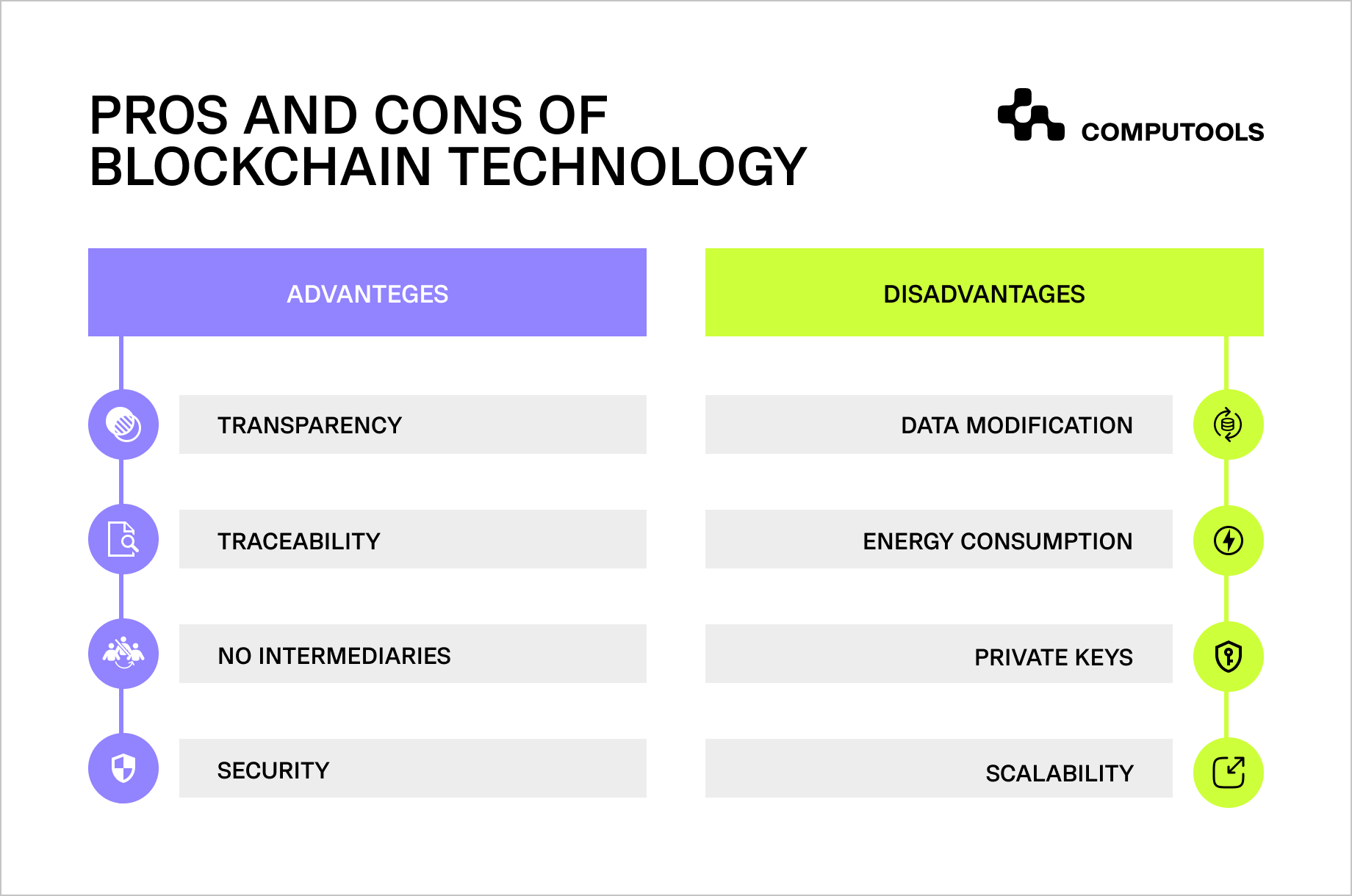

Pros and Cons of Blockchain Technology

Blockchain has been hailed as a groundbreaking innovation with demonstrated potential. However, this versatile technology is not without its drawbacks.

We’ve outlined some of the disadvantages and advantages of blockchain technology to offer a comprehensive view of its capabilities.

Benefits of blockchain

- Transparency

Blockchain networks are decentralised, enabling any network member to inspect and verify recorded data through personal nodes or blockchain explorers, allowing real-time visualisation of all transactions.

- Traceability

Blockchain creates an immutable audit trail, supporting the tracing of asset provenance throughout its journey.

This is particularly useful for industries concerned with environmental or human rights issues related to products, as well as issues like fraud and counterfeiting.

- No intermediaries

Blockchain allows for the direct exchange of digital assets between two or more parties, regardless of whether they know each other, without intermediaries like banks to verify and secure the transaction.

- Security

Blockchain networks offer multiple layers of security. Each network participant has a unique identification number, validating the legitimacy of transactions.

Additionally, transactions require accuracy validation from network members.

Disadvantages of blockchain

- Data modification

The immutability of blockchain data presents challenges for making necessary modifications or correcting errors. Rewriting code on the blockchain is a time-consuming and expensive process.

- Energy consumption

Blockchain’s significant energy consumption is a major barrier to its broader adoption. Keeping ledgers updated in real-time across all nodes requires a lot of energy.

For example, networks like Bitcoin use more energy than countries such as Denmark, Ireland, and Nigeria.

- Private keys

While blockchain offers high security, the reliance on private keys presents a risk. Losing a private key can lead to dire outcomes, with recovery almost always out of the question.

- Scalability

Current blockchain networks can only handle a limited number of transactions per second (TPS). Bitcoin, for example, manages 3 to 7 TPS, and Ethereum processes 13 to 15 TPS.

Predictions for the Future of Blockchain

All available blockchain facts indicate that blockchain will revolutionise the technology and IT sectors in the next few years, much like the internet did in the 90s and early 2000s.

The Computools team highlights three imminent trends as blockchain networks actively transform numerous industries.

1. Blockchain and related technologies will combine to unleash remarkable capabilities.

This combination will lead to the creation of never-before-seen applications. Thanks to blockchain, the data used in these applications will be more secure and reliable, allowing for sharper, more accurate conclusions based on trustworthy data.

2. The goal of complete interconnectivity is getting closer.

While it might take a few more years to achieve total interoperability between different blockchain networks, a lot of organisations now see the need for clear rules and standards to connect all these networks, both the ones that require permission and the ones that don’t.

3. The fight against fraudulent data will escalate with the introduction of validation tools.

Blockchain is set to bolster data protection by employing tools that work with crypto-anchors, IoT beacons, and oracles.

These tools connect the digital and physical worlds by incorporating external data into networks, enhancing trust and reducing reliance on human data entry.

Conclusion

With numerous practical applications already explored, blockchain is still gaining recognition.

As we enter the third decade of blockchain, it’s not a matter of whether legacy companies will adopt the technology, but rather when.

Thinking about integrating blockchain into your business workflows? Reach out to us at info@computools.com to arrange a consultation with our blockchain experts at Computools.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.